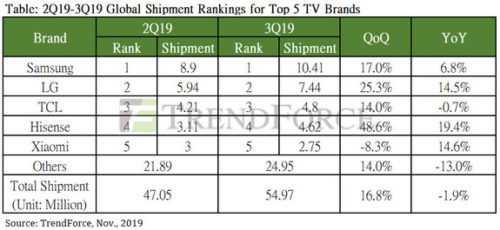

The latest analysis from the WitsView research division of TrendForce shows that global TV shipment in 3Q19 reached 54.97 million units, a 16.8% growth QoQ and 1.9% decline YoY. As China-U.S. trade relations worsened in 2Q19, TV brands took on a speculative attitude towards stocking-up. This attitude completely changed with the imminent arrival, towards the second half of 3Q19, of Double 11 in China and year-end festivities in Europe and the Americas, which are both shopping holidays that require companies to stock up.

Not only did TV brands actively ramp up their shipments, but they also hoped to make up for lost sales in 1H19 through large-scale sales promotions.

According to TrendForce research manager Iris Hu, as brands stock up in preparation for year-end sales, 4Q19 shipment is projected to reach 65.42 million units, a 19% growth QoQ. After the sales prices across all panel sizes dropped below cash costs, panel manufacturers began reducing the production volume of panels in order to establish a price floor in 4Q19. Stabilized low prices of TV panels are expected to help brands plan their sales strategies.

Nonetheless, the TV market is impacted by tariffs-related problems stemming from the China-U.S. trade war. In addition, the Chinese market is increasingly saturated, and Chinese customers have become less and less reliant on TV sets. Even in light of Chinese brands’ active expansion into overseas markets, total TV shipment in 2019 is expected to decline by 1% YoY.

Samsung’s Effective Pricing Strategy Doubles Its Shipment Share of QLED TVs

The first two places in terms of 3Q19 shipment were still occupied by Korean brands. Market leader Samsung increased the market share of its QLED products by adopting consumer-friendly prices. Samsung’s shipment of QLED TV in 2019 broke the 5-million-unit mark for the first time and occupied 2.5% of the market, doubling the previous year’s shipment share. In total, Samsung reached 10.41 million TV units, a growth of 17% QoQ and 6.8% YoY.

On the other hand, LG Electronics (LGE), also based in Korea, notched shipment numbers of 7.44 million units in 3Q19, a 25.3% growth QoQ and 14.5% growth YoY. Because most of LGE’s TV panels were supplied by LG Display, and because it assembled its TV sets in-house, LGE was able to achieve strong cost advantages, which translated into strong competitive advantages in the peak sales season.

As TCL and Hisense Actively Pursue Overseas Markets, Xiaomi Looks for a Resurgence in Shipment via Low Prices

As the domestic demand in China became saturated, and Xiaomi aggressively pursued market share starting from 2018, the two largest Chinese brands TCL and Hisense quickly shifted their sales focus onto the international market. TCL began exporting its products overseas since the beginning of 2019, with remarkable performances in North America, Europe, Latin America, and other emerging markets. The company saw weak shipment numbers in 2Q19 due to uncertainties caused by the China-U.S. trade war and an inflated shipment base period from preemptively stocking up in 1Q19 at the expense of 2Q19 shipment. However, orders from overseas markets came in droves in 3Q19, driven by the arrival of peak season. This, combined with TCL’s stocking up in August in preparation for Double 11, secured the company a 4.8 million unit shipment, a 14% growth QoQ, and a third-place global TV brand ranking.

Hisense is continuing to expand its overseas market this year to include Australia, Europe, and Russia. The company’s exported products currently occupy 50% of its total product shipment. Thanks to the rising demand in both the domestic and overseas markets in 3Q19, Hisense reached an all-time high (for the company) shipment of 4.62 million units, a 48.6% growth QoQ.

Fifth-place Xiaomi traditionally offered a lineup of highly cost-effective products to bolster its customer loyalty and increase market share. Nevertheless, its performance during the 618 shopping festival in 1H19 did not meet prior expectations. Xiaomi’s stocktaking in 3Q19 indirectly reduced its shipment by 8.3% to reach 2.75 million units. The company aims to engage in an aggressive pricing strategy in 4Q19 to attract customers and generate a resurgence in shipment.