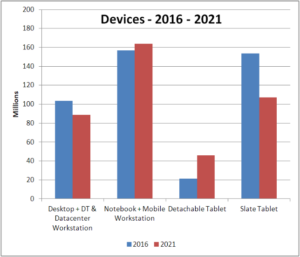

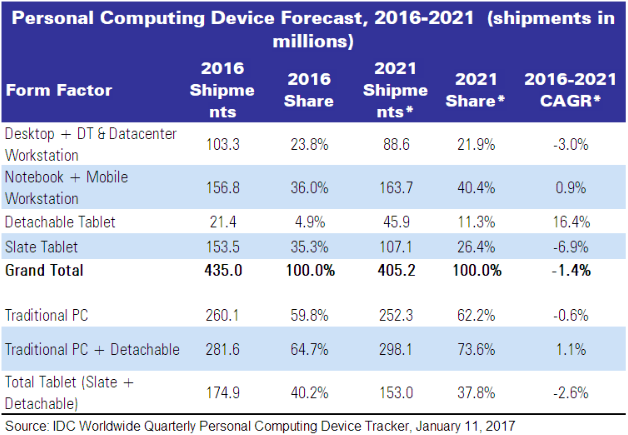

Worldwide shipments of personal computing devices (PCDs), comprised of traditional PCs (a combination of desktop, notebook, and workstations) and tablets (slates and detachables), are forecast to decline from a total of 435.0 million units in 2016 to 405.2 million units at the end of the forecast period in 2021, according to the Worldwide Quarterly Personal Computing Device Tracker from IDC. This represents a five-year compound annual growth rate (CAGR) of -1.4%. IDC has reduced its overall PCD forecast from the previous version by up to 3% depending on the year, with the largest reductions coming from the tablet product categories.

As a collective group of device categories, the PCD market is expected to return to growth in 2019, albeit marginally small. Led by a modest recovery in Europe, Middle East and Africa (EMEA) and Asia/Pacific in the first quarter of 2017, the traditional PC market registered its first quarter of positive year-on-year growth since Q1 2012. Despite the improvement, growth was less than 1% and headwinds remain. IDC expects traditional PC shipments to return to a slow decline until positive growth resumes in 2019. Desktop volume will continue to decline as consumers move to other platforms, while notebook volume will grow modestly, boosted by the commercial market and a steady move toward ultraslim and convertible notebooks.

“The steady refinement of slim and convertible designs, as well as rising commercial spending are helping stabilize overall traditional PC shipments,” said Loren Loverde, an IDC VP. “Although traditional PC shipments will decline slightly by the end of the forecast, rising replacements and steadier growth in emerging regions will keep commercial growth in positive territory and sustain total annual shipments above 252 million throughout the forecast.”

Within the tablet category, the high-level story hasn’t changed all that much. The expectation remains that slate tablets will continue to decline at double-digit rates in 2017, with contraction slowing in the later years of the forecast while detachable tablets are expected to continue strong growth. However, coming off a weaker than expected 2016 for detachable tablets, IDC has reduced its overall detachable tablet forecast with the largest reductions coming from the United States and Asia/Pacific (excluding Japan).

“Sales of detachable tablets haven’t quite met our expectations and as a result we’ve reduced volume projections throughout the forecast period,” said Ryan Reith, program VP. “New detachable tablet products continue to hit the market but the reality of this relatively new product category is that Microsoft and Apple control close to 50% of the volume and both companies have very cyclical product releases and relatively high price points. One piece of industry movement that we continue to watch closely is OEMs that have traditionally focused on the smartphone space moving further into the Windows device market. This is happening with both detachable tablets and notebook PCs, and as recently as this week Huawei announced very attractive products in both categories.”