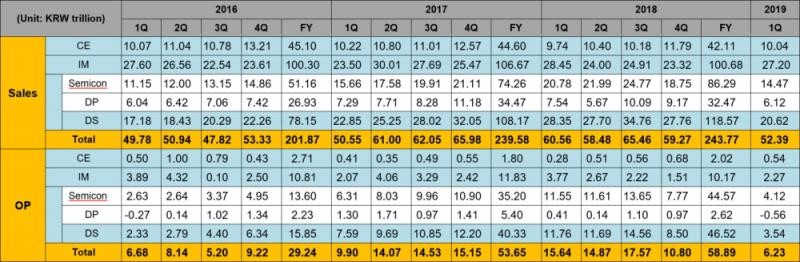

Samsung Electronics posted KRW 52.4 trillion in consolidated quarterly revenue and KRW 6.2 trillion in quarterly operating profit.

First quarter earnings were weighed down by the weakness in memory chips and displays, although the newly launched Galaxy S10 smartphone logged solid sales.

The Semiconductor Business saw a drop in memory chip prices as inventory adjustments continued at datacenter companies, while demand for high-density memory for mobile phones increased thanks to new flagship smartphones. Earnings improved at the System LSI and Foundry businesses over the sales of smartphone application processors (APs).

The Display Panel Business reported a quarterly loss due to decreased demand for flexible displays and increasing market supplies for large displays.

In the IT & Mobile Communications (IM) Division, despite solid sales of the Galaxy S10, profitability in the mobile business declined YoY as competition intensified in the low- to mid-range segment. In addition, amid softer demand in the overall smartphone market, revamping of the Company’s mass-market lineup led to a YOY decrease in sales volume.

Earnings from the Network Business increased, buoyed by the launch of 5G telecommunication service in Korea. Sales of premium TVs such as QLED TVs and ultra-large size models contributed to the YOY earnings growth in the Consumer Electronics (CE) Division.

Looking ahead to the second quarter, Samsung expects limited improvement in the memory chip market, as demand will likely begin to improve for major applications such as mobile products but price declines will likely continue.

Demand is seen increasing for APs and CMOS Image Sensors in the System LSI and Foundry businesses. For Displays, Samsung expects higher demand for rigid panels.

The IM Division is set to focus on flagship products such as the world’s first 5G smartphone and the enhanced mass-market lineup with innovative cameras and display features. The CE Division is likely to report growth in the second quarter on strong seasonal demand for air conditioners and sales of new premium TVs.

For the second half of 2019, the Company expects memory chip demand for high-density products to increase, but uncertainties in the external environment will persist. A further recovery is seen for the Display Business as demand for flexible screens is set to rise on new smartphone launches.

Growing competition in the mature TV and smartphone markets is expected to pose a challenge in the second half, and Samsung will focus on strengthening its leadership in the premium segment.

Over the mid- to long-term, the Company aims to strengthen competitiveness of key businesses by diversifying applications and delivering innovations in components and new device form factors. Samsung will also continue to expand its capabilities in automotive technology, leveraging HARMAN’s solutions, and in artificial intelligence.

In the first quarter, Samsung Electronics’ capital expenditure totaled KRW 4.5 trillion, including KRW 3.6 trillion spent on semiconductors and KRW 0.3 trillion on displays.

Semiconductor Sees 2H Demand Improvement Despite Uncertainties

The Semiconductor Business posted consolidated revenue of KRW 14.47 trillion and operating profit of KRW 4.12 trillion for the quarter.

Overall, the Memory Business saw demand for NAND and DRAM steadily weaken amid macroeconomic uncertainties, weak seasonality and inventory adjustments by datacenter firms. This weakness was partially offset by increased adoption of high-density memory products for mobile and launches of flagship smartphones.

In the second quarter, the overall memory market is likely to remain slow during weak seasonality, although the Company expects demand for some applications to gradually improve.

For NAND, demand for high-density server SSD such as All-Flash-Array is expected to increase, while launches of high-end smartphones with 256GB and higher storage will likely keep demand stable in the second quarter. For the second half, NAND demand is expected to grow across key applications as prices soften. Samsung will seek to actively generate new demand while responding to customer demand for high-density memory, and also strengthen cost competitiveness by expanding supply of 5th generation V-NAND.

For DRAM, server demand will likely improve among datacenter companies with lower inventory levels, starting from the end of the second quarter. PC demand is seen increasing, while high-density adoption in new smartphone models is set to help demand for mobile DRAM. The Company plans to actively address demand for differentiated high-end products, such as LPDDR4X for mobile devices, while also focusing on the transition to 1Y-nm in major applications.

As for the second half, DRAM demand is expected to rise thanks to seasonal effects despite lingering uncertainties. Also, demand for high-density products for server and mobile products is likely to be solid due to expanded adoption of new CPUs in servers and the trend toward high-density in mobile. Samsung plans to flexibly manage its capacity and strengthen competitiveness by ramping up production of 1Y-nm products.

For the System LSI Business, despite slowing demand for image sensors amid weak smartphone seasonality, earnings improved in the first quarter on the back of increased supply of APs and modems. The Company also successfully commercialized the world’s first 5G chipset solution.

In the second quarter, earnings for the business are expected to improve slightly as demand for image sensors and DDIs recovers and demand for 5G chipsets rises. In the second half, despite sluggish demand, smartphone makers are expected to continue to adopt high-spec components. Samsung plans to expand its lineup of image sensors and 5G chipset solutions to address demand for high-end mobile phones. It also plans to diversify product offerings with 3D/fingerprint-on-display sensors and chips for automotive and IoT applications.

For the Foundry Business, earnings were stagnant QoQ due to sluggish global foundry conditions and weak seasonality in the smartphone market. The Company began mass production of 5G and IoT mobile products by adopting the eMRAM process and secured new orders for computing chipsets through FinFET 8-nm process.

Looking ahead, Samsung aims to strengthen its competitiveness through tape-out of the EUV 6-nm process and by completing 5-nm process development. In the second half, based on its mass production of EUV 7-nm process, the Company will focus on developing the EUV 4-nm process and the next-generation architecture.

Display Sees Moderate Improvement In 2Q

The Display Panel Business reported KRW 6.12 trillion in consolidated revenue and KRW 0.56 trillion in operating loss in the first quarter. It posted an operating loss due to weaker profitability in both mobile and large displays.

Mobile displays suffered slower demand and intensifying competition with LTPS LCDs. Large displays also took a hit from a continued decline in LCD panel prices amid weak seasonality.

Looking ahead to the second quarter, Samsung expects limited improvement to earnings as demand for flexible displays is likely to remain weak. The Company will focus on improving earnings by boosting sales of rigid OLEDs and offering differentiated products featuring new technology such as Infinity Display and fingerprint-on-display.

For large displays, the Company forecasts growing demand for value-added products such as large-sized and high resolution TV panels in the second quarter, although concerns over supplies continue. It will focus on actively addressing demand for its core products, providing differentiated technology and improving cost structure.

In the second half, demand for flexible smartphone OLED panels is expected to rebound although pressure on LCD panel prices will persist. Under these circumstances, Samsung will actively respond to demand from major smartphone customers and broaden its OLED business scope with new applications.

As for large displays, despite uncertainties from capacity expansions in the LCD industry, the Company expects demand for the premium TV panels to continue to grow including UHD, 8K and ultra-large TVs. In response, it will strive to improve profitability by focusing on value-added products.

Mobile Supported by Strong Galaxy S10 Sales

The IT & Mobile Communications Division posted KRW 27.2 trillion in consolidated revenue and KRW 2.27 trillion in operating profit for the quarter.

Overall market demand for smartphones decreased QoQ as the industry moved into a seasonally weak period, but Samsung reported a QoQ rise in revenue thanks to solid sales of the Galaxy S10.

However, growth in smartphone shipments was limited as sales of previous models fell due to a lineup reorganization of mid- to low-end products. Increased expenses from adoption of high-end features, marketing and the lineup revamp pressured profitability. Earnings for the Networks Business also improved thanks to the commercial launch of 5G in South Korea.

Looking ahead to the second quarter, as weak seasonality continues, market demand for smartphones is expected to increase slightly QoQ. Samsung will strengthen its product lineup through innovations such as Galaxy S10 5G and Galaxy A80 and continued reorganization of its product offerings.

For the second half, despite intensified market competition, Samsung expects smartphone sales to increase led by new models in all segments from the Galaxy A series to the Galaxy Note amid strong seasonality. In the premium segment, the Company will strengthen its leadership through the new Galaxy Note as well as its innovative products such as 5G and foldable smartphones. Samsung also aims to secure profitability by improving cost efficiency.

For the Networks Business, Samsung will strive to maintain solid performance in the second quarter on commercialization of 5G as well as expansion of overseas LTE networks. In the second half, the Company will continue to expand LTE networks globally and supply 5G equipment for markets such as South Korea and the United States.

Consumer Electronics Eyes High-Value Products for Growth

The Consumer Electronics Division, which includes the Visual Display and Digital Appliances businesses, recorded KRW 10.04 trillion in consolidated revenue and KRW 0.54 trillion in operating profit for the first quarter of 2019.

Earnings for the Visual Display Business fell QoQ as the global TV market entered a slow season, but improved YoY thanks to the early adoption of new models. The expansion of premium product sales contributed, as Samsung solidified its global leading position in premium and ultra-large screen TVs.

Demand for TVs in the second quarter is projected to weaken slightly due to softening demand from emerging markets. Sales are also seen decreasing from a year earlier because of a lack of global sporting events this year. The Company will seek to improve results through further expanding the sales of high-value-added products such as QLED TVs and bringing forward the introduction of new models.

For the Digital Appliance Business, despite a slower global demand, growth in the domestic market has been robust with demand centering on new lifestyle home appliances such as garment refreshers and air purifiers. For the second quarter, the Company plans to improve its performance by bolstering sales of air conditioners, expected to be in peak demand thanks to the summer season.

Looking ahead to the second half of 2019, the TV market is projected to grow slightly YoY despite global economic challenges. Demand for appliances is also expected to rise compared with the first half as political tensions surrounding global trade ease.

? Consolidated Sales and Operating Profit by Segment based on K-IFRS (2016~2019 1Q)

Note 1: Sales for each business include intersegment sales

Note 2: CE (Consumer Electronics), IM (IT & Mobile Communications), DS (Device Solutions), DP (Display Panel)

Note 3: Information on annual earnings is stated according to the business divisions as of 2019

Note 4: From Q1 2017, earnings from the Health & Medical Equipment Business (HME) are excluded from the CE Division