The worldwide semiconductor shortage will persist through 2021, and is expected to recover to normal levels by the second quarter of 2022, according to Gartner, Inc.

“The semiconductor shortage will severely disrupt the supply chain and will constrain the production of many electronic equipment types in 2021. Foundries are increasing wafer prices, and in turn, chip companies are increasing device prices,” said Kanishka Chauhan, principal research analyst at Gartner.

The chip shortage started primarily with devices, such as power management, display devices and microcontrollers, fabricated on legacy nodes at 8-inch foundry fabs, which have a limited supply. The shortage has now extended to other devices, and there are capacity constraints and shortages for substrates, wire bonding, passives, materials, and testing, all of which are parts of the supply chain beyond chip fabs. These are highly commoditized industries with minimal flexibility/capacity to invest aggressively on a short notice.

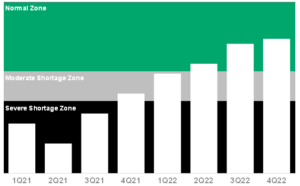

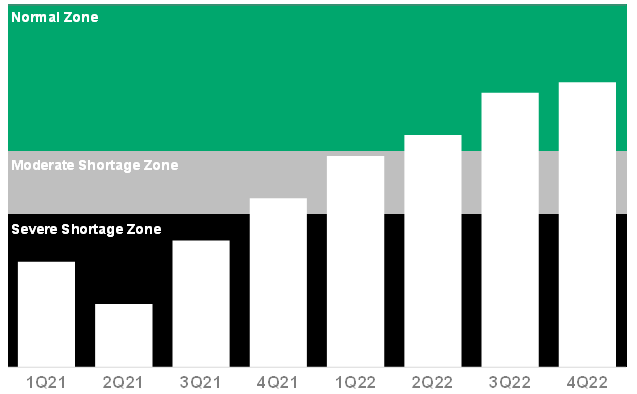

Across most categories, device shortages are expected to be pushed out until the second quarter of 2022 (see Figure 1), while substrate capacity constraints could potentially extend to fourth quarter of 2022.

Gartner Index of Inventory Semiconductor Supply Chain Tracking – Projected Worldwide Semiconductor Inventory Index Movement, 2021-2022

{kind=link}

Note: 1Q21 is a modelled estimate and is subject to change based on actual financials reported by vendors in 2Q21. The index bar for 2Q21 to 4Q22 is only a directional estimate. Source: Gartner (May 2021)

Gartner analysts recommend that OEMs dependent directly or indirectly on semiconductors take four key actions to mitigate risk and revenue loss during the global chip shortage:

- Extend supply chain visibility – The chip shortage makes it essential for supply chain leaders to extend the supply chain visibility beyond the supplier to the silicon level, which will be critical in projecting supply constraints and bottlenecks and eventually, projecting when the crisis situation will improve.

- Guarantee supply with companion model and/or preinvestments – OEMs with smaller and critical component requirements must look to partner with similar entities and approach chip foundries and/or OSAT players as a combined entity to gain some leverage. Additionally, if scale allows, preinvesting in a commoditized part of the chip supply chain and/or foundries, could guarantee the company a long-term supply.

- Track leading indicators – While no relevant parameter by itself will project how the shortage situation will evolve, a combination of relevant parameters can help guide organizations in the right direction.

“Since the current chip shortage is a dynamic situation, it is essential to understand how it changes on a continuous basis. Tracking leading indicators, such as capital investments, inventory index and semiconductor industry revenue growth projections as an early indicator of inventory situations, can help organizations stay updated on the issue and see how the overall industry is growing,” said Gaurav Gupta, research vice president at Gartner.

- Diversify supplier base – Qualifying a different source of chips and/or OSAT partner will require additional work and investment, but it would go a long way in reducing risk. Additionally, creating strategic and tight relationships with distributors, resellers and traders can help with finding the small volume for urgent components.

Gartner clients can learn more in “Semiconductor Inventory Analysis Worldwide, 1Q21 Update,” “Expert Insight Video: Global Chip Shortage Impacting the Automotive Sector,” and “Quick Answer: What Supply Chains at OEMs Dependent on Semiconductors Must Do in Wake of Current Chip Shortages.”