What a difference 12 months can make. In the middle of 2021, the display industry was at peak, with annual revenues of almost $160bn. Corona bounce working and studying from home had pulled in demand: this coupled with supply shortages, of glass, drivers, and ICs pushed up pricing to levels not seen since 2017. But what goes up, must come down and we are now back with TV pricing down at industry lows trading at small amounts above cash cost for some types of TV panel.

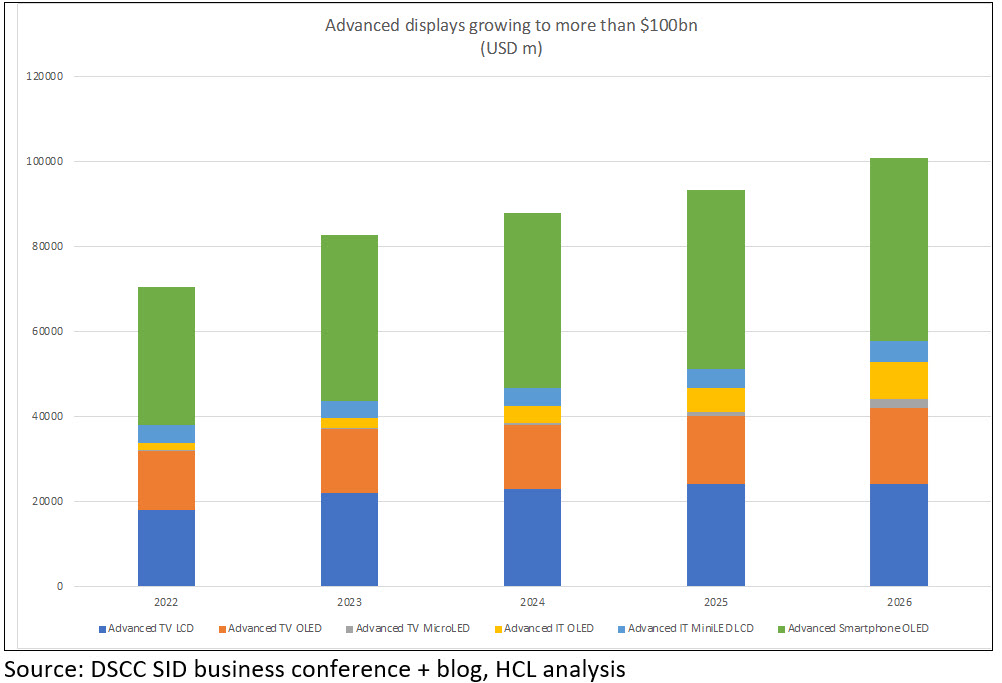

But at the same time, data from DSCC (as updated in the SID business conference this week) points to what they call “Advanced displays” market as the growing high end of opportunity. These displays are OLED or have high colour, high-pixel count (such as 8K) and high-dynamic range. This is where the money is in the display industry, if it is anywhere at all, for the materials makers, equipment makers, panel makers, and perhaps brands.

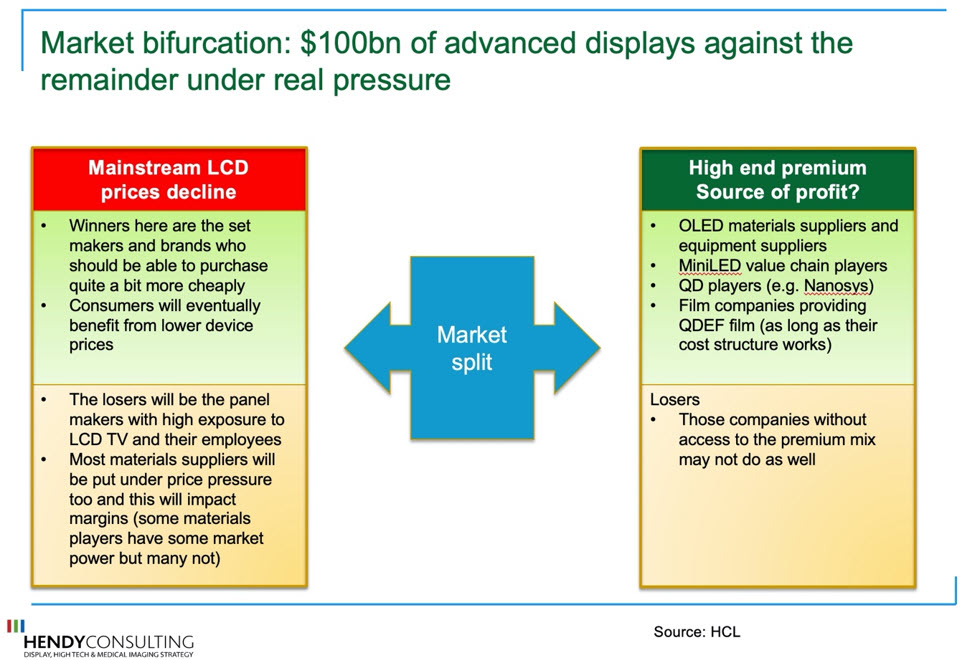

So we have a tail of two industries: one in the doldrums of deep losses and yet the other end, which is still growing and taking share in the total $160bn market, the potential for new materials, new processes and sources of profits. In a way, that I have not seen in my 25 years in the industry, it is like the industry is splitting down the middle: “Advanced displays” and true “Commodity product”

DSCC (on whose numbers from their excellent SID business conference this analysis are based) defines an advanced display as “including OLED-WOLED-QDOLED, 8K (for TV), MiniLED lit and also those with QDEF colour film colour enhancement”. Note that this market grows to $100bn by 2026. The remaining $60+bn of the display industry is then the poor relative, the ”have nots” so to speak where profits will be under immense pressure and the near-term future grim. As Bob Raikes mentioned earlier this week (The Tragedy of the LCD Commons), this market has been put into severe pressure by the debottlenecking in terms of LCD capacity that has happened during the Covid period.

The implications are stark

The implications for players in the display industry are stark: what moves do you need to make to move a greater portion of your business into the “profit pool” advanced displays part of the business and away from the commodity volume part?

Some of these choices are investments into new technologies, into OLED for example, where the new trend is a future for large Gen (Gen 8.5+) IT production based on breakthroughs in OLED deposition equipment and FMMs for larger sizes. There are new materials on the way (UDC is now giving semi-firm commitments to phosphorescent blue OLEDs in commercial product in 2024), tandem structures and cathode enhancements. OLED will show new growth going forward, especially in IT products (Monitors, NB and tablets) based on new lower cost points from breakthrough manufacturing tools.

Some of these choices are around investments in a myriad of colour enhancing QD technologies, from QDEF (where the new award-winning component technology was the new QDEF integrated diffuser plate from Nanosys) to the new QD OLED emissive technology from Samsung SDC that is just hitting the market and to future moves in QDEL longer term

The IT product OLED and MiniLED boom is new

Some of this new growth is continuation of new long-standing trends, but the growth in MiniLED lit LCDs and OLED in IT products specifically is new and heralds a new area of opportunity at the high end in a market that has traditionally been dominated by standard a-Si LCD. There will be implications for the backplane technology (and IGZO is now getting super-hot as a key backplane technology, while LTPS still remains the proven choice, as Coherent pointed out) as well as increased value in MiniLED lit BLUs for new bright, high contrast IT products

Display participants need to think hard about how to access the advanced display market, so that they can have a new blue ocean strategy to make money in the coming difficult times. (IH)