According to the IDC Worldwide Quarterly Mobile Phone Tracker, 84.8 million smartphones were shipped in China in the third quarter of 2020, down 14.3% year-on-year (YoY). This was the result of multiple factors: soft demand; Huawei’s supply constraints; and delayed flagship launches from both Huawei and Apple.

“The escalated US trade restrictions in August ultimately impeded Huawei’s momentum in its home market. Nevertheless, the ban did not cool off the enthusiasm of local Huawei loyalists that supported Huawei’s market share to stay above the 40% mark,” says Will Wong, Research Manager for Client Devices at IDC Asia/Pacific.

{kind=link}

|

China Smartphone Market, Top 5 Company Shipments, Market Share, and YoY Growth, Q3 2020 (shipments in millions) |

|||||

|

Company |

2020Q3 Shipments |

2020Q3 Market Share |

2019Q3 Shipments |

2019Q3 Market Share |

YOY Growth |

|

1. Huawei |

35.1 |

41.4% |

41.5 |

42.0% |

-15.5% |

|

2. vivo |

15.0 |

17.8% |

18.1 |

18.3% |

-16.9% |

|

3. OPPO |

14.1 |

16.6% |

16.4 |

16.6% |

-14.2% |

|

4. Xiaomi |

11.0 |

13.0% |

9.7 |

9.8% |

13.4% |

|

5. Apple |

7.0 |

8.3% |

8.1 |

8.2% |

-13.1% |

|

Others |

2.5 |

3.0% |

5.0 |

5.1% |

-49.6% |

|

Total |

84.8 |

100.0% |

98.9 |

100.0% |

-14.3% |

|

Source: IDC Quarterly Mobile Phone Tracker, 2020Q3 |

|||||

|

Note: All figures are rounded off |

|||||

2020Q3 Top 5 Smartphone Vendor Highlights:

-

Huawei cautiously managed its shipments across its product lineups and lowered the production of some popular models like the Mate 30 series. Its channel management and prioritization also resulted in a supply shortage in the lower-tier cities, delaying purchases from loyal customers.

-

vivo put more focus on various consumer segments at different price points and recorded a narrower decline from a year ago. The vendor continued to penetrate the <US$300 segment with the 5G-enabled Y-series while enhancing its positions in the mid-range and high-end segments with the new S7 and iQOO 5 series as well as the X series flagship.

-

OPPO narrowed its decline from a year ago by focusing on the US$200-400 5G segment. Furthermore, the vendor shipped less in the <US$150 segment as some old models neared the end of their life cycles.

-

Xiaomi was the only top 5 vendor that saw growth from a year ago as its Redmi 9 and K30 series were well-received – especially in the higher-tier cities. The vendor’s new mid-range and high-end models also garnered a favorable word-of-mouth effect, and it sped up its offline channel expansion to support its growth.

-

Apple’s delayed iPhone 12 launch resulted in lower shipments compared to the same period last year. Nevertheless, Apple managed to mitigate the shortfall with its iPhone 11 series, as the models still performed well in both online and offline channels and will continue to be promoted in the upcoming Singles’ Day shopping festival.

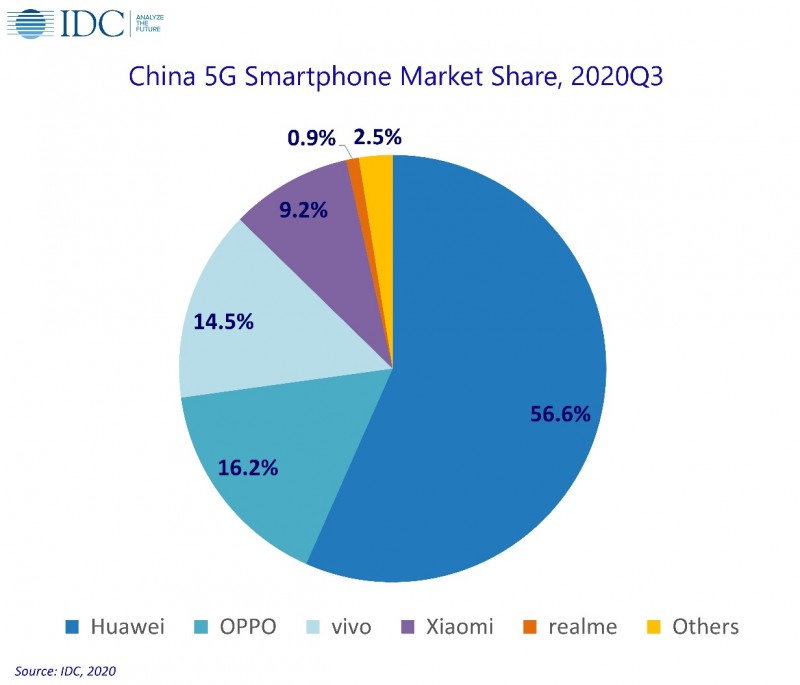

China has so far shipped a total of 117 million 5G handsets since 2019, with 49.7 million in 2020Q3 alone. Huawei continued to lead the 5G market, while OPPO and vivo remained in the second and third spots respectively – mainly supported by their <US$300 5G products. Xiaomi ranked fourth, followed by realme, which launched several new 5G models in September in both online and offline channels.

“External factors such as political risk could spur a possible reshaping of the market as well as an opportunity for growth and expansion. Therefore, having a contingency strategy as part of one’s business expansion initiatives will be crucial for vendors and their business partners to deal with any unfavorable changes,” says Xi Wang, Research Manager for Client System Research at IDC China.