LG and Samsung are involved in a huge battle over the premium TV market and while LG held an event in Munich this week (LG European OLED Day) and quoted data from GfK to support its contention that OLED is winning in that segment. Meanwhile, Samsung has been briefing in Korea, according to the ET News and, in particular, it has attacked IHS and the paper has reported that the IHS data is ‘not accurate’ – a significant issue for the market. Samsung also put out a press release claiming to do well. Let’s start with that.

The Samsung release says that

“according to market research firms GfK and NPD, global market revenue for big screen TVs, larger than 55 inch, occupied over 40% between January and August 2017. In North America, 60% of TV sales were for big screen TVs larger than 55 inch, with 30% for TVs larger than 60 inch”.

The company also said:

“According to GfK and NPD, between January and August 2017, Samsung was the number one player, recording 34% of total global TV market revenue, higher than the market shares of the second and third largest players combined. The company also recorded 42% for big screen TVs, 60” and larger, and 38% for UHD TVs. Samsung also led in market share based on TV pricing, with 44% in TVs, priced over $1500, and 37% for TVs over $2500.

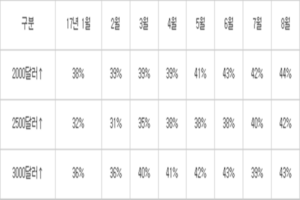

ET News quoted this data from GfK and NPD showing the recent monthly data from GfK/NPD.

The report quotes Samsung as saying that the IHS data is inaccurate because of the way that the researcher categorises the data. Effectively, IHS uses average prices, rather than per-model pricing (as GfK and NPD do) so in the example given by Samsung, if a company sells 10 TV at three different prices, $1,000, $2,000 and $3,000, they would all be counted in the band at the average price of $2,000 and the ten top priced sets would not appear in a band that is “above $2500”.

As can be seen in the data quoted at the Munich event, GfK is also capable of showing that OLED, which Samsung doesn’t supply, is doing well.

Analyst Comment

There has been a dispute between IHS and Samsung over QLED for some time. IHS sees QLED as simply a particular form of wide colour gamut LCD and not as a separate segment. I would agree with them. If you don’t do that, should you have a separate segment for RG phosphor LCDs? Or for LG’s “nanocell” filters?

However, Samsung, which succeeded in persuading much of the market that its LED-backlit LCD TVs were, in fact, ‘LED TVs’. After that success, the company has been trying to do the same kind of thing with Quantum Dots. I absolutely understand why Samsung would want to do this, but I have been complaining about the use of the QLED term by Samsung since it started to use it to describe LCDs. Before the firm started to do this, the term was used by the industry to refer to electro-emissive quantum dot displays (effectively using QDs to replace the organic materials in an OLED-like structure).

That’s a separate argument from the point over the way that sales are tracked, but they are part of a schism between the Samsung and IHS. Of course, none of the researchers has ‘perfect data’. GfK, for example, has very good detail in some parts of the market but sometimes has big holes in the data. In the UK, for some years (and I don’t know if this is still true), GfK was getting great detailed data from many channels, but not from Dixons. Given that Dixons had 40% of the market, or thereabouts, that was something of an issue. NPD for a long time had everyone. Except, if I remember correctly, Walmart. Ooops! IHS, on the other hand, has a supply-chain driven approach. I often characterised the two views as “GfK and NPD have very good detailed views of part of the picture, while IHS has a fuzzy view of the whole picture”. As we say in the UK, “You pay your money and you take your choice”.

Some fifteen or twenty years ago, I was at an event when three different companies claimed the lead in share in the ‘large TV market’. They all claimed DisplaySearch as the source, and they were all correct, but it depended how you defined ‘large TV’. One started at 32″ or so (which was large for a CRT) and was probably LCD. The second started at 42″ and was, if I remember correctly, PDP. The third was at 50″ and was, I think, TI, with DLP-based rear projection. It was all a long time ago, and my memory is vague, but the point is that claims usually depend on definitions, hence the fighting over the meaning of words. As the Chinese say “The beginning of wisdom is to call things by their right names”

We plan to follow up on this topic. (BR)