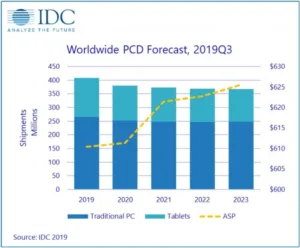

On the heels of strong growth during the third quarter of 2019 (3Q19) and changing dynamics in the market for personal computing devices (PCDs), International Data Corporation (IDC) has raised its outlook for the remainder of 2019. According to a new forecast from the Worldwide Quarterly Personal Computing Device Tracker, overall PCD shipments will reach 407.7 million by the end of 2019, up 0.5% from 2018.

However, despite this recent growth, long-term forecasts remain negative as the market will dip to 366.7 million units in 2023 with a compound annual growth rate (CAGR) of -2.6% from 2019–2023.

“The upcoming end of support for Windows 7 has been a boon for the industry as commercial organizations around the globe have been pursuing hardware upgrades in 2019,” said Jitesh Ubrani research manager for IDC’s Worldwide Mobile Device Trackers. “However, 2020 will remain challenged as the runway for OS-driven hardware purchases shortens and as upcoming tariffs combined with expected chip shortages lead to a 7% decline in new shipments.”

While the overall market remains challenged, IDC anticipates growth in modern form factors such as 2-in-1s and thin and light notebooks. “The migration of consumers towards higher price bands with each product lifecycle will be critical to the long-range health of the personal computing device industry,” said Linn Huang, research vice president, Devices & Displays. “With compute increasingly moving into the cloud and spreading out across an exploding number of devices, things, and sensors, substantial market expansion for PCs and tablets is unlikely over the long haul. Consequently, rising average selling prices (ASPs) will help offset persistent sluggishness in mature technology categories.”

Though other form factors such as traditional desktops and notebooks will continue to decline, IDC anticipates a growing share of those form factors will cater to emerging demand for creator PCs as well as sustained demand for gaming PCs. Meanwhile, slate tablets will continue their downward trajectory as their lifecycles extend and incumbents such as Apple, Samsung, and Huawei slowly shift their product portfolio toward detachable tablets.

Finally, a growing supply of cellular-enabled PCs will also provide an uplift for notebooks and detachable tablets as telcos around the world work closely with the likes of Intel, MediaTek, and Qualcomm to bring 4G-enabled devices in the short term, and 5G-enabled devices in the long term into the hands of consumers and businesses alike.

|

Personal Computing Device Forecast, 2019-2023 (shipments in millions) |

|||||

|

Product |

2019 Shipments* |

2019 Share* |

2023 Shipments* |

2023 Share* |

2019-2023 CAGR |

|

2-in-1 |

50.5 |

12.4% |

72.4 |

19.7% |

9.4% |

|

Desktop + Desktop Workstation |

93.8 |

23.0% |

76.5 |

20.9% |

-5.0% |

|

Notebook + Mobile Workstation |

74.9 |

18.4% |

50.3 |

13.7% |

-9.5% |

|

Slate Tablet |

107.0 |

26.3% |

67.3 |

18.3% |

-11.0% |

|

Ultraslim |

81.4 |

20.0% |

100.3 |

27.3% |

5.3% |

|

Total |

407.7 |

100.0% |

366.7 |

100.0% |

-2.6% |

|

Source: IDC Worldwide Quarterly Personal Computing Device Tracker, November 26, 2019 |

|||||

Table Notes:

• All figures represent forecast data.

• Traditional PCs include Desktop, Notebook, and Workstation.

• 2-in-1 devices are a category including convertible PCs and detachable tablets. Convertible PCs are notebook computers equipped with an integrated keyboard and display that can be used in either a traditional notebook configuration or a slate configuration. A detachable tablet meets all the criteria of a slate tablet but is designed to operate with a first-party keyboard designed specifically for the device.

IDC’s Worldwide Quarterly P ersonal C omputing Device Tracker gathers data in more than 90 countries and provides detailed, timely, and accurate information on the global personal computing device market. This includes data and insight into global trends around desktops, notebooks, detachable tablets, slate tablets, and workstations. In addition to insightful analysis, the program delivers quarterly market share data and a five-year forecast by country. The research includes historical and forecast trend analysis.

For more information, or to subscribe to the research, please contact Kathy Nagamine at 650-350-6423 or [email protected].