We caught up with quite a lot of the ‘hard news’ this week, although there seemed to be plenty going on! We seem to have backed up quite a few articles that need a bit more work or research, so we hope to catch up with those next week.

The front page is dominated by the LCD supply chain. Although it has been clear for several years that we would get to this point, it’s still quite hard to get used to the idea that the LCD business will not be dominated in volume terms by the Korean makers (although they are still ahead in value) as we go forward. The current forecasts suggest that China is going to have a big dominance in share, but there are bound to be some ‘gotchas’ on the way.

As we report in LDM this week, HKC has broken ground on a second G8.6 fab, although local reports are saying that the company is some way short of the kind of yield that it needs to sustain the business in its first fab. That kind of problem may well reduce the enthusiasm of investors in China to pump in money to LCD making. However, as we often say, “engineering beats science, economics beats engineering, but politics beats economics” and much of the motivation for the LCD investment in China is political. And politics is very difficult to forecast, as we have seen over the last couple of years.

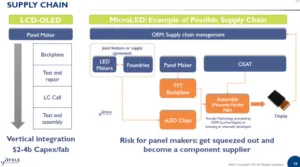

Of course, the Koreans are pushing ahead with OLED developments, but a combination of technical difficulties and deliberate attempts by each of the Koreans to stop or slow down both the other and companies in China and Japan have meant real challenges in increasing the supply the demand that could be available if supply was not constrained. The gap between the available supply and the potential demand is a big driver for the very keen interest in microLED. Now, I have been around the display industry long enough to know that there can be a big difference between ‘nearly there’ and ‘there’ in terms of product quality or manufacturability but it looks as though microLED is ‘nearly there’.

There are some big bets that may be made over the next couple of years. JOLED thinks it can solve the problems of inkjet printing OLEDs, it just needs the money for a fab, it says. Inkjet printing of OLEDs is a topic that we have been reporting on since November 1999. That was an interesting time, as the potential of AMLCD had been established, with wide viewing film, VA and IPS all being solutions to the viewing angle problems of LCD, and response times being improved. However, it wasn’t obvious at that time that TFT LCD could be made big enough or in sufficient quantity. That meant a lot of interest in alternatives at the time. However, the LCD business solved the manufacturing problems and came to dominate.

So, the question now is, will the attempts by the Koreans to control the OLED business succeed? If they do, will their success mean that the restrictions in supply growth that this might mean allow a new technology, such as microLED or even inkjet printing of OLED to enter the market as a significant segment?

It’s amazing how this industry continues to produce new ideas and technology!

Bob