IT market performance remained patchy in April, with some vendors and resellers experiencing a sharp decline in growth while others continued to benefit from long-term enterprise commitment to cloud, digital transformation and security investments. In its latest monthly forecast for Worldwide IT Spending Growth, IDC forecasts overall growth this year in constant currency of 4.8% to $3.27 trillion, a slight improvement on last month’s forecast which reflects resilient IT services market performance.

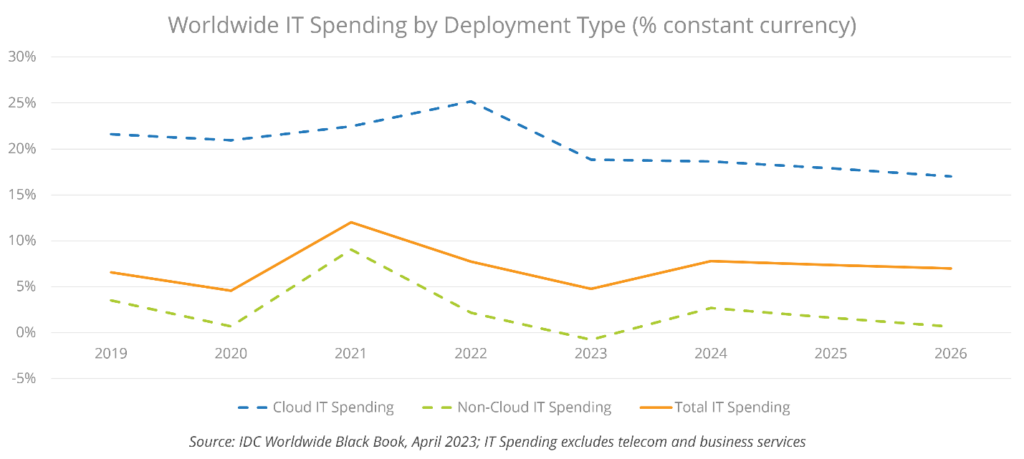

IT services growth this year will be almost 6%, as large enterprises remain committed to long-term digital transformation investments despite short-term economic turbulence. Overall software spending growth will be almost 11%, driven mostly by cloud software revenues which will increase by 19%. This marks a slowdown compared to last year’s cloud software growth of 25% and growth of public cloud IaaS will also slow compared to last year (from 33% in 2022, to 26% in 2023).

“Businesses are much more cost-conscious than a year ago, when inflation was adding to strong growth across much of the IT market,” said Stephen Minton, Vice President in IDC’s Data & Analytics research group. “Efforts to consolidate and control cloud budgets, along with economic uncertainty, mean that IT vendors are having to adjust to a slower pace of growth in the new post-COVID market. Nevertheless, continued double-digit growth in overall cloud spending is driving historic levels of resiliency for the tech industry.”

While software and services spending continue to grow, this contrasts with a significant pullback in capital spending on hardware and equipment, as interest rates begin to have a direct impact on financing while recent turmoil in the banking sector has added to a general sense of economic uncertainty.

“Higher interest rates around the world are clearly a headwind for capital spending this year,” said Minton. “Governments have reacted quickly to banking sector wild cards, but all of this just adds to expectations that a recession is still just around the corner.”

PC spending will decline by 12% this year, while peripheral hardware spending will be down 3%. What little growth there is in hardware spending in 2023 is increasingly concentrated in service provider and cloud-related budgets, but this growth will also be weaker than a year ago. Server/storage spending is forecast to increase by just 2% this year, down from 23% in 2022. While cloud infrastructure will continue to grow, non-cloud server/storage spending will decline by 7% this year.

“For IT vendors and resellers which are mostly providing on-premise and traditional hardware or software to their clients, this is shaping up to be a tough year,” said Minton. “SMB and consumer markets are feeling the impact of higher interest rates and declining confidence. While large enterprise investments in cloud and digital transformation remain resilient, and service providers continue to invest in cloud infrastructure, other areas of the IT market are experiencing a slowdown as the post-COVID shakeout continues to disrupt inventories, supply chains and demand.”