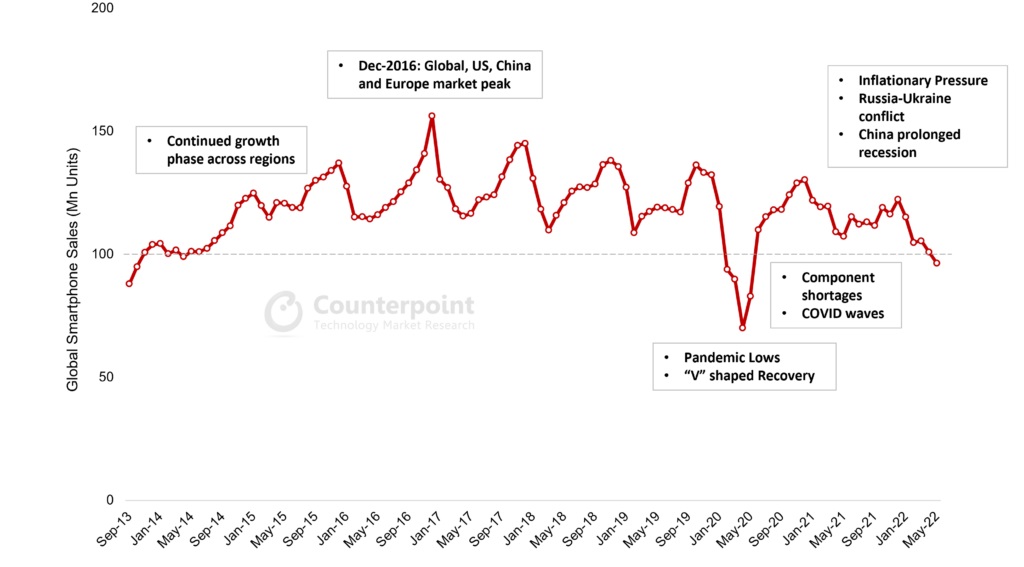

The Global Smartphone Market sales declined 4% Month on Month (MoM) and 10% Year on Year (YoY) in May 2022 to 96 million units, according to Counterpoint Research’s Market Pulse Service. This was the second consecutive month of MoM decline and the 11th consecutive month of YoY sales decline.

Even after a “V” shaped recovery following the first COVID-19 wave in 2020, the smartphone market has still not reached the pre-pandemic levels. In 2021, the smartphone market was impacted by supply constraints and persistent COVID waves. In 2022, the component shortages, although not fully resolved, have been stabilizing. However, the smartphone market is now hit by a demand slump due to multiple factors including inflation, China’s slowdown, and the Ukraine crisis.

{kind=link}

Global Smartphone Sales (sell-through), May 2022

Commenting on inflationary pressures, Research Director Tarun Pathak said, “The demand for a smartphone especially in the advanced economies is driven by replacement, which makes it a discretionary purchase. And inflationary pressures are leading to pessimistic consumer sentiment around the globe with people postponing non-essential purchases, including smartphones. The strengthening US dollar is also hurting emerging economies. A segment of consumers is likely to wait for seasonal promotions before purchasing to offset some of the cost pressures. “

Commenting on the China market, and the Ukraine crisis, Senior Analyst Varun Mishra said, “China’s lockdowns and prolonged economic slowdown has been hurting domestic demand as well as undermining the global supply chain. The smartphone market in China recovered slightly month on month in May as lockdowns eased, however, it remained 17% below May 2021. There may need to be a new baseline market size defined for China’s smartphone market. Added to this is the uncertainty created by the Russia-Ukraine crisis, which is hurting demand in Eastern Europe. None of the OEMs seems to be spared from the negative impact on demand caused by a mix of these factors.”

The low demand is also leading to inventory build-ups leading to declining shipments and order cuts from smartphone manufacturers. Q2 is likely to be the most heavily impacted this year in terms of sales before the situation improves in H2 2022.

According to the Counterpoint macro index, we expect the negativity to continue throughout the summer, but improve gradually during H2, mainly due to a more normalized situation in China, continued improvement in the supply-demand balance in tech supply chains, and a better macroeconomic landscape if inflation peaks in the mid-year period before heading back down. June also marks the beginning of a period of promotions in several regions, like 618 in China, back-to-school in August, Diwali in India followed by Christmas and New Year. It will also mark notable launches like the new Samsung Galaxy Fold series and the iPhone 14 series, which can help ignite some demand.