Display market outlook and issues were discussed at DSCC’s “The 2022 Global Display Supply Chain Dynamics & Technology Conference” on October 19th. It gave a glimpse of what is happening in the current market and what to expect in next few years.

Flat Panel display Market Slowed Down in 2022

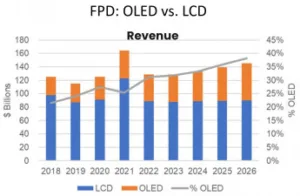

According to Bob O’Brien’s ‘Display Market Outlook” presentation, after two years of great growth, driven by the pandemic, the flat panel market has slowed down. While 2021 was the best year in flat panel display history with the biggest price and revenue increases, 2022 will be a year with double digit revenue decline and no area growth. TVs, mobile phones, monitors, notebooks, and tablets, are all expected to decline in units and revenue in 2022. High inventory in the supply chain needs to be digested and panel suppliers are cutting utilization rates.

Recovery is expected in 2023. Still global recession, macro downturn and demand constraints can bring downside risk. Stronger growth in China stimulated by lower prices especially in the TV market can bring upside potential to the forecast. For the long-term forecast up to 2026, LCD units and revenue are expected to decline slowly and LCD area growth will slow to 3% CAGR with OLED gaining share. OLED is expected to have double digit percentage area growth, but revenue growth will be slower as prices decline.

Figure 1: Source: DSCC’s Quarterly FPD Supply/Demand Report.

Figure 1: Source: DSCC’s Quarterly FPD Supply/Demand Report.

LCD and OLED battling for Premium TV Market: MiniLED & QDOLED pushing the Technology

TV is the most important application for the flat panel display market as it commands 70% share in terms of display area. It will increase its share to 72% of display area by 2024 according to Bob O’Brien’s “TV Market Outlook” presentation. According to his presentation, pandemic demand drove the biggest increase ever for LCD TV panel prices. After the pandemic demand dried up the industry saw the fastest price declines in history. TV panel prices are stabilizing at new all-time lows.

Panel price increases in 2021 also drove the first ever price increase in TV sets in the U.S market. TV inflation peaked in August 2021 at 13% but by August 2022 prices were down by 20%. Lower TV prices driven by lower demand and lower LCD panel prices are making TV set prices for the holiday season more competitive.

A Strong Technology Battle in TV

The technology battle is strong in premium TV market with a three-way battle between MiniLED LCD, white OLED and QDOLED. DSCC’s Advanced TV segment includes QDEF, WOLED, 8KLCD, MiniLED LCD and QDOLED. Except for QDEF, all are much higher costs than standard LCD. According to the DSCC cost model comparison, MiniLED LCD cost is on a par with WOLED with a range that is higher or lower depending on the number of LEDs and QDOLED has the highest cost.

According to the TV Market Outlook presentation, OLED TV has gained share with new screen sizes of 48” and 83”. In Q2 2022 OLED TV<=48” grew 50% Y/Y. Advanced LCD TV lost unit share in 2021 due to higher panel prices. In 2022 LCD is regaining unit share due to lower panel prices. MiniLED LCD TVs grew rapidly in 2021 but continue to be outsold by OLED TVs. According to Bob’s presentation:

- The worldwide TV market will continue to be dominated by LCD technologies, including MiniLED.

- Unit demand will be flat, but screen sizes will continue to increase, driving area growth at a 5% CAGR (‘19-’26) for total TV.

- OLED TV units/area will grow at a 23%/23% CAGR (‘19-’26).

- LCD TV units will decline at a 1% CAGR but area will grow at 4%.

DSCC expects Advanced TVs for all technologies to grow by 20% CAGR from 2019-2026. LCD is expected to grow by 19% driven by MiniLED and 8K. OLED will grow by 22% with QDOLED and Inkjet Printed OLED adding to WOLED. MicroLED will remain a miniscule fraction of Advanced TV units.

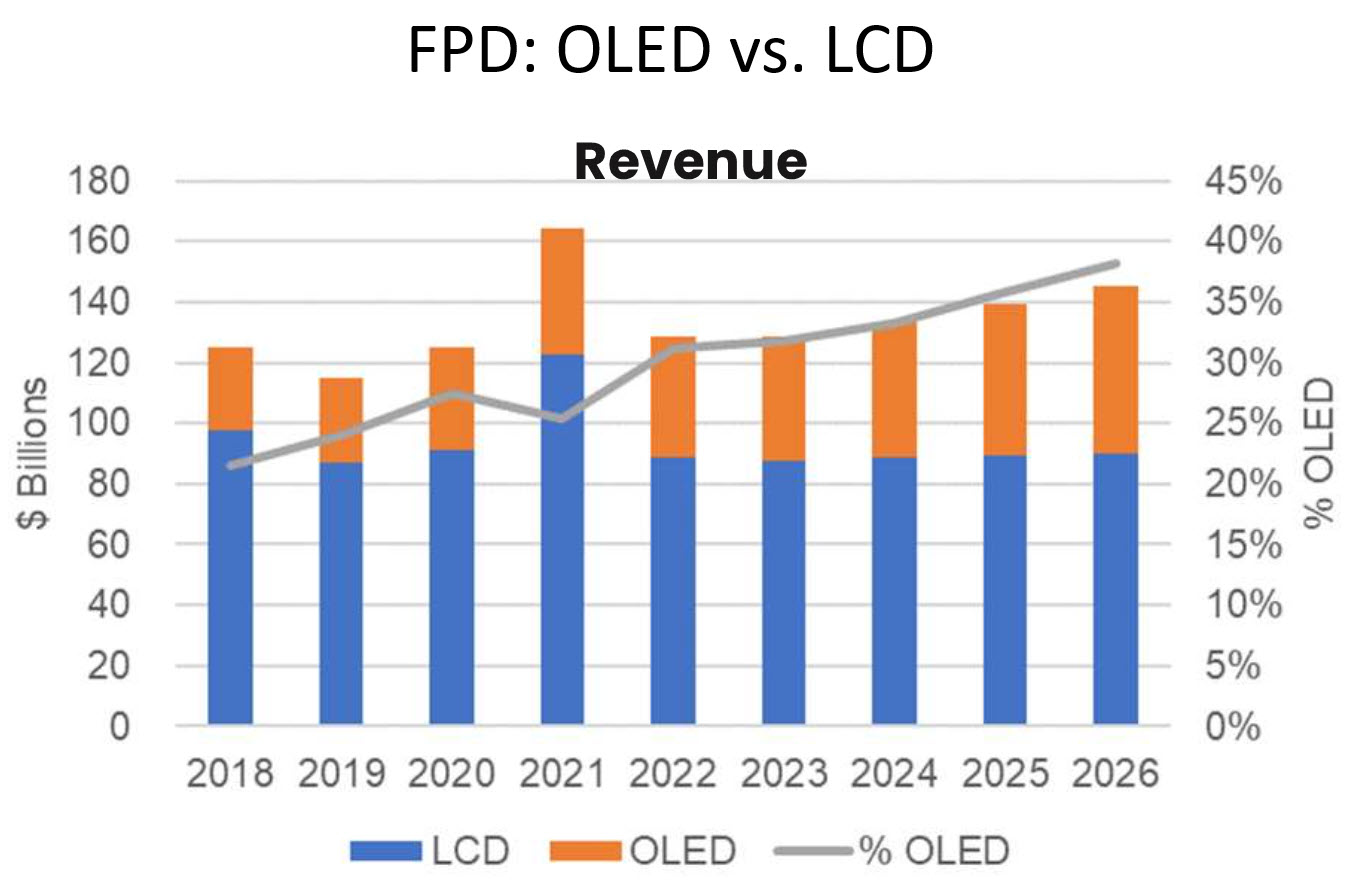

TVs using Quantum Dot technology are forecast to grow through the forecasted period up to 2026. DSCC expects growth in TVs using quantum dot technology to have 16% CAGR from 2019-2026. QD will be the dominant configuration on MiniLED TVs.

According to Ross Young’s presentation on “Display Capex and Manufacturing Technology”, Samsung Display (SDC) is planning to add another 30K QDOLED capacity to its current mass production of 8.5 Gen Fab with 30K capacity. He presented that new QDOLED investment is expected to be decided in 1H23. New phosphorescent blue OLED emitters would significantly help to reduce costs and would expand existing capacity by reducing the number of blue layers. Ross’s presentation highlighted that currently in QDOLEDS, QDs are deposited on a separate color filter (CF) substrate. In future it is expected to shift to QD on encapsulation (QOE), in which a single substrate is used and the QDs are deposited over the TFE. By this process brightness can be increased by 20%.

Figure 2: Source: DSCC Advanced TV Shipment Report

Figure 2: Source: DSCC Advanced TV Shipment Report

MicroLED TVs have been available since 2020 but prices are higher than $100K. MicroLED is expected to show strong growth but it is forecast by DSCC to have only 0.1% of unit volume of Advanced TV in 2026.

OLED Technology and Capacity Enhancements: Increasing MiniLED and OLED competition in IT Market

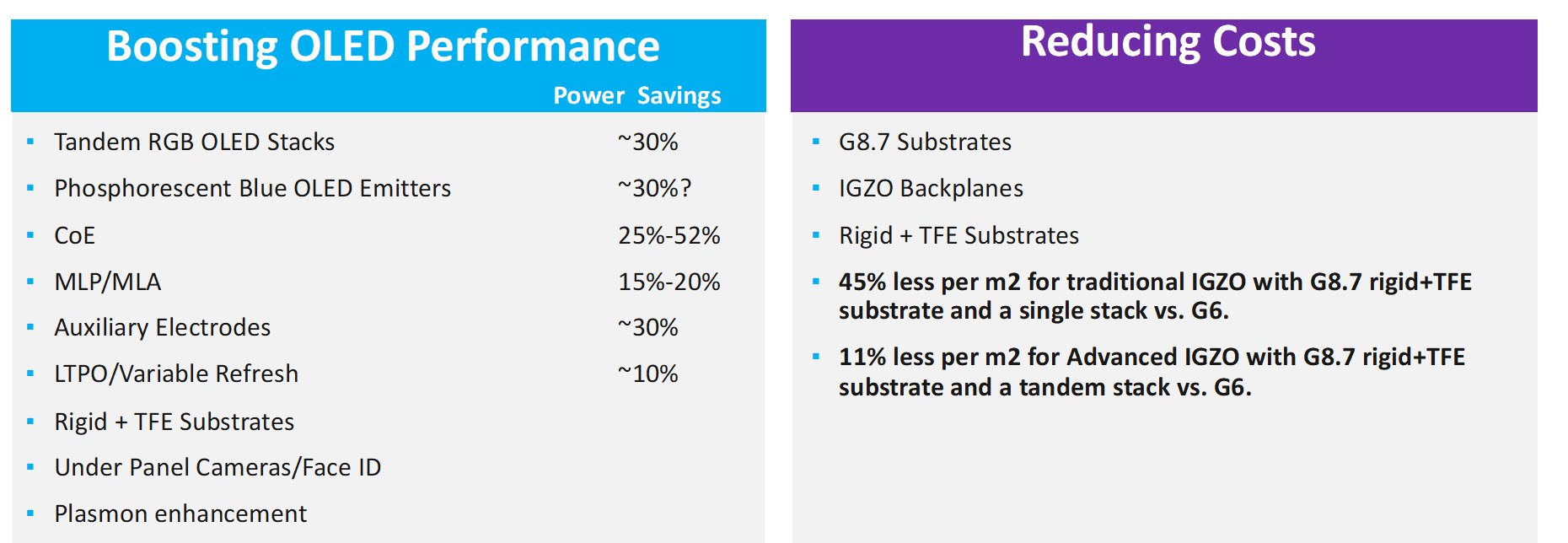

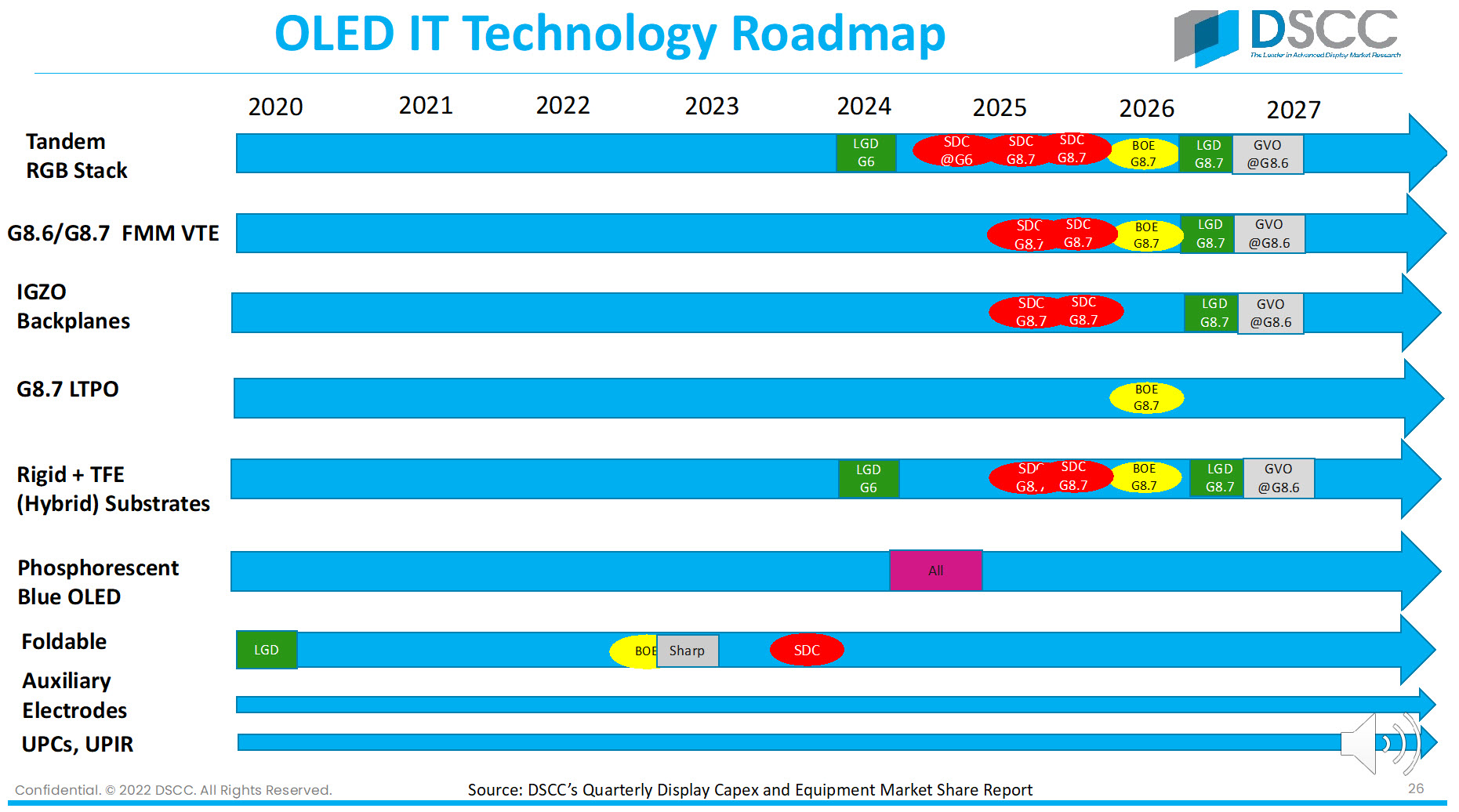

Ross Young, in his “Display Capex and Manufacturing Technology” presentation, said that big improvements are coming in OLED performance. Tandem RGB OLED stacks, Phosphorescent blue OLED emitters, color filter on encapsulation (CoE), rigid plus TFE (Thin Film Encapsulation) substrate, LTPO/Variable refresh and many other technology enhancements will boost OLED performance in future. At the same time G8.7 substrates, IGZO backplanes and rigid plus TFE will help to reduce costs.

Figure 3: Source: DSCC Quarterly Display Capex and Equipment Market Share R Figure 3: Source: DSCC Quarterly Display Capex and Equipment Market Share Report

Figure 3: Source: DSCC Quarterly Display Capex and Equipment Market Share Report

According to his presentation, from 2025 to the 2027 time frame, SDC, BOE, and LGD will have 8.7 Tandem RGB stack fabs with Rigid plus TFE (hybrid) substrate. While SDC and LGD are planning for IGZO backplanes, BOE will have LTPO backplanes. Tandem stacks are expected to provide higher efficiency, higher life time and reduced burn-in but there are challenges with higher Capex (8.7 tandem stack tools expected cost $1 billion for 15K substrates/month) and lower yields.

Rigid+ TFE substrate can also generate real cost savings by eliminating a number of process steps and equipment. Eliminating the top substrate can significantly reduce the weight and thickness vs rigid OLEDs. High mobility IGZO backplanes have many advantages, Ross explained, including low leakage, low temperature process, low off current, good uniformity, high transparency, low refresh drive, variable refresh rates, fewer masks (7 to 10), scalable to larger sizes and a single fab could address all display applications.

It also has many challenges including sensitivy to process and materials and bias stress stability which is highly sensitive to small variations in oxygen concentration. Advanced IGZO may have twice as many masks compared to traditional IGZO backplanes. According to DSCC data, LTPO at G8.7 is only 5% more cost than Advanced IGZO due to high mask counts and additional process steps in Advanced IGZO fabs. G6 has highest price per square meter. Traditional IGZO on G8.7 rigid+ TFE is 45% less per square meter. G8.7 Advanced IGZO is 11% less and G8.7 LTPO is 6% less.

The “Display Cost and Price Outlook” presentation from Yoshio Tamura gave a cost comparison of display products. In his presentation, he said

“SDC is now aggressively promoting rigid OLED for notebook PCs. In addition, Apple is said to be launching an OLED tablet in 2024 by using a hybrid RGB OLED display next to its current MiniLED product. Apple is striving for thinner, brighter and longer lifetime OLED displays with new advanced technologies such as tandem, rigid TFE and better mobility. Rigid and Hybrid OLED displays will have to compete with thinner/lighter LCDs, Oxide LCDs, LTPS LCDs and QHD/UHD LCDs especially in the high end of the notebook PC market to fill in their new G8.5 to 8.7G fabs from 2024”.

David Naranjo, in his “IT Display Market Outlook” said that 2020 and 2021 had seen a surge in units and revenue as a result of the pandemic. 2022 is estimated to see a decline of 13% Y/Y in units and 23% Y/Y decline in revenue as a result of these macroeconomic issues and weakened consumer and commercial demand. He also presented that Advanced IT displays continued to benefit from increased utilization of excess rigid capacity, more brand participation and marketing that has increased consumer awareness. According to him in 2022, although the market has slowed versus their previous estimate, DSCC expects:

- Advanced notebook PC units to increase 66% Y/Y

- Advanced monitor units will have increased 187% Y/Y

- Advanced tablet units will have increased 31% Y/Y

According to his presentation:

- For advanced Monitors: both OLEDs and MiniLEDs are expected to enjoy rapid growth, with OLEDs rising at a 91% CAGR from 2021-2026 and MiniLEDs rising at a 64% CAGR. MiniLEDs are expected to continue to lead with the majority share through the forecast period. An open cell LCD panel combined with MiniLED backlights is very cost effective versus OLED.

- For advanced notebook PCs: both OLEDs and MiniLEDs are expected to enjoy rapid growth with OLEDs rising at a 50% CAGR and MiniLEDs rising at 43% CAGR and the category rising at a 48% CAGR from 2021 – 2026. While MiniLEDs will maintain a rigid form factor, OLEDs are expected to be available in rigid, rigid + thin film encapsulation (TFE) and foldable form factors from 2023- 2024. TFE eliminates the top glass, reducing thickness and weight. From 2023, OLED is expected to have higher share.

- For Advanced Tablets: DSCC forecast OLED tablets to grow at a 46% CAGR from 2021-2026 to ~19 million units with MiniLED tablets declining at a 52% CAGR as a result of their expectation that Apple will enter the OLED tablet category with an 11” OLED tablet in 2024.

Despite the slower growth for IT applications versus their original expectations, DSCC still foresees Advanced IT displays as being poised to grow as brands offer more options with competitive price points and strong value propositions.

According to DSCC’s forecasts and outlook, the flat panel display market is expected to decline in 2022 after 2 years of growth. Technology advances in OLED, Quantum Dot and MiniLED will help suppliers to differentiate products and drive growth in Advanced TV, monitor, notebook and tablet markets. (SD)

Sweta Dash, President, Dash-Insights

Sweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact [email protected] or visit www.dash-insights.com