The global market for OLED materials is poised for a rebound after experiencing a deficit in recent years, according to Omdia. After enjoying steady growth path until 2021, driven by the rapid expansion of OLEDs in the display market, the OLED materials sector faced a decline for the first time in 2022.

The decline was primarily due to sluggish end-market sales of OLED TVs. The OLED TV’s larger unit area compared to other OLED applications results in higher material consumption during manufacturing. Despite OLED TV shipments being relatively low, their share in total OLED material consumption is significant.

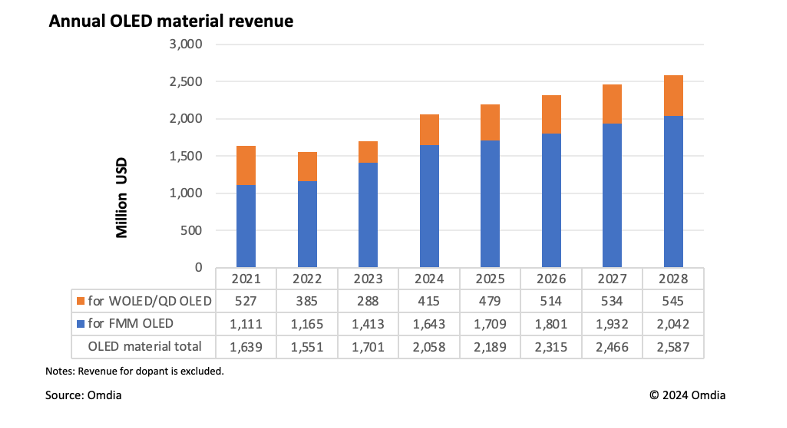

The latest data show a substantial revenue decline for WOLED/QD OLED, while revenue for FMM RGB OLED remained relatively stable. This year, the utilization of WOLED fabs appears to be improving. According to Omdia, the utilization of LGD’s Paju E4 line rebounded to over 60% in the first quarter of 2024, up from a low of 33% at the end of 2022. LGD’s WOLED line in Guangzhou also saw utilization rise to over 50%. Samsung Display plans to maintain the operation of its QD OLED fab at over 70% during the first half of 2024. “Consequently, we anticipate a significant increase in OLED materials revenue for WOLED/QD OLED this year,” Kim added.

Material revenue for FMM RGB OLED has shown robust growth since 2023. This growth is attributed to increased material demand for Apple’s latest iPad models, complemented by sustained revenue from traditional iPhone displays. Additionally, Chinese manufacturers are increasing their consumption of OLED materials to meet local display demand. Omdia forecasts that annual OLED materials revenue (excluding dopants revenue) will exceed $2 billion this year and is projected to reach $2.6 billion by 2028.