At the DisplayForum in 2003, Barry Young, then of DisplaySearch and now of the OLED Association and a contributor to Display Daily, said that the ‘perfect’ application for OLEDs was the portable DVD player. He was wrong on the device as that market didn’t develop, but he was right that the key advantages of OLED matched that application. The key device was the smartphone.

The advantages for for OLED were the

-

weight and thinness

-

great quality and power efficiency with video

-

and relatively low usage every day and short lifetime for buyer (compared to, for example, IT displays)

The fantastic advances in smartphones and the great implementation of the iPhone as a video device meant that it became the ‘on-the-go’ media consumption device rather than the portable DVD player.

However, for IT applications, the OLED has struggled to establish itself. Anybody who has ever had even a short look at an OLED-based notebook will understand the great impact that they make with their great contrast and wide colour gamut. Unfortunately, ergonomic research has shown the ergonomic advantage in most working environments of ‘negative contrast’, that is to say, dark text on a light background. That’s not news and if it had been the other way around, printers would have developed black paper and white ink! Unfortunately, although OLEDs have a power consumption advantage over LCD when most of the display is dark, when it’s bright, the advantage shifts to LCD (and one of the reasons that miniLED is so interesting for LCD makers is that it allows LCD to improve its efficiency and look to get closer to OLED with darker images).

Furthermore, OLED lifetime, especially of blue material, continues to be a challenge. If you are just using a smartphone for, say, two hours per day and replace it after three years, the total life of the display only needs to be just over 2000 hours. On the other hand, if you have a monitor that is on 8 hours a day, and that is kept for 7 or 8 years, the lifetime needs to be 16,000 hours. And as a home worker, my own monitor will probably be well over 30,000 hours by the time I upgrade it!

The combination of high brightness and long life has made image burn in a significant issue for OLED in IT applications. Although OLED monitors have been shown and sold, the numbers have been tiny up to now and products have been withdrawn by Dell and others. Sony has stopped development of OLED monitors even for broadcast applications.

DSCC does believe that there is scope for growth in OLED monitors as OLED makers shift their allocations between different applications, but I remain sceptical, unless burn in issues can be fixed. However, I am more than happy to conduct a long term test if any OLED monitor maker thinks I’m wrong 😉

What about Tablets?….

The weight/bulk and great video quality of OLED should, surely, be a big advantage for tablet applications, shouldn’t it? Well, I thought so and chose the tablet I bought several years ago because it had a great looking OLED. But with a largish smartphone and a notebook as well, I rarely use the tablet, so lifetime has not been an issue.

Over the last couple of weeks, there have been several reports from the Korean press that Apple and Samsung have agreed to defer a project to use OLEDs in Apple’s iPads in the next couple of years. The plan was first rumoured towards the end of 2020. According to the reports, Apple is not completely happy with the lifetime and/or brightness (they are inter-related) of OLEDs. The reports say that Apple wanted Samsung to use a ‘tandem’ structure for the OLED layers to boost the output and extend the lifetime. That’s an approach that LG Display uses for its automotive OLEDs, which are also under pressure over lifetime and brightness. (although your car probably has a design life of just 5,000 hours)

However, Samsung seems reluctant to supply this technology, at least, it probably doesn’t want to supply this kind of complex technology at the kind of price that Apple wants to pay! The technology is bound to be expensive. As well as using more materials and steps with potential for yield losses, the significantly longer time needed to make tandem displays would either mean a need for a big capital investment or a significant reduction in factory capacity.

Apple has, of course, used miniLED technology in its latest iPad Pro, but as we saw last year (Apple Explains the Pro XDR Monitor), the engineering in miniLED implentation with high quality is far from trivial. Moving to an OLED should be simpler, but Apple would not want to suffer from a long term warranty issue.

And Notebooks?

Back in 2015, there was a push by Samsung and LG (LG ‘Solves Burn-In’, Looks to Mid-Size OLEDs) to promote OLEDs for notebooks and at CES in 2016 we saw Lenovo (Lenovo Deluge Led by OLED Notebook) and others show products. It made me think that there was an inflection point for the technology, (OLEDs Reach an Inflection Point at CES) but the PCs were more expensive and there were significant supply issues, so things really didn’t get going and the topic and products went away again.

However, Samsung has been making the same noises again for the last couple of years and again there have been a number of products launched especially since CES this year. Why is Samsung persisting? There are two reasons, I think. The first is that the smartphone market is pretty saturated and now effectively the whole of the premium market is based on OLEDs. While you could boost volumes by switching more of the lower end to OLED (and that will happen), you won’t boost revenues by much. Revenue growth will have to come from new form factors such as foldables that will sell at a premium.

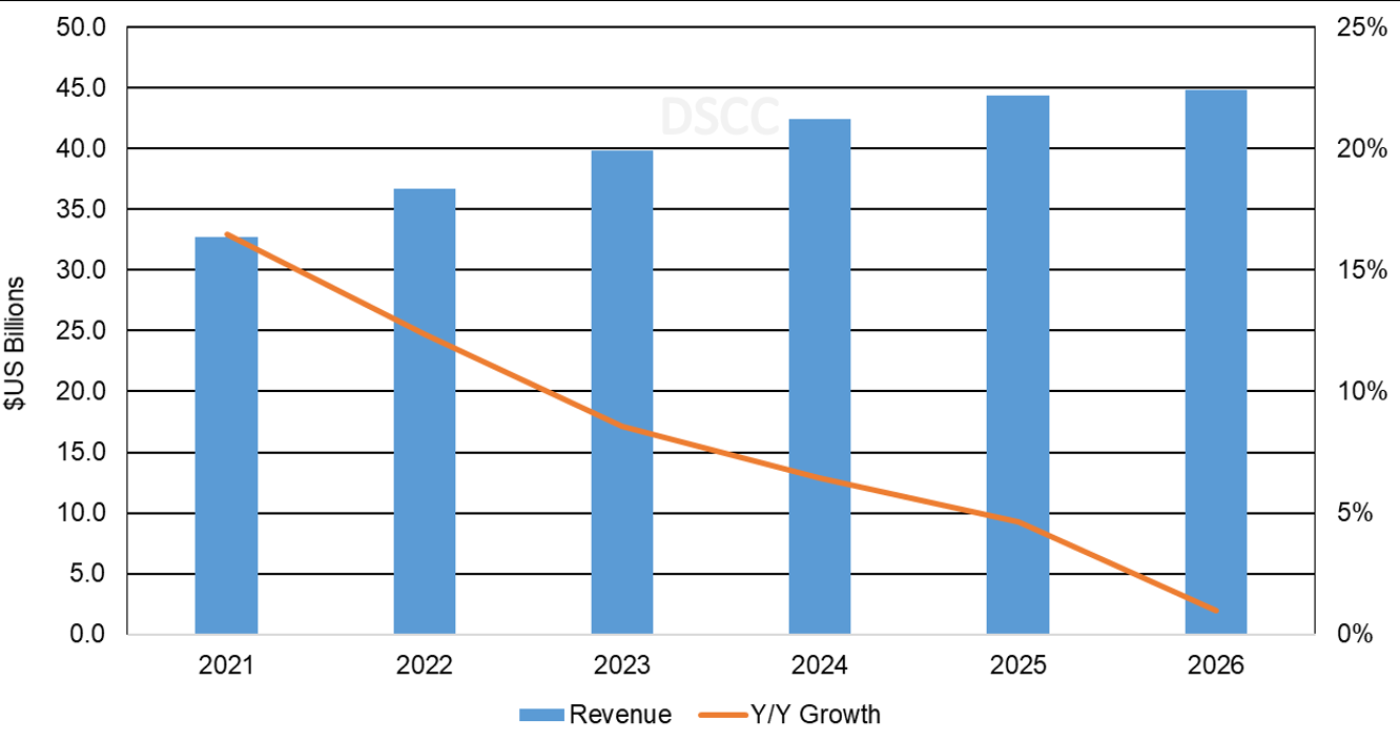

This chart from DSCC this week highlights the flattening growth in the revenues for OLED panels to be used in smartphones.

This chart from DSCC this week highlights the flattening growth in the revenues for OLED panels to be used in smartphones.

In its blog article this week, DSCC showed its forecast OLED revenues for smartphones and it confirms the flattening of revenue growth.

So, to keep growth in the OLED business, you need to drive new applications. Unfortunately, small OLEDs are made on G6 substrates. Making larger OLEDs on G6 is not so competitive and you really need to get to G8 or G8.5 substrates. LG Display, of course, makes TV OLEDs on this kind of substrate, but those are based on WOLED and wouldn’t be power efficient enough for notebooks. Samsung will want to make RGB OLEDs using polysilicon (or LTPO) backplanes and that is far from trivial in terms of technology and in terms of finance. Nobody has made LTPS at that substrate size before and difficulties in that area were reported to be one of the reasons that Samsung Display’s earlier attempts to mass produce RGB OLEDs for TVs foundered.

As it happens, this week DSCC published its latest forecast for notebook OLEDs and David Naranjo, Senior Director, DSCC said

““The long-term growth in OLED notebook PCs is driven by lower costs from new optimized fabs as panel suppliers move from G6 LTPS to G8.5 oxide. We estimate there will be a 32% savings in depreciation per 15.6” IT panel”.

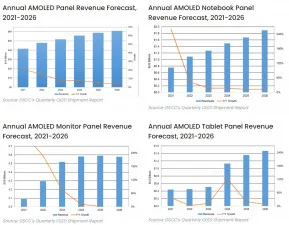

The DSCC forecasts for OLEDs for IT Applications. Note the different scales on the axes!

The DSCC forecasts for OLEDs for IT Applications. Note the different scales on the axes!

DSCC also released its forecasts for the different IT applications. It shows notebook panels growing steadily in revenue over the forecast, while monitors get started, but then stall. I would expect this to be that there is a market for high end users that will not be able to resist the lure of OLED for its great visual impact, in content creation and gaming, but that the technology will not get into the mainstream any time soon. The value of monitor revenues will only be around 1% of the value of the whole OLED panel market.

DSCC expects tablets to stay pretty much where they are until 2024. That would chime with reports that it will be around that time that Apple introduces the technology to the iPad. Revenues for tablets will still be behind notebooks and all three applications combined will only be around 9% of the overall market value, so useful, but not game-changing.

Of course, there might be room for some new form factors to brighten the prospects, as foldables are doing for smartphones and, by chance, I saw this review today of the Lenovo X1 Fold. It looks interesting, but not game-changing. (BR)