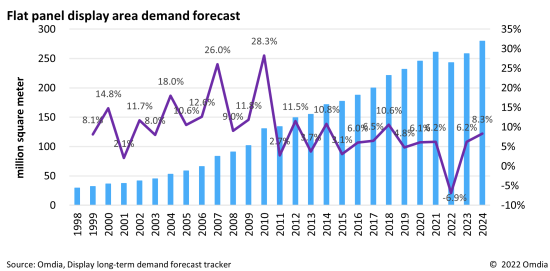

Omdia’s latest Display long-term demand forecast tracker indicates that area demand for displays in 2023 will grow by 6.2% year-on-year (YoY). With softened inflation and slowing interest rate hikes, plummeting demand has bottomed out, thereby making way for a rebound to normalization in demand by the second half of 2023.

Display demand in 2022 was expected to fall below the normal level and escape the impact of COVID19. Along with global inflation, supply chain disruption and the energy crisis due to increasing raw material costs there has been a steeper fall in demand which has resulted in a 6.9% decrease YoY. All in all, 2022 will be the first year in the history of flat panel display in which area demand records negative growth.

{kind=link}

Flat panel display area demand forecast

Yet, according to Ricky Park, Senior Principal Analyst in Omdia’s Display research practice, if there are signs that global inflation has slowed and the economy is bottoming out, “panel prices and retail prices that have fallen for more than a year can stimulate consumer sentiment, especially the recovery speed of demand for ultra-large sized TVs, which have seen a sharp decline in prices. This will lead to a fast recovery in area demand.”

Major panel makers are mass-producing various TV size products over 70 inches to preoccupy the extra-large sized TV market and are maximizing production cost reduction by optimizing process efficiency. It is expected that OLED TV will increase its market share by improving image quality and reducing price. The over-70-inch TV market is expected to grow by more than 15% from 18 million units in 2022 to 21 million units in 2023. In terms of area, it is expected to exceed 20% of the total TV display market in 2023 for the first time. TV display takes around 80% area shipment of total flat panel display, TV display demand recovery influence total flat display area demand forecast.

However, despite panel makers’ unprecedented efforts to lower fab utilization rates, set makers’ inventory levels have not yet normalized. This is expected to remain a burden on the panel demand market in the first half of 2023.