The overall production capacity for large-size LCD panels rose above the expected level in the first half of 2017 despite seasonal headwinds, according to research by WitsView, a division of TrendForce. Panel suppliers actually found their processing lines fully loaded and were compelled to make some of their newly added production capacity available ahead of schedule.

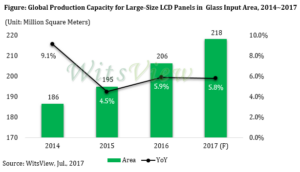

WitsView estimates that the global production capacity for large-size LCD panels in terms of total glass input area will increase by 5.8% annually in 2017 to reach 218.3 million square meters. This figure is 0.3 percentage point above an earlier estimate. Supply will become an important factor in determining the course of the panel market during second half of 2017, especially in the fourth quarter.

“This year’s increase of monthly large-size panel capacity is estimated at about 295K sheets per month (K = 1,000),” said Kou-Han Tseng, assistant research manager of WitsView. “And with some this additional capacity being made available in advance, the large-size panel capacity for the first half of 2017 is estimated to have reached 100K sheets per month, higher than the earlier estimate of 85K.”

More than 60% of this year’s newly added production capacity will become available later in the second half of 2017. Hence, the large-size panel capacity will increase by about 105K and 90K sheets per month in the third and fourth quarter, respectively.

The additional 295K sheets per month that the panel industry will be taking on this year are going to be used mainly for the manufacturing of TV panels of different sizes including the 43-, 50-, 55- and 65-inch segments. WitsView’s analysis indicates that the growing production capacity will have the greatest impact on the 43- and 65-inch segments, which have been regarded as niche markets with regard to supply.

Global monthly shipments of 43-inch TV panels were around 2.5 million units at the beginning of 2017 and then rose further this second quarter when BOE Technology’s new fab in the Chinese city of Fuzhou came into operation. Average monthly volume for the 43-inch is projected to reach 3 million units by the end of 2017, a 20% increase compared with the start of the year. Due to the loosening of supply, quotes for this size segment have also gone soft from May onward.

As for 65-inch TV panels, their prices have been on a sharp upswing since the start of 2017, spurring Taiwanese and South Korean panel makers to raise production for this size segment. As new production capacity becomes available in the year’s second half, the average monthly shipments worldwide for 65-inch panels are projected to grow by more than 30%, from just 750K units in the first quarter to about one million units at the end of the year. With the expansion in supply, the 65-inch segment will face pressure to correct prices downward during the latter six-month period.