Tenet painfully clawed itself to maybe $80M in ticket sales in the US and perhaps $400M globally while most major projects were slid into next year or worse, slipped into various D2C options. Studios and all but the most ardent theater goers said, “You know that I love you … I just don’t like you very much right now.” And getting liked is getting even more difficult for cinemas.

![]()

“Don’t listen to what I say. Listen to what I want.” – Detroit, “Sorry to Bother You,” Cinereach, 2018

“Don’t listen to what I say. Listen to what I want.” – Detroit, “Sorry to Bother You,” Cinereach, 2018

Five years ago, box office revenue was three times SVOD revenue. VOD surpassed ticket sales last year and cinema revenues are projected to plunge 66 percent this year. Ampere forecasts VOD will be more than twice the size by 2024. OTT has surged an estimated 26% this year and is projected to double by 2024 ($46.6 billion in 2019 to $86.8 billion in 2024). Even by 2024, Strategy Analytics projects that cinema revenues will be below the 2019 level but we’re not real sure about that if China’s return to seats in seats is any indication.

Overload – Movie theaters had it all – a special place for folks to go/be together, an exclusive for all of the very best content studios had to offer and unlimited candy, popcorn, snacks. Then 2020 hit and they discovered there were too many of them and the content either would come for a little while or the pipeline would dry up. Important but not that important.

Overload – Movie theaters had it all – a special place for folks to go/be together, an exclusive for all of the very best content studios had to offer and unlimited candy, popcorn, snacks. Then 2020 hit and they discovered there were too many of them and the content either would come for a little while or the pipeline would dry up. Important but not that important.

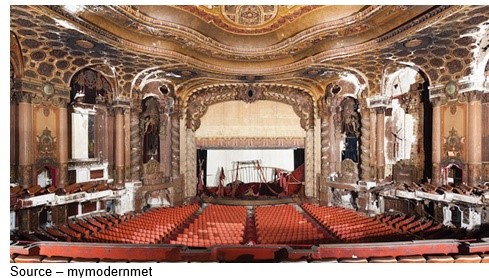

No! Professional theaters (plays, musicals, opera) are temporarily closed until people can safely get together in the communal environments to share the beauty and excitement of live appearances. Harlem’s famed Apollo Theater, which has hosted some of finest new and established acts from around the globe, will eventually reopen. People will again be entertained as much as folks were in 1913 when the burlesque and later the vaudeville venue emerged.

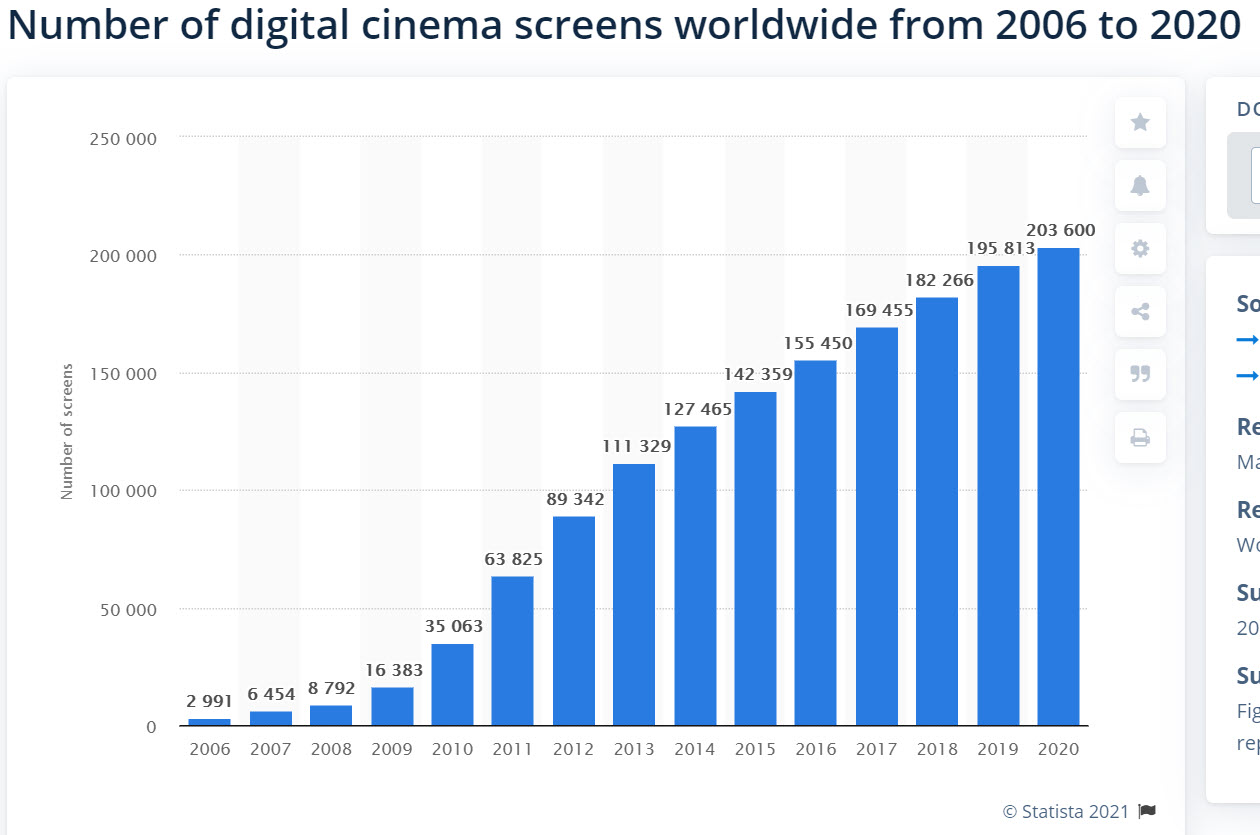

But some movie theaters will close permanently, others will thrive once again. Last year, there were more than 195.8 thousand digital cinema screens worldwide–up from 127.46 thousand five years earlier.

Number of digital cinema screens worldwide 2006-2020. Source:Statista

Number of digital cinema screens worldwide 2006-2020. Source:Statista

Digital screens have increased 20-fold in the past decade and IMax is continuing to expand its large-screen immersive venues around the globe. And they will probably do very well but hundreds, maybe thousands, of cinemas will close their doors … permanently. There are simply too many screens!

Tragically, a majority of theaters that will probably close will be local art house theaters where independent distributors and indie filmmakers present micro-, small- and medium-budget creative work that isn’t intent on pandering to “safe subject” audiences but people who like to think about the creative work during and after they leave the cinema. In addition, there are simply beginning to be too many films to watch while you’re home!

Or are there?

Next – You can’t turn around without encountering another great screen and a gigantic library of video stories. And still, there’s not enough because we want more.

Next – You can’t turn around without encountering another great screen and a gigantic library of video stories. And still, there’s not enough because we want more.

There’s Pay TV, D2C (PVOD – Paid, SVOD – Subscription, AVOD – ad-supported/free Video on Demand) and pirated stuff (yeah, we know, not you but … someone is doing it). New stuff, old stuff, borrowed stuff, foreign stuff; it’s an embarrassment of riches that is almost impossible to resist.

Sit Right Down – With all the confusion/chaos around you, it’s way too easy to simply curl up in front of the TV and watch something/anything rather than dressing up and going out for the evening.

Sit Right Down – With all the confusion/chaos around you, it’s way too easy to simply curl up in front of the TV and watch something/anything rather than dressing up and going out for the evening.

Soothsayers everywhere love to report how the new OTT options are killing traditional ad-supported appointment TV. In the US, a third of the households no longer have subscriptions because they like the freedom of choosing what they want, when they want, on the screen they want and … they hate the $100 +/- cable bill!

US penetration is down to about 78% while the Asia-Pacific market is expected to grow to more than 666M in two years. Similarly, the Latin American and MEA markets will increase.

Lack of Scripted Content

In case you missed it, one of the biggest challenges for Pay TV is the lack of high-quality scripted content. Unscripted shows, which we aggressively avoid, increased 24% this past year and have found a growing audience of people barricaded in their homes. When we see the fake reality TV shows promoted, the only thing we can think of is being seated in a coliseum in ancient Rome, rooting for the lion.

As the cancelled upfront gala showed early this spring, there were few fall/midseason series unveiled because of the long and aborted production periods. And the drought will continue into 2021. While networks are rushing to get new projects completed (comedy, crime/thriller, romance, drama, sci-fi and fantasy) they’re relying on their libraries of past shows to fill the entertainment gap.

But the content distribution market has grown broader and deeper.

First Delivery – You can blame Netflix for starting the streaming stampede. We bet studios and networks wished Blockbuster would have taken Hastings up when he offered to sell his little company to him.

First Delivery – You can blame Netflix for starting the streaming stampede. We bet studios and networks wished Blockbuster would have taken Hastings up when he offered to sell his little company to him.

Everything was still going well for theaters and Pay TV until Reid Hastings and the old red envelope company decided it was time for a change. O.K., it wasn’t just Netflix at that time (In fact, it was a small streaming on-demand service in early 2000 called SelectPlay that kicked things off.), but it didn’t take long for everyone to figure out that going direct to consumer (D2C) was not only fun (bypassing the cable guy) but maybe profitable. “Overnight” this past year more than 1K OTT services have emerged to give consumers different, unique content they could enjoy on their own terms.

It’s Everywhere – OTT content comes from a lot of creative sources around the globe and it continues to grow in every quarter.

It’s Everywhere – OTT content comes from a lot of creative sources around the globe and it continues to grow in every quarter.

The current global SVOD leaders are Netflix, Amazon, Disney+, Apple TV+ and YouTube. Often referred to as ‘the Big 5’, they are far from alone in their quest to capture subscriber screens.

Despite a stumble out of the gate, AT&T/Warner/HBO Max is focused on capturing market share while balancing the needs of their parent’s $85 billion debt along with those same parents’ desire to keep theater chains happy/supplied (tentpole movie Tenet ultimately brought in about $350M in ticket sales).

Phone, Content – AT&T has a hunger for it all – serving your screen and controlling content and its production; and yes, servicing a huge debt. Sometimes you can’t please everyone or do everything right. But … we’ll see what they sell next.

Phone, Content – AT&T has a hunger for it all – serving your screen and controlling content and its production; and yes, servicing a huge debt. Sometimes you can’t please everyone or do everything right. But … we’ll see what they sell next.

Disney+ and Hulu have shown the fastest growth (14% and 17% respectively) nationally and internationally. Disney’s willingness to add PVOD offerings like Hamilton and Mulan to stimulate awareness and interest in subscribing to their service has worked, growing global subscriptions to more than 86M in a mere nine months since the launch with its eye on being a $40 billion streaming giant within five years.

Hulu (owned by Disney), CBS All Access, BBC, ESPN+ (Disney), Sky’s Now TV, iflix and a myriad other subscription services are also vying for subscribers.

Global, Pacific Basin – Things look very promising for the Big 5 streaming services until you get a closer look at the three Chinese services. Then things get “interesting.”

Global, Pacific Basin – Things look very promising for the Big 5 streaming services until you get a closer look at the three Chinese services. Then things get “interesting.”

While the US still represents the largest entertainment market (43%), the protected borders of China is the world’s second largest – and eyeing top slot – entertainment market (1.4 billion population).The country’s fast-growing, deep-pocketed ‘BAT’ firms – Baidu (iQiyi), Alibaba (Youku) and Tencent – are also focusing on the international arena.

Allan McLennan, Chief Executive of Padme Media Group, noted that the Big 10 streamers still have more international experience and production quality than the BAT firms.

“The Big ten are focused on improving their quality and quantity. They are co-producing variety shows, drama, animation and other projects for their local and global markets. It’s not a matter of if they will be able to compete as equals in the entertainment world, but how soon.”

iQiyi has more than 100M paying subscribers, Tencent over 95M and Youku more than 85M subscribers. In addition, all three have 100s of millions of ad-supported viewers. India, also with a population of about 1.4 billion, has a number of leading AVOD and SVOD services, including Hotstar (Disney) with about 400M active users, while Amazon Prime and Netflix each hold a 20% share of the country’s OTT market.

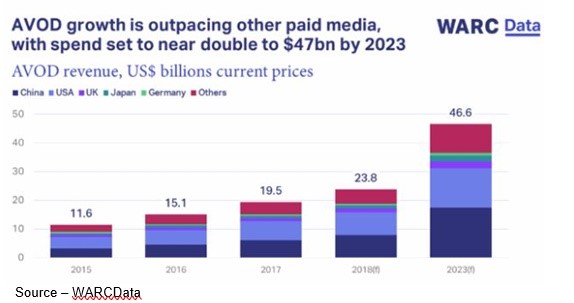

Ad Supported – “Free” content isn’t as popular in the Americas and EU as it is in APAC countries. But as folks’ subscription expenses grow, they’re warming up to the ad-supported services.

Ad Supported – “Free” content isn’t as popular in the Americas and EU as it is in APAC countries. But as folks’ subscription expenses grow, they’re warming up to the ad-supported services.

While the most preferred OTT services in India and China are ad supported, AVOD has only recently become attractive service additions for people in the rest of the world … thank gawd! Until this year, ad-supported services only existed in the long shadows of subscription services until people suddenly began suffering from subscription fatigue. Joyn, Tubi, Rakuten, Pluto TV and Peacock have been low-key “free” services in the America’s and EU.

McLennan noted:

“Ad-supported services were thought of as low-quality, ancient shows/movies until recently. Backed by major entertainment players, Tubi/Fox; Joyn/ProSiebenSat.1 and Discovery; Rakuten; Pluto TV/ViacomCBS and Peacock/Comcast’s NBC Universal have upgraded and expanded their content libraries, enhanced their UIs (user interfaces) and expanded their marketing and international reach.For example, Pluto is now regularly recording 80M users/month while Tubi has 33M MAUs (monthly average users) and both are aggressively expanding in Latin American and European markets,”

McLennan said there are two key reasons the ad-supported services are growing:

- People suddenly find 4-5 SVOD services aren’t any less expensive than their cable bundle

- The services maintain a much shorter ad slot – 3-4 minutes per 60-minute show vs 15-20 minutes in broadcast shows

He continued, saying,

“Because the services are IP-based, marketers are beginning to understand they are more easily able to serve ads to people who more closely meet their product’s ideal customer profile and are tailored to their wants and needs. In other words, it is more precise than broadcast TV’s GRP (gross rating point) system, so the ads are less obtrusive and better accepted,” he added. “Everyone wins!”

But people are mentally tired of searching through the 4-7 services looking for “something!”

Single Source – People who have cut or never had a cord don’t want to rush to the cable service unless they can give them one choice for reaching across all of their content and help with instant evening entertainment selection.

Single Source – People who have cut or never had a cord don’t want to rush to the cable service unless they can give them one choice for reaching across all of their content and help with instant evening entertainment selection.

Options like Roku, Amazon Fire and Apple TV devices are okay solutions. But folks really want one aggregated solution that’s well developed and well executed – one that gives them a wide choice of content and manages their content billing all in one house. Yeah, it’s the old Pay TV bundle you ditched but without the forever, no-break contract.

McLennan contends that they’re well positioned to handle the task since Comcast, Charter, Sky, Rogers, all of them; have the audiences, relationships and pipes and are already serving three quarters of the entertainment audience. Far from SVODs being competitors of the aggregators, there are strong benefits because they can add services/content without having to wade through the heavy lifting negotiations. Of course, streamers aren’t willing to share subscriber data but the big three (Netflix, Amazon, Disney) have already hammered out the details with pipe service providers in many countries around the globe.

The next phase for them is a range of slimmed-down Pay TV bundle options combined with AVOD and subscription options. Then they can offer the single unique service consumers have been begging for – search and discovery across all of the customer’s content sources to provide entertainment recommendations based on the most popular content as well as their viewing habits/experience. Organizations like Comcast have already added integrated voice and text search, single remote control and fairly simple billing.

In addition, they’ve added home security solutions as well as fixed and mobile phone services to become more useful, more indispensable to the family.

In the long term, the move will benefit everyone in the M&E ecosystem … especially the consumer. Imagine a solution where everyone will be treated equal and everyone will win. It’s like Detroit said in Sorry to Bother You,

“We will have a transformative experience.”

It’s about freakin time! (AM)

Andy Marken – [email protected] – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media and industry analysts/consultants.