The Europe, Middle East, and Africa (EMEA) traditional PC market (desktops, notebooks, and workstations) surged YoY in 2020Q2 (+26.4% YoY) and totaled 20.7 million units, according to International Data Corporation (IDC). As supply and logistic bottlenecks eased up, the enormous pent up demand for notebooks (+49.0% YoY) was more than enough to offset the desktop softness (-16.1% YoY).

The Western European PC market exceeded already positive expectations with a momentous growth of 30.6% YoY, the strongest overall growth since 1998, as COVID lockdowns incurred ongoing commercial strength (+20.5% YoY) and unprecedented consumer demand (+51.2% YoY).

“2020Q2 marks the highest consumer growth ever recorded in Western Europe” said Liam Hall, senior research analyst, IDC Western Europe Personal Computing. “Lockdowns meant single device households were faced with the infeasibility of sharing ‘the family computer’ to accommodate multiple, simultaneous demands to work, study, and provide entertainment. Additional notebooks have been the key solution here, jumping 61.4% YoY, but even desktops had strong demand with +10.8% YoY growth.”

On the commercial side, growth was entirely driven by the sharp uptake of notebooks (+55.2% YoY), offsetting the heavy desktop decline (-30.4% YoY). Notebooks were undoubtedly the prominent solution used to address the exceptionally high demand to work and study from home and were further boosted by a strong backlog from Q1 due to the supply and logistic constraints in the quarter. There were still pockets of demand for desktops, for example in businesses that were confident that employees would transition full time to working from home so did not require a mobile form factor. However, high market inventory and uncertainties around employees’ future working habits led to the negative desktop performance.

Both CEE and MEA recorded an outstanding performance in the traditional PC market, especially the CEE region which outperformed any expectations and posted a growth of 29.6% YoY. The MEA region grew more modestly resulting in a 6.9% YoY increase.

“The overall PC market was driven strongly by the consumer demand coupled with tenders in the public sector and demand across the commercial sectors in general,” said Nikolina Jurisic, Senior Research Manager, IDC EMEA. “Home-schooling and home-working fueled the tremendous surge in demand, and sales-in reached 6.75 million units for two combined regions.”

In CEMA the consumer sector rose 23.5% YoY, mostly driven by notebooks (+27.5% YoY), though not exclusively as desktops also posted growth of 8.8% YoY.

“PC gaming and the need for entertainment during social distancing certainly helped the increase in desktops,” said Jurisic. “The commercial segments grew 13.2% YoY, and as expected, notebooks captured the market, reporting growth of 46.0%YoY, as companies had to meet increased demand for remote working.”

Vendor Highlights

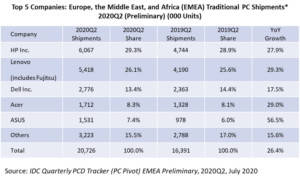

Traditional PC market consolidation continued to occur, top 5 vendors’ share growing in 2020Q2. The top 5 players accounted for 84.5% of total market volume, compared with 82.5% in 2020Q1, and 83.0% in 2019Q2.

-

HP Inc continued to lead in the EMEA PC market, posting a market share of 29.3%, rising by +0.4 pp YoY. The vendor enjoyed an increase in shipments of 27.9% YoY due to huge demand for devices for work and entertainment while staying at home.

-

Lenovo (including Fujitsu) also held its place, with the second highest market share at 26.1% (+0.5 pp YoY). Lenovo continues to grow, showcasing its ability to satisfy the strong demand across both segments.

-

Dell Inc. remained in third position and saw a market share of 13.4% — a decrease of -1.0 pp YoY. The vendor enjoyed growth for the 16th consecutive quarter, and 2020Q2 saw a 17.5% increase YoY in shipments. As has been the case for many vendors, growth has come from being able to satiate the demand for education and work equipment for those staying at home.

-

Acer regained fourth place over ASUS with a market share of 8.3% (+0.2 pp YoY). Booming consumer and gaming demand, especially around entry-level devices, alongside strong education output, saw Acer post shipment growth of 29.0% YoY.

-

ASUS fell to fifth position, after rising to fourth for a single quarter. The vendor posted a market share of 7.4% (+1.4 pp YoY). Now enjoying its third consecutive quarter of growth after 12 consecutive quarters of decline, ASUS posted a huge growth of 56.5% YoY, carried by massive consumer demand.

Table notes:

? Some IDC estimates were made prior to financial earnings reports.

? Shipments include shipments to distribution channels or end users. OEM sales are counted under the vendor/brand under which they are sold.

? Traditional PCs include desktops, notebooks, and workstations, and do not include tablets or x86 servers. Detachable tablets and slate tablets are part of the Personal Computing Device Tracker, but are not addressed in this press release.

? Data for all vendors is reported for calendar periods.