The flat panel display (FPD) equipment market is expected to start to decline after an unprecedented build-up in 2017 as panel makers take a more cautious approach as they wait for demand to catch up to rapidly ramping capacity.

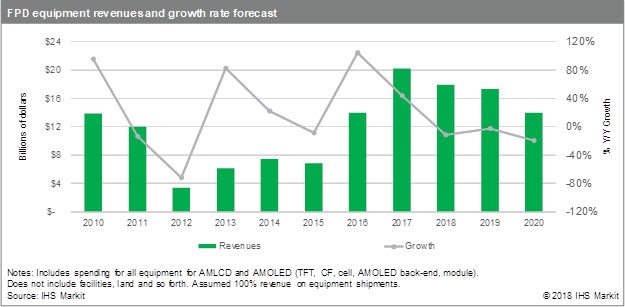

The FPD equipment market is forecast to fall from $20.2 billion in 2017 to $14.0 billion in 2020, declining at a compound annual rate of 11.6 percent, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

“The expansion of the FPD equipment market that started in 2016 has been driven by the high equipment intensity of new flexible active-matrix organic light-emitting diode (AMOLED) display factories and the scale of Gen 10.5/11 LCD factories,” said Chase Li, senior analyst at IHS Markit. “This expansion has been further fueled by Chinese local governments, which have supported panel makers with various mechanisms such as financing, land grants, reduced taxes, infrastructure and direct subsidies.”

Such broad government support of Chinese FPD fabs for all types of display technologies and factory sizes is starting to distort the supply/demand balance as the new capacity begins to ramp. In the case of flexible AMOLED factories targeting smartphones, many multiple billion-dollar investments and even expansion phases have been moving forward before panel makers have proven their ability to produce high quality panels at high yields and competitive costs. The glut level of thin-film transistor (TFT) AMOLED panels for mobile applications is forecast to exceed 40 percent of the demand in terms of area in 2019. This implies that, on average, factories for mobile applications are likely to be underutilized.

This situation has caused both panel makers and China’s local governments to evaluate more critically new flexible AMOLED factory plans. Even South Korean panel makers have pulled back from their previous plans to expand Gen 6 flexible AMOLED capacity continuously due to slower-than-expected panel demand growth. Reduced spending on AMOLED fabs for mobile applications accounts for most of the decline in equipment spending in 2018 and 2019.

Even so, Chinese local governments continue to fund selected projects despite the tightening of credit, particularly for Gen 10.5/11 LCD factories. These projects are predicted to keep equipment spending relatively firm through 2020. However, it threatens to push the large display supply/demand glut level to a record annual high of 18 percent in 2020, unless panel makers reduce excessive LCD TV panel capacity by converting some of it to OLED TV panel production and shutter less productive legacy factories.

High-end OLED TVs are one segment that is still expected to face tight panel supply for the next few years. Although, demand is low compared to standard LCD TVs, OLED TVs are a growing niche, whose panel demand is forecast to rise from 2.9 million units in 2018 to 6.7 million units in 2020. Being the only panel maker to have commercialized OLED TV panels to-date, LG Display is shipping all the panels it fabricates and running its current factories at full utilization.

According to the AMOLED and LCD Supply Demand & Equipment Tracker by IHS Markit, equipment spending in 2019 will be significantly supported by the conversion of legacy LCD fabs to advanced AMOLED factories. JOLED, Samsung Display and others are utilizing previously purchased TFT tools, while adding OLED frontplane, color conversion, cell and module equipment, hoping that they will keep them ahead of rivals and enable them to ride the growth of the AMOLED TV market.

“The FPD equipment market has always been highly volatile depending on market and technology changes. Some slow-down is not surprising following years of record high equipment spending,” Li said. “How all the equipment being installed will affect the future opportunity is a question that equipment makers are now struggling to answer. Based on IHS Markit analysis, the correction will continue beyond 2020. Even so, hope for expanding the new technology investments in AMOLED and quantum-dot (QD) OLED TVs as well as foldable displays, combined with industry restructuring and increased demand as prices fall offers the hope of another positive cycle coming.”

About IHS Markit

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.