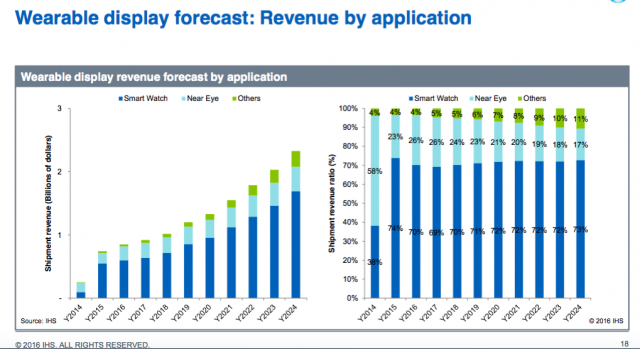

Placing a bet on wearables? Look no further than the smartwatch category, which will dominate the display revenue space going forward, according to the latest IHS data presented at Display Week 2016 business conference. At the Wednesday session on Wearable Display Technology and Market Outlook, IHS manufactuing guru Charles Annis (ok official title: Director, but he really is the former) emphasized that “Smart watches are the most significant wearable display opportunity” in the space. The caveat: don’t look for the category to contribute much to display area, as the smartwatch category will remain in “small niche” status by the display industry’s display area metric.

Perhaps the first really “cool” head worn device this side of Ray-Ban Wayfarers (green classic G-15′ tortoise of course) Source: Reddit.com In short, this means a limited opportunity for equipment and materials suppliers looking for that next engine of growth. It won’t come from embedded displays in virtual reality headsets either, even though the torrent of hype has been particularly heightened since the Facebook acquisition of Oculus VR. And this is in spite of the wave of new product announcements including brand names like Sony, Samsung and Google (ok it’s made out of cardboard, but so were the early versions of airplanes). Least we forget there are also new entrants to VR devices like Fove (a 197% successful Kickstarter project using cutting-edge foveated rendering with eye tracking – way cool and to some the real future in the space) and Avegant Glyph (they call it media wear) with perhaps one of the best industrial designs, beckoning back to Star Treck’s Geordi La Forge, (perhaps the “coolest” looking headset ever designed!)

Perhaps the first really “cool” head worn device this side of Ray-Ban Wayfarers (green classic G-15′ tortoise of course) Source: Reddit.com In short, this means a limited opportunity for equipment and materials suppliers looking for that next engine of growth. It won’t come from embedded displays in virtual reality headsets either, even though the torrent of hype has been particularly heightened since the Facebook acquisition of Oculus VR. And this is in spite of the wave of new product announcements including brand names like Sony, Samsung and Google (ok it’s made out of cardboard, but so were the early versions of airplanes). Least we forget there are also new entrants to VR devices like Fove (a 197% successful Kickstarter project using cutting-edge foveated rendering with eye tracking – way cool and to some the real future in the space) and Avegant Glyph (they call it media wear) with perhaps one of the best industrial designs, beckoning back to Star Treck’s Geordi La Forge, (perhaps the “coolest” looking headset ever designed!)

Cool-factor devices or not, it’s still not clear that VR will have a life outside of games, or even just how to scope the opportunity according to Annis. Frankly, I agree. Health care, already addressed in a previous session, will do well by the wearable market but it has the added incentive of subsidized devices (and consequently lower cost/value) Annis said. But the market overall is poised for growth (particularly for display and supply chain companies) and the numbers tell the story best.

VR By the Numbers

Since 2015, smartwatch revenue has dominated the wearable space at 70+% shipment/revenue ratio, which will continue to remain relatively flat through 2024 compared to near to eye and other technologies, according to the research. And even so, that total revenue number won’t hit $1B for the smartwatch until well into the next decade.

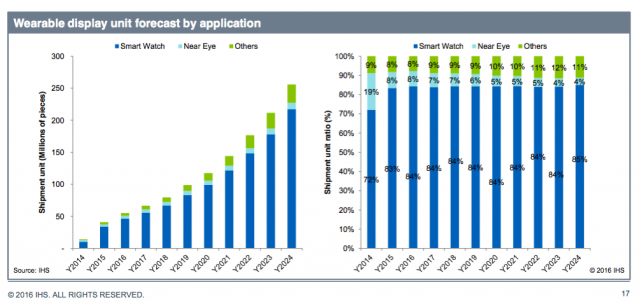

On the wearable display unit sales side, smartwatches will hit 50M devices this year and grow to over 200M by the end of 2024. With 84% of the market that also remains pretty flat throughout the period.

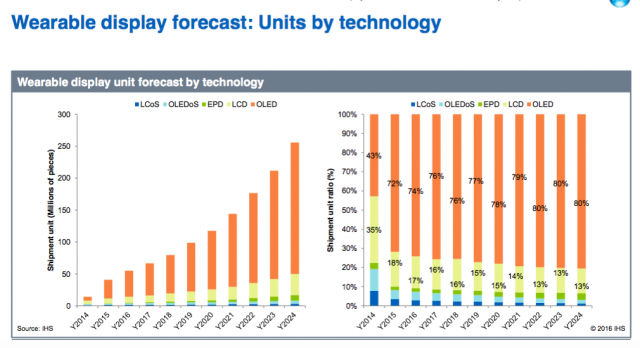

By display technology, Annis said to look for OLEDs to dominate the space with 72% – 80% market penetration throughout the period (ending in 2024). LCD, on the other hand, has moved in the opposite direction, from a high of 35% in 2014 to around 17% by the end of this year, and down to about 13% by the end of the forecast period according to IHS’ reckoning.

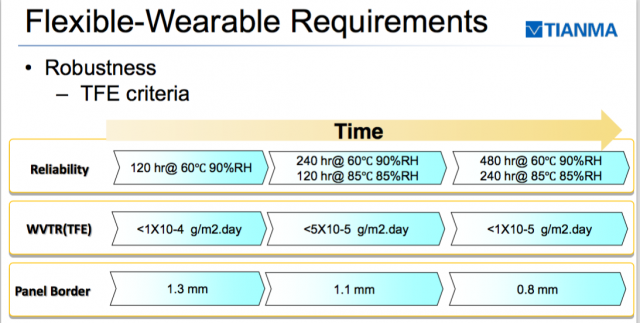

On the flexible side, we saw a presentation from DZ Peng of Tianma Micro-Electronics Group, on OLED flexible panels. The company highlighted its flexible/wearable requirements that include lower power consumption, displays initially with flexibility that will lead to “bend-ability”, which includes a thin and light design and has important metrics includin bending number and radius (see chart). This plus ruggedness : robustness in design that will require some form of thin film encapsulation (TFE for short) that is optimized for such display manufacturing.

The group said they will focus on the small & medium-sized displays and AMOLED production and shipment have already started, with the goal to speed up the developments of the wearable-flexible AMOLED displays going forward. But it will take more from the industry for these panels to go mainstream.

We see the Tianma effort as laudable, as they look to bring standards to the nascent industry, that (like OLED before) always seemed to be just two years away from full product launch. When the products finally do start hitting the shelves, perhaps this is when the smartwatch wearables market will really begin to take off.

Analyst Comment

Some (including yours truly) believe that if Steve Jobs were still alive, the Apple smartwatch would never have seen the light of day, because it is essentially (at least arguably in industrial design) a ‘me too’ device that is hard to differentiate from previously shipping products from other name brands like Sony, LG or Samsung: designs that shipped in the past with little real market traction to drive the category forward. Rather, the Apple watch is a bean-counter product designed not to inspire (bring joy to the user) but instead to satisfy the investors, and make the next quarter number. Apple clearly failed on both counts and in so doing is on the way to becoming yet another ‘me too company with its me too device. And the slippery slope just got a little slicker.

Like the first iPhone, (and iPod before it) the product category is in disarray, and begging for a break-out design and that requires a new display and industrial design along with a new way of interfacing that has never been done/seen before. It will require, some believe, the mature, flexible, bendable display to accomplish this lofty goal. So for now, even though smartwatches dominate the category, it is not a break-out product and still, as IHS points out, in a niche market space. But as evidenced even by the dearth of flexible presentations at this IHS display marketing conference, we still have a long way to go for a dependable (not to mention second source) supply of these illusive yet incredibly sexy new panels. – Steve Sechrist