LCD TV panel prices have been declining since July 2021 and the trend is expected to continue throughout Q2 2022. With an improvement in the Covid19 situation and a shift away from STH (Stay-at-home) and WFH (Work-from-home) policies, market demand for TVs, monitors and notebooks are all forecast to be lower in 2022 compared to 2021.

At the same time, panel makers’ fab utilization rate cuts were very moderate in recent months according to industry data. Further price reductions for TV panels will push prices to below cash cost level; thereby forcing panel suppliers to intensify fab utilization rate cuts to reduce production. The recent lockdowns in China to control Covid are starting to impact factory and component production. If LCD TV set prices can reflect the cost savings for set makers from panel price reductions in the past quarters, it could help to improve demand for set. With lower production and better demand, TV panel prices could stop declining in 2H2022.

TV Panel Price Reduction continuing

According to a DSCC blog in April by Bob O’Brien,

“the potential for a negative impact on global TV demand from Russian war in Ukraine combined with high inventory levels suggest continued price pressure in Q2. Prices have declined dramatically from their peaks in mid-2021 but supply has continued to be robust throughout the first quarter and to start the second. Prices cannot fall much further before they are below cash costs, but there are no obvious drivers of demand, and demand uncertainty has been heightened by the war in Ukraine”.

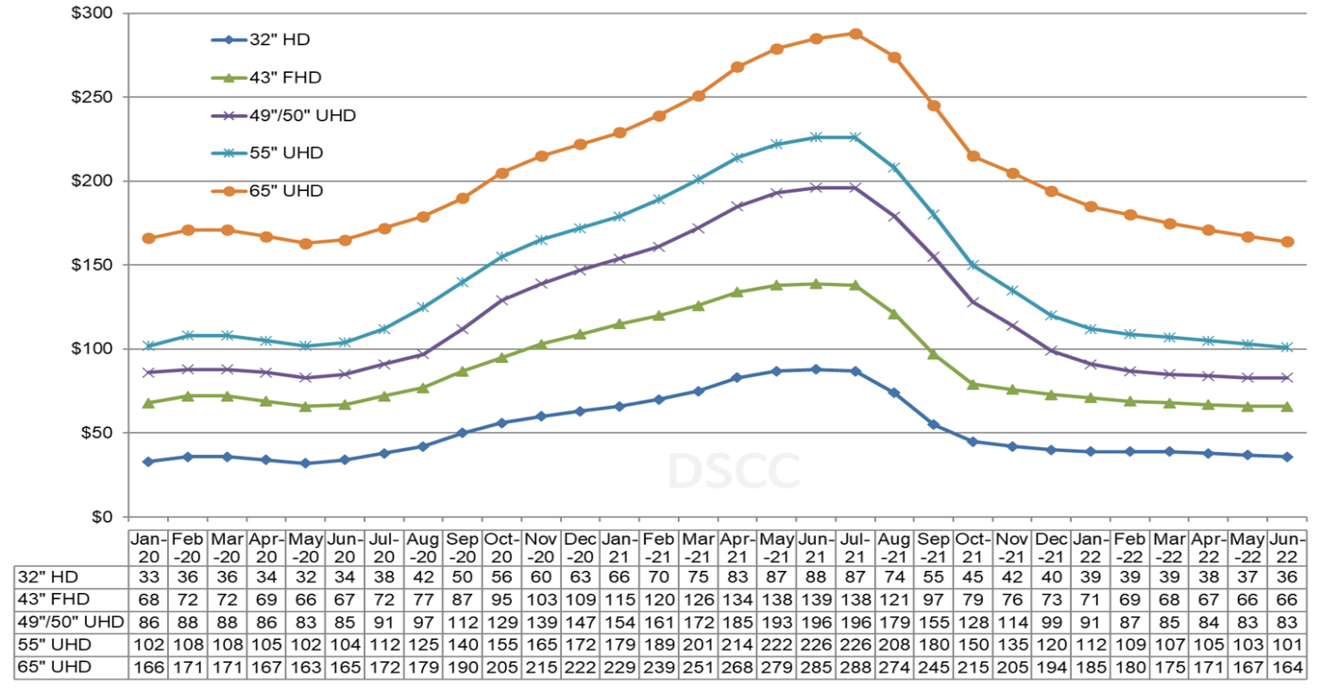

The chart below highlights DSCC’s latest TV panel price update in April, showing both

- the biggest price increases in the history of the flat panel display industry, from mid-2020 to mid-2021 and then

- the fastest price decreases in the autumn of 2021. The fourth quarter of 2021 saw the biggest Q/Q price declines in the history of the flat panel display industry.

LCD TV Panel Prices January 2020-June 2022

Source: Displaysupplychain.com April 4th, 2022

Source: Displaysupplychain.com April 4th, 2022

According to DSCC’s blog,

“Despite the signals of weak demand, panel maker utilization remained high in Q1’22 and appears to be continuing at a high level. The industry appears to be building inventory at a rate that is unsustainable, and past experience suggests that price declines will continue until prices fall below cash costs”.

Uncertainty leads to lower TV demand

Large LCD panels saw dramatic increase in prices in the first half of 2021 due to unprecedented tight supply that was impacted by component shortages and strong demand both in TV and IT market. Tight supply and extremely high panel prices resulted in high LCD TV set prices. Softness in demand (due to higher set prices and improvements in the COVID 19 situation globally) combined with supply expansion lead to panel price reductions in 2H 2021. The Russia and Ukraine war, high oil price, inflation, higher interest rates in US, supply chain issues and uncertainties about second half of 2022 are all leading to further cuts in demand forecasts for 2022. LCD TV set prices are still at a higher level.

According to the April 2022 PriceWise publication by Omdia.

“Some major retailers and TV makers have been turning bearish and disappointed about TV sell-through results in recent months. They are concerned if they can smoothly clear their higher-than-normal inventories on hand during this challenging period. Therefore, they are pressured to either lower or delay TV shipments in the coming months, although they foresee logistic issues, such as port congestion, in-land transportation, and China’s zero-Covid policy, to continue disrupting their supply chain planning for this year”.

According to the publication,

“top TV makers Samsung and LG Electronics made another order cut in April, lowering purchasing plans for 2Q22; panel makers have to offer more price concessions in 2Q22. Expectations of price stabilization are diminishing for 32- and 43-inch panels, while 65-, 75-, and 85-inch panel prices are plummeting. After a drastic order cut in March and April, Samsung intends to strongly refill more panels from this June and 3Q22 onward to materialize its TV business plans for 2022”.

Traditionally, Q3 is the season for higher panel demand, as brands get ready for stronger sales in the holiday season. War, Inflation, global and macroeconomic uncertainties this year have impacted the large LCD panel market outlook.

Higher TV set price impacting demand

Higher TV set prices will impact demand. QLED- and MiniLED-based LCD TV compete with OLED TV in the premium market. With LCD panel price increases and set price increases the cost gap between LCD and OLED TV went down in 2021. LG Displays also implemented major capacity expansion of OLED TV panels with its Gen 8.5 fab in China. New product sizes, higher productions and cost reductions helped OLED TV to gain unit market share in the premium TV market. Also new QD OLED TVs from Samsung and Sony are now entering the market in 2022. If LCD TV panel price reductions can be reflected in set price reductions it will help to make QLED and MiniLED TV more competitive in the premium market. The major panel price reductions for LCD TV have not been reflected in set prices up to now.

According to a TrendForce publication in April, 2022,

“Due to issues in 2021 such as the shortage of cargo containers and port congestion, shipping costs spiked, indirectly inflating the production cost of TV sets. Before the pandemic, shipping costs on a 65-inch TV was US$9. Last year, this jumped to US$50-US$100, scaling with TV size. Even though current TV panel pricing has plunged by 30% to 40% compared to last year’s peak, the fact that freight costs are not expected to improve in 2022 will inevitably affect TV brand promotions and scale of stocking during the peak season of overseas markets in 2H22”.

TrendForce has also revised its TV shipments forecast downward for 2022.

Supply Side Impact can Shift the Balance

Lockdowns in China to control Covid19 are starting to impact factory output and component supply. According to an Omdia publication in April,

“HMO, the second polarizer supplier in China, has two lines located in Kunshan, mainly producing TV polarizers. However, because of the rapid spread of COVID-19 in nearby Shanghai, the entire city of Kunshan went into lockdown from April 6. HMO mainly supplies polarizers for large TV panels and provides polarizers to most Chinese panel makers, including CEC-Panda, CHOT, China Star, HKC, and SIO. Since most panel makers have about two weeks of polarizer inventory, the lockdown in the Kunshan area has not immediately impeded panel production. However, if the lockdown is longer than the original schedule, the HMO inventory held by panel makers could run out by mid-April. Moreover, HMO’s inventory of subfilms is short as ports are closed. Assuming that the polarizer supply is stopped for April, the TV panel production area may decrease by over 5% in the second quarter of 2022”.

Supply issues could also increase polarizer price. Further panel price reductions in Q2 2022 could push prices to below cash cost level forcing panel suppliers to cut LCD fab utilization rates. A supply side adjustment would shift LCD supply demand balance to be tighter.

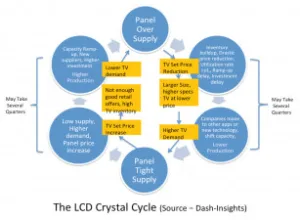

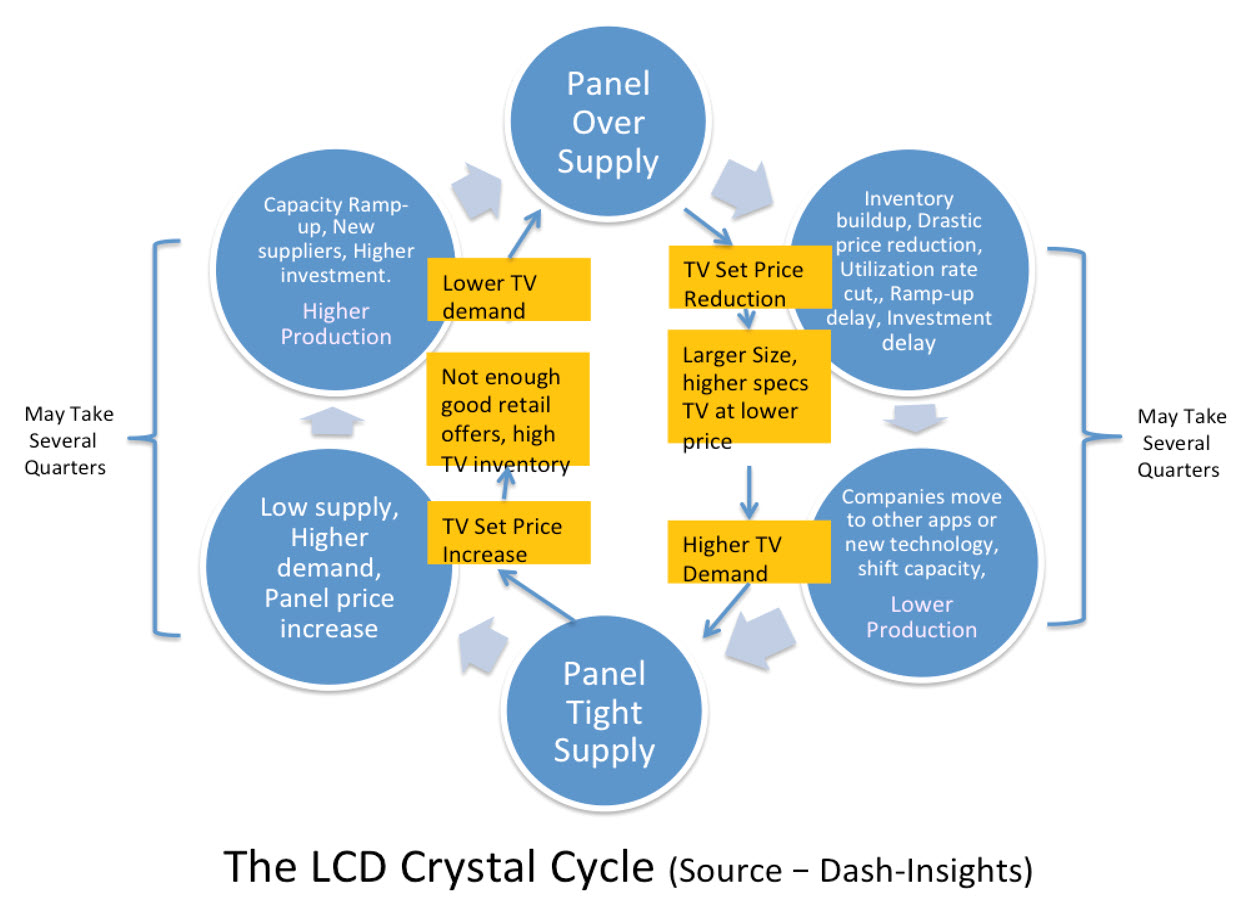

Capacity expansion ? Price reduction ? Demand creation

The history of LCD industry has shown that the industry follows a strategy of capacity expansion, price reduction and demand creation to drive application market growth. This strategy has resulted in periodic cycles of oversupply (some call it the Crystal Cycle) that pushes price to below cost level. Then production cuts, investment delays and increases in demand due to low prices push the industry back to tight supply and increased prices. There is a time lag between each stage and between oversupply and tight supply. That creates heavy collateral damage for suppliers leading to loss of revenue and profitability.

It seems that at the moment, the market has reached towards the end of the “down cycle”. In the “down cycle” when prices decline, panel buyers delay purchases and keep lower inventories to avoid holding higher cost inventory, resulting in a further reduction in demand.

If the supply side can be adjusted by production cuts and set prices can be reduced to reflect panel price reduction costs savings, LCD TV panel demand could improve in the second half of 2022 and stop panel price decline. (SD)

Sweta Dash, President, Dash-Insights

Sweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact [email protected] or visit www.dash-insights.com