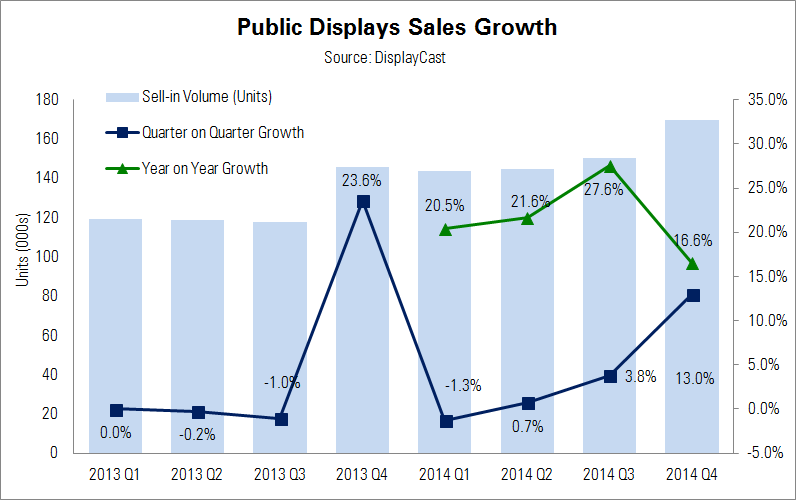

European Public Display growth was up by 16.6% on an annual basis in Q4 with 13% growth from Q3, according to the DisplayCast Public Display service from Meko.

“We have seen a change in the seasonality of the European market as it has developed”, said Bob Raikes, principal analyst for the service. “For the last several years, we have seen strong growth in Q4 and Q1 of the following year after relatively flat performance during the year”.

Samsung is the dominant player in the market, with NEC in second place and LG in third. Philips had a very strong quarter and that development meant that the top four are well ahead of “the rest”.

Regionally, the Nordics saw a good result and Russia was not as bad as might have been feared. “Public Displays tend to be part of quite extended roll-outs”, said Raikes, “so the effect of short term economic issues, such as the Russian rouble problem, tends to be delayed. In September, local vendors were still very positive about the market, but this had changed by half way through the quarter”. Sales were weak in Central Europe, while Western Europe was in line with Meko’s forecast.

UltraHD remains at just under 0.5% of the market on a volume basis and LG is the biggest player, with some good sales in MEA.