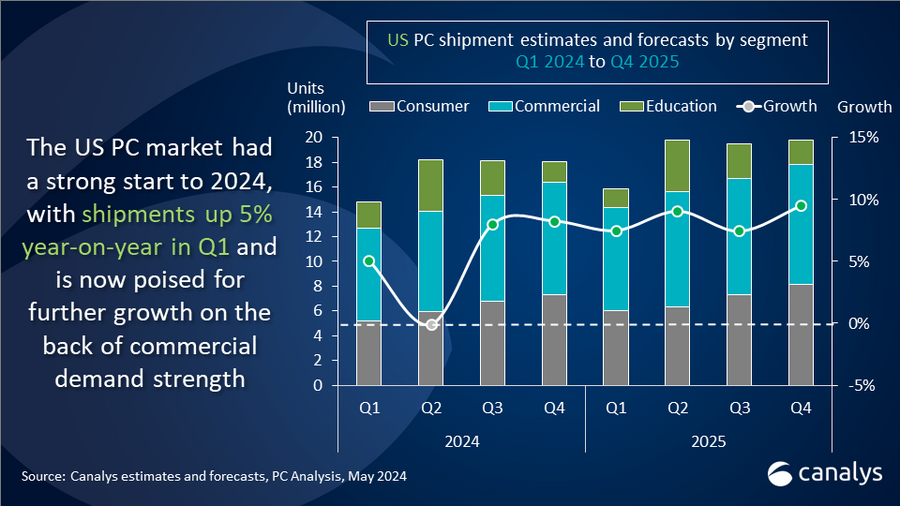

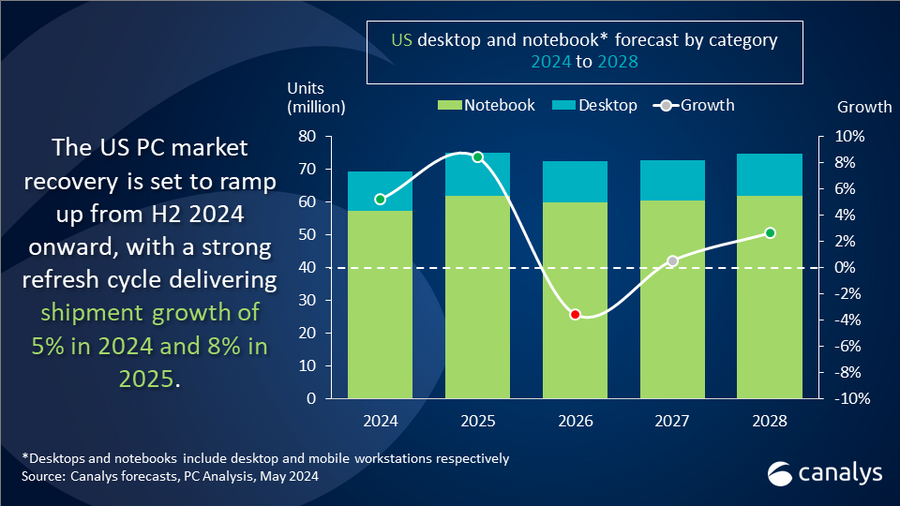

In Q1 2024, PC shipments in the US (excluding tablets) grew by 5% year-on-year, reaching 14.8 million units. The consumer and small-medium business (SMB) segments were the primary drivers of this growth, each experiencing shipment increases above 9% year-on-year. This strong start to the year indicates a healthy recovery trajectory for the market, supported by the ongoing Windows refresh cycle. Total PC shipments in the US are expected to reach 69 million units in 2024 and grow by another 8% to 75 million units in 2025.

Source: Canalys

The consumer segment demonstrated the best performance for the third consecutive quarter, largely due to continued discounting after the holiday season, which boosted consumer demand. The commercial sector also showed improvement, particularly among SMBs, indicating the start of the anticipated refresh cycle driven by the end-of-life for Windows 10. This positive performance suggests that enterprise customers are likely to follow suit, contributing to a highly positive near-term market outlook.

Source: Canalys

Stable macroeconomic conditions in the US have resulted in healthier consumer spending and increased business investment in IT. The market is expected to gain further momentum over the next four quarters, coinciding with the greater availability of on-device AI capabilities. New products and user experiences are set to excite both consumers and businesses, driving the adoption of AI-capable PCs within the Windows and Apple ecosystems. Greg Davis, an analyst at Canalys, emphasized that the US is forecasted to lead in the adoption of these advanced devices as vendors and their partners focus on upgrading customers to premium AI-enabled devices, capitalizing on the significant market opportunity.

US Desktop and Notebook Forecast (Units in Thousands)

Segment

2023 shipments

2024 shipments

2025 shipments

2024 annual growth

2025 annual growth

Consumer

25,351

25,236

27,785

-0.5%

10.1%

Commercial

27,183

29,313

32,475

7.8%

10.8%

Government

3,817

3,877

4,211

1.6%

8.6%

Education

9,424

10,766

10,527

14.2%

-2.2%

Total

65,775

69,192

74,998

5.2%

8.4%

Source: Canalys

US Tablets Forecast (Units in Thousands)

Segment

2023 shipments

2024 shipments

2025 shipments

2024 annual growth

2025 annual growth

Consumer

33,840

34,688

36,344

2.5%

4.8%

Commercial

6,323

6,554

7,204

3.7%

9.9%

Government

484

439

371

-9.3%

-15.3%

Education

1,936

1,987

1,975

2.6%

-0.6%

Total

42,583

43,668

45,894

2.5%

5.1%

Source: Canalys

US Desktop and Notebook Shipments (Market Share and Annual Growth – Units in Thousands)

Vendor

Q1 2024 shipments

Q1 2024 market share

Q1 2023 shipments

Q1 2023 market share

Annual growth

HP

3,639

24.6%

3,733

26.6%

-2.5%

Dell

3,596

24.4%

3,801

27.0%

-5.4%

Lenovo

2,594

17.6%

2,119

15.1%

22.4%

Apple

2,102

14.2%

1,723

12.3%

22.0%

Acer

811

5.5%

787

5.6%

2.9%

Others

2,024

13.7%

1,890

13.4%

7.1%

Total

14,766

100.0%

14,053

100.0%

3.3%

Source: Canalys

US Tablet Shipments (Market Share and Annual Growth – Units in Thousands)