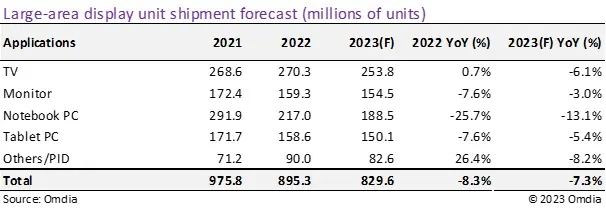

The global large-area display market is undergoing significant changes in 2023, according to the recent findings by Omdia. Year-over-year (YoY) shipments of large-area displays, which include both LCDs and OLEDs, are predicted to decrease by 7.3%, a further dip from the previously projected 3.2%.

This deeper-than-anticipated slump can be attributed to various factors. The demand for displays used in mobile PCs and monitors is weakening, resulting in fewer price increases. On the other hand, LCD TV display prices have continued to rise in 2023. While display makers began reaping profits from the LCD TV display segment around mid-2023, they continue to incur losses in the IT LCD sector. As a result, there has been a strategic reduction in IT LCD shipments for the year in an effort to minimize losses. From the close of the third quarter until the year’s end, some display makers are contemplating reducing their LCD factory utilization rates. This move aims to maintain the pricing structure of LCD TV displays. The intent behind this approach appears to focus on protecting display prices rather than boosting shipment volume as 2023 wraps up.

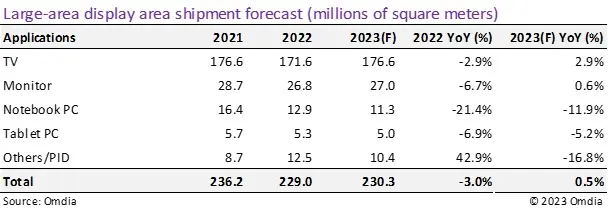

However, the total area of large-area display shipments is anticipated to see a slight uptick. Specifically, a 0.5% YoY growth is forecasted for 2023, driven mainly by consumers opting for larger TV displays. The monitor display segment is also predicted to show modest growth in shipment area by 0.6% YoY, largely due to the increased demand in specific niches like gaming monitors.

In terms of revenue, the large-area display market is projected to reach $63.2 billion in 2023, marking a 4% YoY decline. This figure is also a 3.1% drop from the earlier forecast of $65.2 billion. Only the TV display revenue segment is on track for growth, with an expected 16.4% YoY increase, bolstered by price hikes initiated in early 2023.

On the competitive front, BOE is poised to dominate the large-area display unit shipments with a predicted 32.1% market share in 2023. Following BOE are Innolux and LG with 13.7% and 11.9% respectively. When it comes to the shipment area, BOE still leads the pack with a 26.4% share, trailed by CSOT and HKC.

In the large-area OLED segment, Samsung emerges as a leader, expected to command a hefty 57.7% share of unit shipments. LG follows with a 33.2% share. But, when it comes to shipment area, LG tops the charts with an impressive 73.3%, while Samsung Display claims 25.8%.