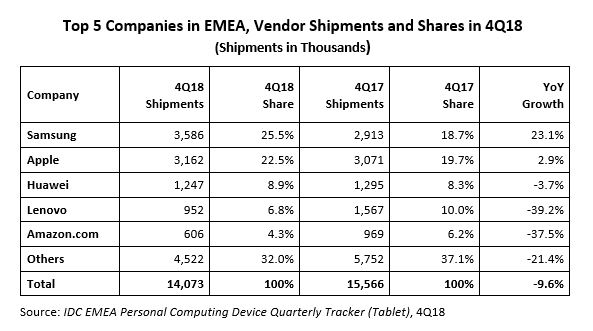

The overall tablet market in EMEA declined 9.6% YoY, shipping 14.1 million units in the last quarter of 2018 (4Q18), according to the latest figures published by International Data Corporation (IDC).

2018 closed with a 9.4% YoY drop for the region. The outlook for early 2019 remains weak and the market in EMEA is expected to decline 9.4% in 1Q19.

Plummeting tablet shipments in the region continues to be strongly driven by the erosion in consumer demand, with sales in 4Q particularly affected by a disappointing Black Friday in the Western European region.

“Prime Day was the main promotional event for this category in 2018 and this negatively impacted seasonality in the fourth quarter, as shipments were transferred to the third quarter,” said Daniel Goncalves, senior research analyst, IDC Western European Personal Computing Devices. “All major markets in Western Europe such as the U.K., Germany, France, and Italy posted strong double-digit declines in 4Q as consumers prioritized other smart connected devices at the expense of tablets.”

Western Europe declined 12% YoY in 4Q18, while Central and Eastern Europe, the Middle East, and Africa (CEMA) declined 4.6% YoY. Nikolina Jurisic, product manager at IDC CEMA, said, “Different factors are to blame for the decline, including market maturity, saturation, cannibalization from large screen size smartphones, vendors and consumers focusing on convertible products, and a lack of innovation in tablets.”

Samsung leads the company ranking in EMEA, fueled by stronger traction of the brand in the emerging CEMA markets, while Apple — number 2 in EMEA — was number 1 in Western Europe, with the more affordable iPad encouraging consumers to refresh their tablets. It also comfortably held the number 1 position in the detachable category, supported by the iPad Pro refresh last November. Huawei is third and continues to increase its footprint across the most developed economies. Lenovo has softened its push on tablet devices, while Amazon’s decline is explained by the seasonality shift into 3Q18.

IDC expects the decline to slow down throughout 2019, helped not only by more favorable YoY comparisons but also by the pickup in commercial, which is expected to return to growth in 2020. The commercial tablet market in EMEA is expected to grow at a CAGR of 3.8% to 2023.

“Digital transformation and the increasing demand for mobile solutions will eventually lead to a rebound in tablets in enterprise,” said Goncalves. “In the detachable category the products available match enterprise requirements in terms of performance, and the latest Surface and iPad Pro refreshes are a statement when it comes to the potential of such devices either as pure notebook replacements or in use cases where both mobility and keyboard capabilities are essential.”

The end of life for Windows 7 support in 2020 is expected to be a turning point for the adoption of detachables in enterprise and to boost new usage scenarios for the form factor. “The migration of the large Win 7 installed base still sitting in many large and very large corporations, particularly in the public sector, across the EMEA region, will boost the penetration of detachable solutions. It is a matter of time and, perhaps, price point adjustments,” said Goncalves.

The short-term forecast remains negative and the rollout of detachables will continue to be limited in EMEA as other macroeconomic factors take effect. “The short-term Intel CPU shortage will negatively impact Windows detachable tablets. Economic uncertainly in MEA and a weak and volatile exchange rate in Russia, coupled with economic slowdown and possible new sanctions, are expected to impact demand in the coming quarters. Nevertheless, small pockets of growth are expected in larger tablet screen sizes and in commercial in the CEMA region,” said Jurisic.

Note: Tablets are portable, battery-powered computing devices inclusive of both slate and detachable form factors. Tablets may use LCD or OLED displays (epaper-based ereaders are not included here). Tablets are both slate and detachable keyboard form factor devices with color displays equal to or larger than 7.0in. and smaller than 16.0in.

IDC’s Quarterly PCD Tracker provides unmatched market coverage and forecasts for the entire device space, covering PCs and tablets, in more than 80 countries — providing fast, essential, and comprehensive market information across the entire personal computing device market.

For more information on IDC’s EMEA Quarterly Personal Computing Device Tracker or other IDC research services, please contact Vice President Karine Paoli on +44 (0) 20 8987 7218 or at [email protected]. Alternatively, contact your local IDC office or visit www.idc.com.