Raghu Das hosted the Printed Electronics keynote at the event. IDTechEx has worked in this space since 2001, and believes that it is now a $24.2 billion industry – including organic and flexible electronics.

Raghu Das hosted the Printed Electronics keynote at the event. IDTechEx has worked in this space since 2001, and believes that it is now a $24.2 billion industry – including organic and flexible electronics.

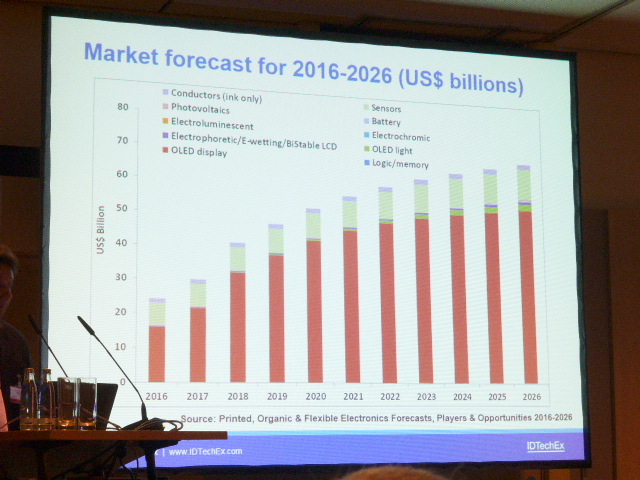

OLED displays will be the largest sector of the market this year, with a value of $16 billion. Sensors ($6.5 billion) and conductive inks ($1.4 billion) will make up the rest. Other, smaller sectors will include electronic paper ($250 million), OLED lighting (<$50 million) and electrochromic displays (<$2 million).

IDT assumes that the first flagship phone with a fully flexible display will be released in 2017. We are seeing a transition towards these types of products now with curved-but-rigid designs like Samsung’s Galaxy Edge models. Flexible OLEDs will be popular; LG Display has announced its $8.7 billion investment (see IDTEchEx Predicts Huge Investments in Flexible Displays), and SDC is likely to follow. Apple is widely believed to be preparing to release an iPhone with an OLED screen, as well, although flexibility is unlikely in this initial model.

Looking at quantum dots, Das said that the QDOT market (QDs used as an emissive material) will be worth $500 million this year, and over $3 billion by 2020. This work is at an early stage right now, and faces challenges; for instance in the use of cadmium, which is likely to see regulation review in the EU.

The next topic was reflective displays, which initially saw use in eReaders, although growth is now taking place in electronic shelf labels: 35% of these use electronic paper. Amazon continues to invest in its electro-wetting technology, which it acquired from Liquavista, although there are still no products to show.

OLED lighting was discussed by Marek Ramsi in the opening keynote (OLED Lighting is a Growth Market). Will it eventually disrupt general lighting, Das asked? 10 years from now OLED lighting could have a value of $1.8 billion, in an $80 billion lighting market. Adoption at this time will be very mixed, but led by the architectural, automotive and hospitality sectors.

Conductive inks are a shrinking part of the printed electronics market for displays (they are used for touch screen edge electrodes), said Das (although still see wide use in, for example, photovoltaic applications). This is because as bezels get thinner less ink is required. Some screens have been shown with a printed area of 20μm – it is difficult to print electrodes on areas thinner than this.

There were fewer conductive ink companies at the IDTechEx Show this year, said Das – partly due to the falling price of silver, which is used in the inks. More ink is sold, but revenues have been flat or down.

Transparent conductive films are yet another area of printed electronics, and one that has seen high levels of investment, as companies expected the adoption of touch in notebooks and AIO PCs to be higher. Consolidation is now occuring in the market. ITO/PET will remain dominant, but other technologies will represent about 60% of the market’s value.

Overall, OLED displays will remain the driving force in printed electronics until at least 2026.