Challenges within the smartphone market carried right into the first quarter of 2019 (1Q19) with shipment volumes down 6.6% year over year, according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker.

Smartphone vendors shipped a total of 310.8 million units in 1Q19, which marked the sixth consecutive quarter of decline. In 2018, smartphone shipments dropped 4.1% over 2017, which was inclusive of a first quarter that was down 3.5% – just half of what the market experienced in 1Q19. This quarter’s results are a clear sign that 2019 will be another down year for worldwide smartphone shipments. The only highlight from a vendor perspective was Huawei, which made a strong statement by growing volume and share despite market headwinds.

“It is becoming increasingly clear that Huawei is laser focused on growing its stature in the world of mobile devices, with smartphones being its lead horse,” said Ryan Reith, program vice president with IDC’s Worldwide Mobile Device Trackers. “The overall smartphone market continues to be challenged in almost all areas, yet Huawei was able to grow shipments by 50%, not only signifying a clear number two in terms of market share but also closing the gap on the market leader Samsung. This new ranking of Samsung, Huawei, and Apple is very likely what we’ll see when 2019 is all said and done.”

From a geographic standpoint, while the China market will likely be challenged for the remainder of 2019, it was the U.S. market that felt the worst of the downturn in 1Q19. Smartphone volumes declined 15% year over year during the quarter as replacement rates continue to slow in one of the world’s largest markets. Apple iPhone challenges contributed to the exceptionally poor 1Q19 in the U.S., but they were not alone as Samsung, LG, and other top vendors also witnessed declining volumes during the quarter.

“The less than stellar first quarter in the United States can be attributed to the continued slowdown we are witnessing at the high end of the market,” said Anthony Scarsella, research manager with IDC’s Worldwide Quarterly Mobile Phone Tracker. “Consumers continue to hold on to their phones longer than before as newer higher priced models offer little incentive to shell out top dollar to upgrade. Moreover, the pending arrival of 5G handsets could have consumers waiting until both the networks and devices are ready for prime time in 2020.”

Smartphone Company Highlights

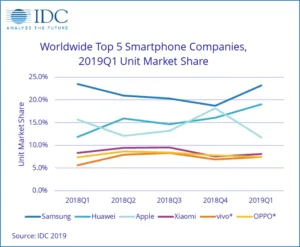

Samsung saw volumes drop 8.1% in 1Q19 with shipments of 71.9 million. The results were enough to keep Samsung in the top spot of the market, but Huawei is continuing to close the gap between the two smartphone leaders. Despite challenging earnings in terms of profits, Samsung did say that the recently launched Galaxy S10 series did sell well during the quarter. With the 5G variant now launched in its home market of Korea and plans to bring this device and other 5G SKUs to other important markets in 2019, it will be equally crucial for Samsung not to lose focus on its mid-tier product strategy to fend off Huawei.

Huawei moved its way into a clear number two spot as the only smartphone vendor at the top of the market that saw volumes grow during 1Q19. Impressively, the company had year-over-year growth of 50.3% in 1Q19 with volumes of 59.1 million units and a 19.0% market share. Huawei is now within striking distance of Samsung at the top of the global market. In China, Huawei continued its positive momentum with a well-rounded portfolio targeting all segments from low to high. Huawei’s high-end models continued to create a strong affiliation for the mid to low-end models, which are supporting the company’s overall shipment performance.

Apple had a challenging first quarter as shipments dropped to 36.4 million units representing a staggering 30.2% decline from last year. The iPhone struggled to win over conusmers in most major markets as competitors continue to eat away at Apple’s market share. Price cuts in China throughout the quarter along with favorable trade-in deals in many markets were still not enough to encourage consumers to upgrade. Combine this with the fact that most competitors will shortly launch 5G phones and new foldable devices, the iPhone could face a difficult remainder of the year. Despite the lackluster quarter, Apple’s strong installed base along with its recent agreement with Qualcomm will be viewed as the light at the end of the tunnel heading into 2020 for the Cupertino-based giant.

Xiaomi also experienced a decline in 1Q19 with volumes of 25.0 million, which was down 10.2% year over year. Despite its continued movement into Europe and other regions, Asia/Pacific (excluding Japan) remains its most important region with China, India, and Indonesia accounting for the bulk of its volume in the region. Of those three critical markets, India was the only country in Asia/Pacific where Xiaomi grew its shipments during the quarter. Its brand continues to build out in many markets including India as it continues its push beyond urban markets and into rural areas of India.

Vivo returned to the top 5 of the smartphone market with volumes of 23.2 million and a market share of 7.5%, tying* it with OPPO for the number 5 position. Other than Huawei, vivo was the only other vendor at the top of the market that was able to grow shipments in 1Q19 with volumes up 24.0% over 1Q18. India continues to be its most important market outside of China, and the company continues to invest substantial money on marketing with the Indian Premier League for Cricket being a prime example of these investments.

OPPO was tied* with vivo in terms of market share, although slightly behind in terms of overall shipment volumes. OPPO shipped 23.1 million smartphones in 1Q19, enough to capture a 7.4% market share, although volumes were down 6.0% from 1Q18. The recent announcement of the Reno series brought OPPO back to the forefront of the global smartphone innovation discussion. However, lower end models like the A series continue to drive most of its smartphone volumes.

|

Worldwide Quarterly Smartphone Top 5 Company Shipments, 2019Q1 and 2018Q1 (Shipments in millions) |

|||||

|

Company |

1Q19 Shipment Volumes |

1Q19 Market Share |

1Q18 Shipment Volumes |

1Q18 Market Share |

Year-Over-Year Change |

|

1. Samsung |

71.9 |

23.1% |

78.2 |

23.5% |

-8.1% |

|

2. Huawei |

59.1 |

19.0% |

39.3 |

11.8% |

50.3% |

|

3. Apple |

36.4 |

11.7% |

52.2 |

15.7% |

-30.2% |

|

4. Xiaomi |

25.0 |

8.0% |

27.8 |

8.4% |

-10.2% |

|

5. vivo* |

23.2 |

7.5% |

18.7 |

5.6% |

24.0% |

|

5. OPPO* |

23.1 |

7.4% |

24.6 |

7.4% |

-6.0% |

|

Others |

72.1 |

23.2% |

91.9 |

27.6% |

-21.5% |

|

Total |

310.8 |

100.0% |

332.7 |

100.0% |

-6.6% |

|

Source: IDC Quarterly Mobile Phone Tracker, April 30, 2019 |

|||||

Notes:

-

Data are preliminary and subject to change.

-

Company shipments are branded device shipments and exclude OEM sales for all vendors.

-

The “Company” represents the current parent company (or holding company) for all brands owned and operated as a subsidiary.

* IDC declares a statistical tie in the worldwide smartphone market when there is a difference of 0.1% or less in the share of revenues or shipments among two or more vendors.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools.

For more information about IDC’s Worldwide Quarterly Mobile Phone Tracker, please contact Kathy Nagamine at 650-350-6423 or [email protected].

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly-owned subsidiary of International Data Group (IDG), the world’s leading media, data and marketing services company that activates and engages the most influential technology buyers. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn.