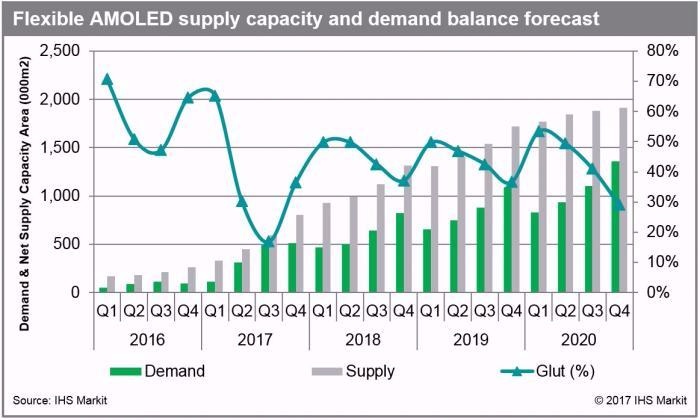

With flexible active-matrix organic light-emitting diode (AMOLED) panel fabs building at a quicker pace than global demand, supply capacity of flexible AMOLED panels is forecast to be 44 percent higher than global demand in 2018, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

The net area capacity of flexible AMOLED panels is expected to reach 4.4 million square meters in 2018, up 100 percent from 2017. However, demand for flexible AMOLED panels is increasing slower than suppliers’ expectation, at 69.9 percent to 2.4 million square meters in 2018, according to the AMOLED & Flexible Display Intelligence Service by IHS Markit.

“Panel makers had expected that flexible AMOLED panels would penetrate into the smartphone market fast,” said Jerry Kang, principal analyst of display research at IHS Markit. “But, this year, most smartphone brands have focused on LCD or rigid AMOLED wide-screens with an 18:9 or higher aspect ratio rather than curved screens using flexible AMOLED panels because the price of flexible AMOLED module is still much higher.”

According to the OLED Display Cost Model by IHS Markit, it costs 1.5 times more to produce flexible OLED panels in the Gen 6 production line than to make rigid OLED panels in the same Gen 6 line.

“The wide-screen smartphone is expected to maintain its competiveness against one with curved edge screen for a while,” Kang said.

Due to the high cost, smartphone brands use the flexible AMOLED panels for their highest-end product segment, making it more difficult for the second-tier flexible AMOLED panel suppliers to meet the product qualification. “This may result in seriously low fab utilization at the second-tier panel suppliers,” Kang said.

The AMOLED & Flexible Display Intelligence Service covers the latest trend and forecast of the AMOLED display industries (including shadow mask and PI substrates), technology and capacity analysis, and panel suppliers’ business strategies by region.

The OLED Display Cost Model provides more detailed cost analysis of OLED panels, including details of boards, arrays, luminescent materials, encapsulants, direct materials such as driver ICs. The report also covers overheads such as occupancy rate, selling, general and depreciation costs. In addition, this report analyzes OLED panels in a wide range of sizes and applications.