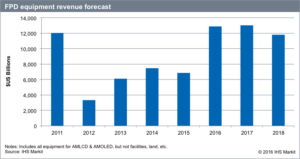

FPD equipment sales are expected to attain their highest sustained three-year level in the history of the industry. FPD equipment spending will rise 89%, hitting $12.9 billion in 2016. Increased spending levels will continue, reaching $13 billion in 2017, then declining slightly to $11.8 billion in 2018, according to IHS Markit.

“Investments in new FPD factories have been trending upwards for the past several years as Chinese panel makers continue to relentlessly build new FPD factories to make the country the largest FPD producing region in the world,” said Charles Annis, senior director at IHS Markit. “In fact, China will surpass long-dominant South Korea in capacity share by the second quarter of 2017.”

According to the IHS Markit Display Supply Demand & Equipment Tracker, in addition to the substantial number of sixth-generation (Gen 6) and Gen 8 factories (fabs) being built in China, the two largest panel makers in the country, BOE and China Star, are rushing to construct Gen 10.5 fabs that process enormous glass substrates, targeting efficient production of 65″ and 75″ panels. FPD makers in South Korea and Japan have now started ceding the LCD market to producers of lower-cost displays in China. They are also starting to shutter their large-area LCD factories, to focus on AMOLED panel production, where they still have a technology edge. Declining capacity in other regions is now balancing supply and demand, which is further encouraging Chinese makers to press their advantage and build even more factories. China will account for 65% of all FPD equipment spending, on average, between 2016 and 2018.

The FPD industry is in the midst of an unprecedented and rapid display technology shift from LCD to AMOLED for mobile applications. Samsung Display has led this change to-date with the success of its own AMOLED displays for Galaxy-based products and expansion of AMOLED panel sales to other smartphone makers looking to differentiate their products with high-end displays. Panel makers in South Korea and Japan are rushing to build new AMOLED fabs, so as not to miss out on the market shift. Chinese makers, backed by joint ventures with regional governments, are also building a large number of AMOLED factories, because they view AMOLED as a potential opportunity to upgrade from trailing-edge to leading-edge display manufacturing.

“Not only are there an extraordinary number of new FPD factories under construction, but many of the new factories are also some of the most expensive ever built,” Annis said. “Of course, the Gen 10.5 factories have much more capacity, but the capital costs are more than twice that of typical Gen 8 factories, due to the size of machines and unique facility requirements.”

Almost all of the new AMOLED factories plan to produce flexible, plastic-based displays. Most of these new factories are adopting highly complicated, high-mask-count LTPS-TFT processes that require more high-resolution exposure lines and other supporting equipment. The new flexible AMOLED lines now under construction are almost 50% more expensive than the rigid AMOLED factories constructed only a few years ago.

“FPD equipment makers are scrambling to ramp-up capacity to meet customer demand and take advantage of the best sales opportunity ever,” Annis said. “Even so, equipment companies know how cyclical the market is, so they need to manage the additional capacity and staff they are now putting in place, when the market eventually starts to slow down.”