LCD TV panel capacity has increased substantially in 2019 mostly due to the expansion of Gen 10.5 fabs. After growth in 2018, LCD TV demand weakened this year caused by slower economic growth, concerns about a trade war and tariff rate increases. Capacity expansion and higher production combined with weaker demand have resulted in considerable oversupply of LCD TV panels in 2019 leading to drastic panel price reductions.

Some panel prices went below cash cost by the end of Q3, forcing suppliers to cut production and delay expansion plans to reduce losses. What will be the implications for the industry in the holiday season and 2020? Can these very low panel prices help to drive TV demand?

Intense expansion of LCD TV panel capacity

Massive 10.5 Gen capacity that can produce 8-up 65″ and 6-up 75″ panels from a single mother glass substrate are coming to display market in the next three years. The trend already started in 2018 as BOE started its a-Si TFT LCD Gen 10.5 fab from the first quarter. It ramped up to its full capacity in the first half of 2019. China Star (CSOT) also started its a-SI TFT-LCD Gen 10.5 fab also in the first half of this year, focusing on 65″ and 75″ TV panels. There were also increases in capacity from other gen 8.5 fabs. Foxconn/Sharp’s Gen 10.5 fab was also expected to start in 2019, with full production ramp up in 2020, but it has been delayed now.

By the year 2021 and 2022 about eight to ten 10.5 Gen fabs with huge capacity are expected to be in production. Fear of panel oversupply is looming even larger for future years. With considerable growth in capacity and the entrance of new panel suppliers and TV brands, competition has accelerated with intense price pressure. Capacity expansion in 2019 combined with low TV demand has pushed the market in severe oversupply situation in the second half of 2019.

Fear & Uncertainty lead to slower TV demand

Fear and uncertainties due to the rade war between the US and China and an expected tariff increase in Q3 2019 pushed TV brands to move panel orders to earlier in the first half of the year. Weaker TV set sales led to an inventory build-up by the end of Q2. Also fear of TV price increases due to tariffs, reduced the second half outlook suggesting reduced panel demand and increasing inventories also on the panel side. Panel prices also started to decline.

By Q3 2019, too much capacity was chasing too little demand pushing the market to oversupply. Fierce competition has led to drastic panel price reductions, pushing prices below even cash cost for some products. Panel suppliers’ financial results suffered in Q3 as many lost money. Suppliers from China, Korea and Taiwan all started lowering utilization rates by the end of Q3 to reduce oversupply and in the hope of stabilizing panel price. Very low prices combined with lower utilization rates is making the revenue and profitability outlook for panel suppliers difficult in Q4 2019.

Vizio 55 inch Class M-Series Quantum 4K Ultra HD (2160p) HDR Smart TV (m556-g4) (2019 Model), Black $398.00 (Source:Walmart)

Vizio 55 inch Class M-Series Quantum 4K Ultra HD (2160p) HDR Smart TV (m556-g4) (2019 Model), Black $398.00 (Source:Walmart)

Suppliers forced to cut production as price dipped below cost

BOE and China Star have cut utilization rates of Gen 10.5 fabs. Sharp has delayed the start of production at its 10.5 Gen fab by six months and plans to start in 2020. LGD and Samsung display already decided to shift away from LCD more towards OLED and QDOLED respectively. Both companies are cutting utilization rates in their 7, 7.5 and 8.5 Gen fabs. Taiwanes suppliers are also cutting 8.5 Gen fab utilization rates.

According to industry data some panel suppliers are already cutting utilization rates below 50 to 60% for their Gen 8.5 fabs. And Chinese suppliers are cutting their fab capacity by 20% to 25%. Some have shifted capacity away from TV to other applications. In summary, drastic price reduction has resulted in cut in utilization rates, delay in fab construction and ramp ups and closing down of older fabs, or conversion to OLED or QDOLED fabs. This can help to reduce oversupply. Still there is a need for an increase in demand especially for larger size TV to absorb the massive LCD capacity.

Samsung – 65″ Class – LED – NU6900 Series – 2160p – Smart – 4K UHD TV with HDR Price $479.99 (Source BestBuy.com)

Samsung – 65″ Class – LED – NU6900 Series – 2160p – Smart – 4K UHD TV with HDR Price $479.99 (Source BestBuy.com)

The Suppliers’ pain is consumer’s gain; lowered price TV

There were real concerns about TV set price rises in 2019 due to a fear of a trade war and tariff increases. Drastic reductions of panel price could help to reduce TV set price. Some indications have already been seen in early version Black Friday sales offerings in the U.S. market. Walmart started its deals early. For example, Walmart is offering a Vizio 55″ class M series quantum dot 4KUHD HDR TV for a super low price of $398 pushing it below the $400 threshold.

Target is offering a Philips 55″ UHD smart TV for less than $250. Best Buy is offering an LG 65-inch 4K UHD TV for less than $500. These are super low prices mostly as ‘door busters’ or in limited quantities. In general, black Friday TV prices seem aggressive. High inventories, oversupply and low panel prices have led to these low prices. Due to competitive pressure LG has also reduced its OLED TV price aggressively – LG 55″ 4 K Smart TVs are at below $1300. Sony’s 65″ UHD OLED is being offered at $2000. As it can be seen OLED is still three times higher in price compared to quantum dot TVs. Going forward, aggressive TV set retail prices enabled by low panel price could help to drive demand.

LG OLED65C9PUA Alexa Built-in C9 Series 65″ 4K Ultra HD Smart OLED TV (2019) by LG – Price $2,096.99 (Source Amazon.com)

LG OLED65C9PUA Alexa Built-in C9 Series 65″ 4K Ultra HD Smart OLED TV (2019) by LG – Price $2,096.99 (Source Amazon.com)

Capacity Expansion – Price reduction – Demand creation

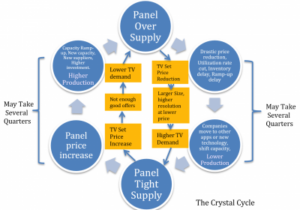

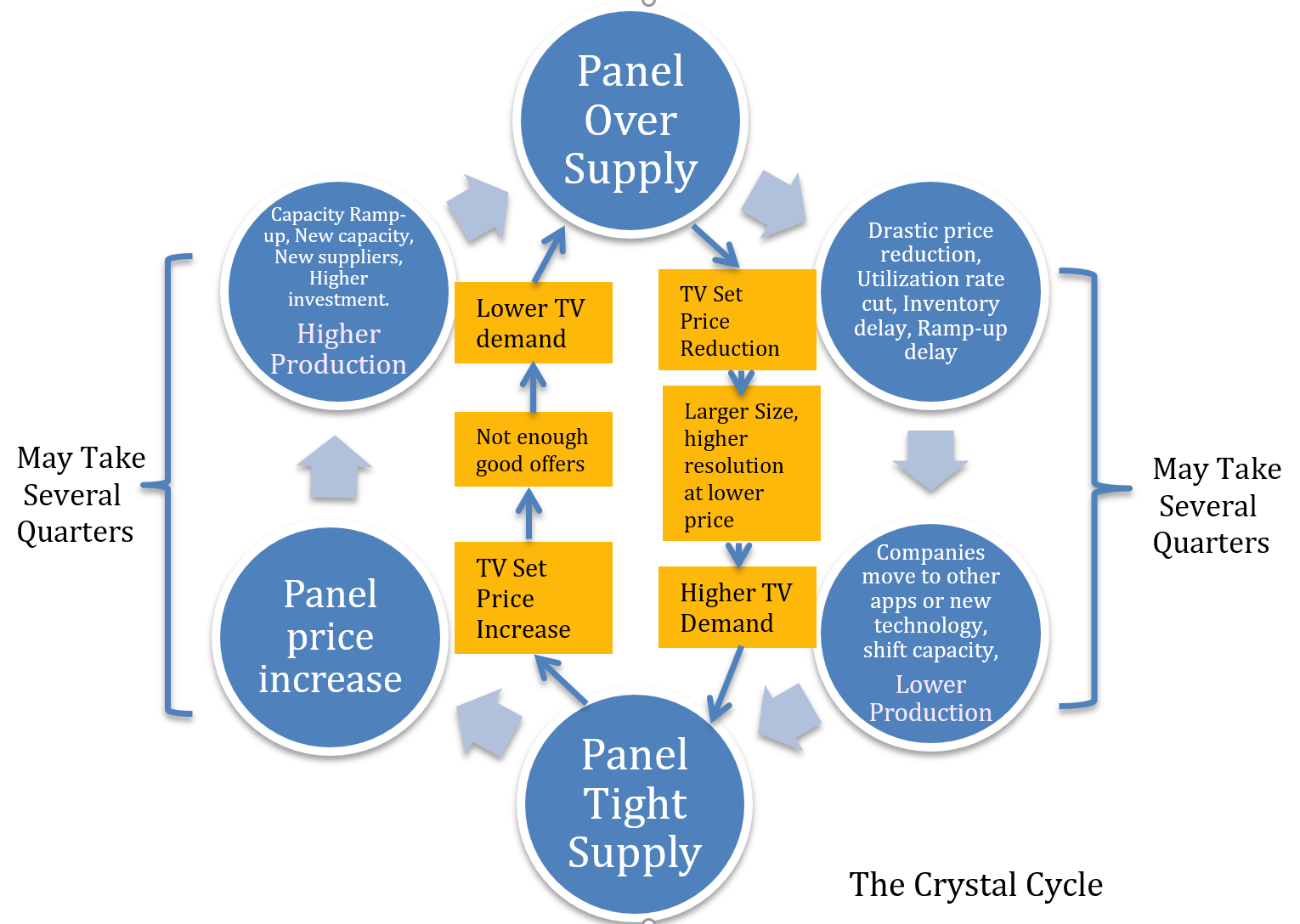

The history of LCD industry has shown that the industry follows a strategy of capacity expansion, price reduction and demand creation to drive application market growth. This strategy has resulted in periodic cycles of oversupply (some call it the Crystal Cycle) that pushes price to below cost level. Then production cuts, investment delays and increases demand due to low prices push the industry back to tight supply and increased prices. There is a time lag between each stage and between oversupply and tight supply. That creates heavy collateral damage for suppliers leading to loss of revenue and profitability.

In extreme over-supply situation, only a few companies with strong financial strength and commitment to LCD can survive. Others have to move away to other new technologies or shift to specialty type applications away from the commodity markets. In the last 20 years, there are plenty of examples in the LCD industry of this change. This capital-intensive industry requires billions of dollar-investments with uncertain outlook.

The LCD Crystal Cycle (Source – Dash-Insights) Click for higher resolution

The LCD Crystal Cycle (Source – Dash-Insights) Click for higher resolution

Implications for the Industry

Panel over-supply (by bringing down panel prices to way lower level than what is possible through cost improvement) can help to drive demand in many different ways.

- Drive holiday sales with very aggressive black Friday deals, Cyber Monday and other holiday deals with low TV set prices

- Low price trend can continue in Q1 for the US Super Bowl and for the Chinese New Year sales

- Increased panel demand in the first half of 2020 due to preparation for the 2020 Olympics

- Increased shares for Quantum dot TVs during the holidays and 2020 by bringing prices down to the mainstream consumer level

- Increased sales for OLED TV due to lower prices

- Increase LED LCD TV sales due to low prices

- Shift to larger size (above 50-inch especially to 65-inch) and higher resolution (4K and 8K) and better performance (HDR, WCG) due to lower costs .

For the industry there can be many implications.

- Industry restructuring with change in market shares of top leaders

- Shift in regional shares (China share increasing)

- Suppliers moving away from TV applications more towards value-based specialty applications

- Suppliers shifting faster to new technology – Samsung QD-OLED or QD LCD, LG shifting more to OLED, China suppliers also focusing more on OLED and quantum dots

- Cancellations, delays in investment, and utilization rate adjustments

Lower panel prices can help TV set holiday sales demand by reducing retail prices. a trend that could even spill over to 2020. If panel capacity comes back too soon, it may reduce the opportunity to drive TV demand. Panel suppliers have to navigate a delicate balance of capacity management to capture the opportunity for higher TV demand. – Sweta Dash

Sweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact [email protected] or visit www.dash-insight.com