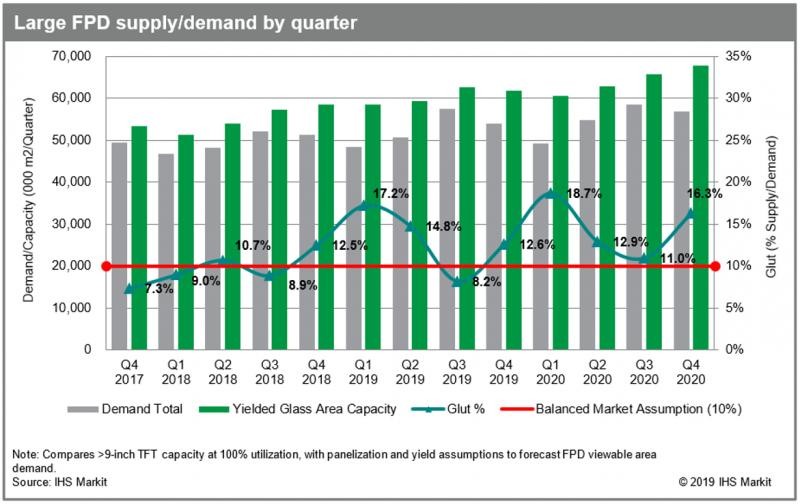

The large flat-panel display (FPD) market, which is currently experiencing oversupply, is expected to move towards a more balanced and even tight market by the third quarter of 2019, albeit briefly, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

The current imbalance for large FPDs, larger than 9 inches, is causing panel prices to fall, which is weighing heavily on profitability of panel makers. The declining profitability is already contributing to capacity rationalization and low prices are currently expected to stimulate demand. The large FPD glut is forecast to fall to 8.2 percent, below the 10-percent balance bar, in the third quarter.

Large FPD production capacity has generally been growing at a faster rate than demand for more than a year now. This growth mainly comes from new Gen 8.6 and Gen 10.5/11 factories in China, in addition to productivity improvements at legacy factories.

With the exception of the third quarter of 2018, when demand was seasonally high, prices have deteriorated continuously since the second half of 2017. In the fourth quarter of 2018, weighted-average large-panel prices fell 2.7 percent. This price decline rate is expected to accelerate to 5.4 percent in the first quarter of 2019.

Falling prices have also decreased profits, even pushing long-time Taiwanese liquid crystal display (LCD) maker CPT to file for bankruptcy protection in December 2018. Since then, the company’s production has almost completely stopped and it is unclear when or if it will resume.

The combination of low prices and growing inventories is finally causing panel makers to lower factory utilization rates. The average industry-wide utilization rate is anticipated to drop to 84 percent in the first quarter of 2019, down 3.5 percentage points from the previous year, marking the lowest level since the first quarter of 2016.

Some panel makers will also either close legacy LCD facilities or convert them to organic light-emitting diode (OLED) lines while some others will postpone their planned investment in new facilities.

“Capacity reduction and shuttering of existing FPD factories, in addition to reduced utilization rates in the first quarter of 2019, looks like a harbinger of a growing trend,” said Charles Annis, senior director at IHS Markit. “With so much new capacity currently being built out, substantial amounts of uncompetitive legacy production capacity are expected to be taken offline, as the industry works to balance supply and demand.”

According to the AMOLED and LCD Supply Demand & Equipment Intelligence Service by IHS Markit, a more balanced supply of large FPD panels should lead to firmer pricing and profitability. Some TV makers are also now predicting tighter supply later this year and have begun to increase panel procurement, which is already encouraging panel makers to start negotiating price increases on some panel sizes. Demand for large FPD panels is expected to increase to 57 million square-meters in the third quarter of 2019, up about 10 percent from a year ago.

“Although there are caveats about the global economy, early year optimism and market timing, lower prices continue to spur demand expectations,” Annis said. “As excess capacity is shuttered and demand increases, supply and demand will self-correct over time.”