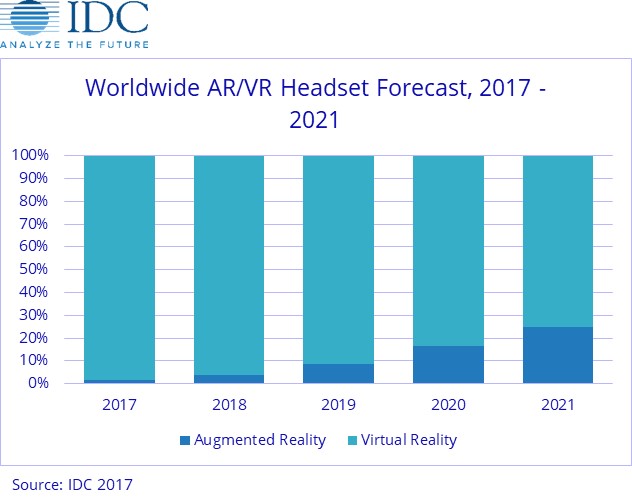

IDC is forecasting that the combined AR and VR headset market to reach 13.7 million units this year, growing to 81.2 million units by 2021 with a compound annual growth rate of 56.1%.

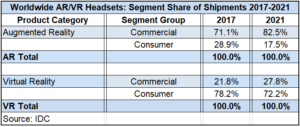

According to the IDC forecast data from the Worldwide Quarterly Augmented and Virtual Reality Headset Tracker, VR headsets will account for more than 90% of the market until 2019, while AR will account for the rest. In the final two years of the forecast (2020 and 2021), IDC expects AR headsets to experience exponential growth and to capture a quarter of the market. It is also forecast that combined shipments of AR and VR headsets will grow to 81.2 million units in 2021.

Sales of AR devices are tiny compared to VR at the moment.

Sales of AR devices are tiny compared to VR at the moment.

Jitesh Ubrani, senior research analyst for IDC believes that AR headsets are on track to account for over $30 billion in revenue by 2021, which is almost twice that of VR, as most of the AR headsets will carry much higher average selling prices. Meanwhile, Ubrani believes that most consumers will experience AR on mobile devices and consumer-grade headsets.

It is forecast that VR headsets will drive a near-term shift in computing due to recent price reductions across all the major platforms and to new entrants appearing in the next months. This should drive growth in the second half of 2017 and will help to offset a slow start to the year. Screenless viewers such as the Gear VR will continue to maintain a majority share, although the category’s share will continue to decline as lower-priced tethered HMDs gain share over the course of the next two years. IDC is predicting that standalone HMDs will gain share in the latter forecast years.

Tom Mainelli, VP of devices and AR/VR at IDC, believes that VR has suffered from some unrealistic growth expectations this year, but overall the market is still growing at a reasonable rate and new products from Microsoft and its partners should help drive additional interest in the final quarter of the year.

AR/VR Headset Market Forecasts