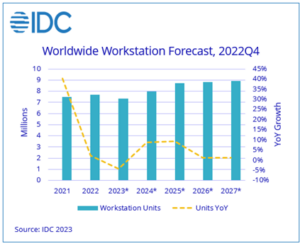

The global desktop and mobile workstation market began 2022 with strong momentum but ultimately faced saturation and economic realities near the year’s end. Unit shipments in the fourth quarter of 2022 (22Q4) shrank 22.2% compared to a year ago as IT device spending slowed amidst economic concerns and fulfillment of backlogged orders, according to the International Data Corporation (IDC) Worldwide Quarterly Workstation Tracker.

For the entire year, the market still managed to achieve a shipment record of nearly 7.7 million units, growing 2.1% and surpassing the previous record of 7.5 million set in 2021. Unlike the year prior, which saw unprecedented mobile workstation adoption due to work from home, the gains in 2022 came from the return to office momentum that sparked a desktop workstation recovery while the mobile side was flat. Nonetheless, one permanent change wrought by COVID-19 is that IDC expects the mobile form factor to be the dominant device going forward in markets where hybrid work has taken root.

“We had four consecutive quarters where shipments exceeded two million units from the third quarter of 2021 through the second quarter of 2022,” said Jay Chou, research manager, Worldwide Client Devices Tracker. “This was well above historical norms and proved unsustainable in the face of tightened budgets and ongoing inflation. After two years of strong purchases, we expect corporate IT to divert away from endpoint devices and we’ll likely see 2023 volume shrink 4.2%. This is a slight change from our previous forecast which expected a milder contraction. However, beyond the short-term challenges, we believe new model launches, Windows 11 transition, and other drivers should lead to growth from 2024.”

Worldwide Workstation Market Share by Vendor

Dell remained in the top spot, wrapping up 2022 as the only vendor with share gains. The vendor’s measured approach to inventory management helped it weather the sector downturn better than others. At number two, HP Inc. continued its focus on mobile form factors but was hurt by earlier aggressive channel shipments. Third place vendor Lenovo saw its share dip for the year due to slowing demand for its premium and value-tier models. ASUS maintained its niche in the desktop workstation space and overtook NEC in 2022 for the fourth spot.

| Company | 2022 Shipments | 2022 Market Share | 2021 Shipments | 2021 Market Share | 2022/2021 Growth |

| 1. Dell Technologies | 3,171.2 | 41.4% | 2,979.6 | 39.8% | +6.4% |

| 2. HP Inc. | 2,580.4 | 33.7% | 2,549.3 | 34.0% | +1.2% |

| 3. Lenovo | 1,860.0 | 24.3% | 1,920.9 | 25.6% | -3.2% |

| 4. ASUS | 24.5 | 0.3% | 19.7 | 0.3% | +24.3% |

| 5. NEC | 20.1 | 0.3% | 26.1 | 0.3% | -22.7% |

| Total | 7,656.2 | 100.0% | 7,495.6 | 100.0% | +2.1% |

Looking ahead, IDC expects global shipments to decline 4.2% year over year in 2023 as the market cools and the focus shifts to inventory clearing and budget discipline. Beyond 2023, expanding workload requirements should stimulate shipments to help drive solid recoveries in 2024 and 2025.