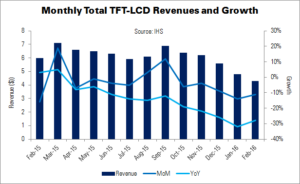

IHS has released its PriceWise data, which contains predictions of LCD panel prices in March.

TV panels

The earthquake in Taiwan (Earthquake Rocks Taiwan Production Base) this February, as well as low production yields for new models – especially from Korean panel vendors – have led to a disturbed TV supply chain. Market sentiment regarding supply and demand has been changed. Panel makers intend to stabilise prices, following losses in Q4’15 and a forecast weak financial outlook for Q1’16.

Some panel makers plan to raise the price for 32″ and 40″ units, which were strategically priced too low for TV customers. However, leading TV vendors are still waiting to observe supply chain dynamics. It is unlikely that these vendors will take clear and decisive action to adjust panel procurement plans for March and Q2’16, until supply-side issues become clearer. Slow market demand, pipeline inventories and rising G8.5 capacities have made TV makers less aggressive and more cautious.

Overall, IHS believes that the best-case scenario for panel makers is that they are able to stabilise TV panel prices for 32″ and 40″-43″ panels in March. However, the rising supply capabilities of Chinese makers remains a concern. Industry peers will continue to be pressured by the desire to move 32″ capacity to larger (49″ and 55″) sizes. It is unlikely that prices will rebound soon.

Monitor panels

Weak demand will have led to a decline in the ASP of monitor panels in March. Shipments are expected to rise MoM, and the price of 19.5″ and 21.5″ panels will fall slightly, due to the reduced supply from Taiwanese G6 fabs damaged by the earthquake. However, 23″+ panels continue to face downward pressure on prices and will have fallen by more than $0.50 in March, due to aggressive price promotions by panel makers. Korean panel makers are considering moving sub-21.5″ monitor panel capacity to TV panel production, due to losses, in Q2’16. This could lead to lower pressure on prices.

Notebook panels

Weak end-market sales will have led to a fall in notebook PC panel prices, and rising inventory for brands. The average price of mainstream models will have fallen between $0.30 and $0.50. Set makers’ purchase plans will have risen slightly, however, and panel makers are under pressure to get rid of their inventory by the end of Q1.

Deals will be struck, following negotiations over FullHD TN notebook panels, which will drop prices by between $1 and $2 to sustain volume in Q2. Therefore, replacement of a small portion of HD and FHD notebook panels is occurring now. IHS expects the downward pressure on HD TN panel prices to continue in Q2.

Mobile phone panels

Low-end cell prices are expected to have increased in March. However, smartphone module prices will have remained stable, as module makers were cautious about releasing orders. Panel makers attempted to raise prices of 5″ 1280 x 720 (HD) on-cell modules, but have not yet agreed deals with clients. Lower demand from the open cell market is also keeping the price stable.

Panel makers have released quotation prices to brands, for products coming in Q2. Lower prices on FHD displays, including in-cell units, will come into effect then.

Tablet panels

Demand for tablet PCs continues to fall, and capacity was affected by the Taiwanese earthquake. Tablet PC brands are thus driving down panel prices. Panel makers have been preparing new models for production, but brands have requested a material change to lower costs. Therefore, overall tablet PC panel prices fell by more than $1, due to the adoption of new lower-cost units.

Apple will soon release its iPad Pro Mini, with a 9.7″ oxide-TFT panel; IHS expects only Korean and Japanese panel vendors to take advantage of this, and sustain their market share. Chinese and Taiwanese brands are having difficulty promoting panels that can compete with those that Apple is using.