According to TrendForce research, global LCD monitor shipments reached 72.3 million units in 1H22, a level on par with to the same period in 2021. Certain whole devices orders in 4Q21 were deferred to 1Q22 due to logistics and transportation issues. In addition, some brands felt optimistic regarding the outlook for 2022, so they initiated aggressive promotions to stimulate sales in 1Q22.

Although the Russian-Ukrainian war and rising inflation have seriously impacted demand in the European consumer market since Q2, demand for business models is still positive, which in turn bridges the gap left by the consumer market.

{kind=link}

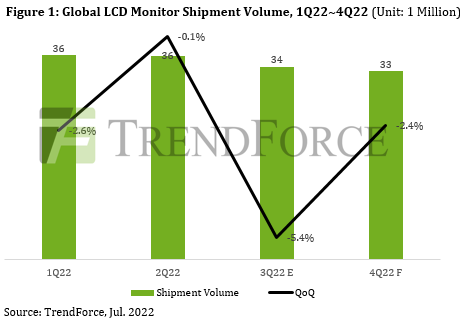

Looking forward to LCD monitor market trends in 2H22, TrendForce indicates, since most orders for business models had been digested by the end of 2Q22, coupled with the sluggishness of new orders, overall business demand momentum has not been as good as in 1H22. Consumer models are affected by rising inflation and interest rate hikes in the United States and market consumption continues in lethargy. LCD monitor shipments are expected to decrease by 5.4% and 2.4% QoQ in 3Q22 and 4Q22, respectively. The proportion of shipments in the first and second half of the year will fall at approximately 51.7: 48.3.

At present, the shortage of cargo containers and port congestion has eased. In 2Q22, the transit time of whole LCD monitor devices from China to North America and Europe decreased by approximately 2 to 3 weeks compared to 1Q22. In addition, as demand continues to weaken, branded manufacturers’ whole device inventory levels have soared. The fastest way for brands to reduce on hand inventory is to curtail the purchasing of front-end panels, components, and SI whole devices and introduce aggressive promotions to stimulate sales. TrendForce forecasts LCD monitor shipments will reach 139.9 million units in 2022, a decrease of 3.5% YoY. However, the shipment strategy branded manufacturers use to control inventory may herald a peakless peak season and a winter of discontent for panel makers and SIs in 2H22.