Chinese companies shipped 9.54 million wearable devices in the second quarter of 2016, an increase of 13.2% from the previous quarter and up 81.4% from a year earlier, according to IDC’s China Wearable Device Market Quarterly Tracker report. Shipments of basic wearable devices such as wristbands, children’s watches and smart running shoes grew by 92.1%, while smart wearables led by smartwatches were up by 3.4% from a year earlier.

“Unlike basic wearable products in overseas markets where fitness tracking is their main function, basic wearable devices in China are of much richer product forms and offer more functionality. This has enabled the fast expansion of China’s basic wearable device market,” said Jean Xiao, research manager at IDC China. “Meanwhile, unlike their international counterparts, China-based vendors have a more profound understanding of local market segments. Cost-effective products and precisely targeted marketing and sales strategies appeal to Chinese consumers more easily.”

The rapid growth in China’s wearable device market has largely been due to local vendors’ ability to adapt quickly and cultivate new market segments intensively. This is reflected in the following aspects:

Product focus shifts from hardware to software.

Be they makers of fitness wristbands such as Xiaomi and Lifesense or children’s watches like Okki and 360, vendors focused initially on improving the hardware performance of their products. However, after the market took shape in 2015, vendors gradually shifted their focus towards developing wearable device applications and software platforms. For example, the product function of children’s watches has gradually evolved from a location-positioning device to meet parents’ safety needs into a mobile device that offers social networking, entertainment and interaction for kids.

Functionality expands in new wearable ranges.

China-based vendors have also gradually changed from making small-scale exploratory innovation in wearable device functions to translating such innovation into essential functions for most products. Following the pioneering launch of public transit payment wristbands in 2015, payment has now become an indispensable function of China-made wearable devices. Whether it is payment through NFC or by way of QR code scanning on APP installed on smartwatches, by supporting mobile payment on wearable devices, China-based vendors have become both pioneers and bellwethers in the wearable payment field. In 2016 Mobvoi and Huami were the first China-based manufacturers to introduce offline music storage to their smartwatch ranges. This is set to become the next major function for new wearable devices.

Channel coverage developed from isolated spots to full-platforms.

In 2015, wearable device vendors opted for single e-commerce platforms to launch their new products. The picture changed in 2016 when more vendors opted to sell their products on both online and offline platforms. Consumers now have such a mature understanding of wearable devices that traditional channels such as retail outlets have to stock emerging smart hardware to attract new user groups. This means that vendors with product and brand advantages are gradually gaining the upper hand across the market. Full-platform channel management will also pose a test to vendors’ overall strength.

Market expands from domestic to overseas.

After the success of the Xiaomi wristband in India and other overseas markets, more and more China-based wearable device vendors started to enter overseas markets in 2016. Through the US crowd-funding website Kickstarter, Mobvoi amassed a total of over $2 million from 9,955 people in one month, making it the top-ranking smartwatch under the category of wearable device on the website. Similarly, China-based wristband vendor, Bong, won an order for 3.8 million sport wristbands from a subsidiary of Thailand Telecom. The drive by China-based vendors into overseas markets is gradually winning them an increasing share of the global wearable device market.

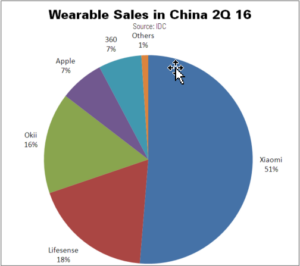

“Having withstood the test of fierce competition in the rapidly expanding home market, China-based wearable device vendors represented by Xiaomi, Lifesense and Okii have accumulated considerable strengths in product functionality, software technology and channel strategy and have become a force to be reckoned with in the global wearable device market, “Jean Xiao said. “Emerging wearable device startups represented by Mobvoi and Bong have also started to win their place in overseas markets. IDC believes that China-based wearable device vendors will move further ahead in this field.”

|

IDC: China wearable device shipments by vendor, 2Q16 (K units) – Top 5 Vendors |

|||||

|

Vendor |

2Q16 shipments |

2Q16 market share |

2Q15 shipments |

2Q15 market share |

Y/Y |

|

1.Xiaomi |

2,869 |

30.1% |

2,750 |

52.3% |

4.3% |

|

2.Lifesense |

1,033 |

10.8% |

0 |

0 |

N/A |

|

3.Okii |

875 |

9.2% |

0 |

0 |

N/A |

|

4.Apple |

382 |

4% |

391 |

7.4% |

(2.3%) |

|

5.360 |

373 |

3.9% |

257 |

4.9% |

45.1% |

|

Others |

4,008 |

42% |

1,862 |

35.4% |

115.3% |

|

All |

9,540 |

100% |

5,260 |

100% |

81.4% |

Source: IDC China Wearable Device Market Quarterly Tracker