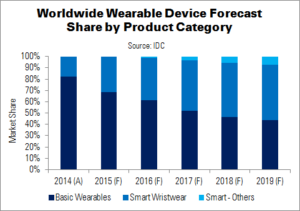

New vendors; new devices; a growing number of experiences and price points; and steady consumer adoption will drive the global wearable market in the future, says IDC. The firm forecasts that wearable device shipments will reach 76.1 million units this year, representing 163.6% growth from 28.9 million units in 2014. By 2019, IDC expects worldwide wearable shipments to reach 173.4 million units; this leads to a five-year CAGR of 22.9%. Figures include both basic (i.e. Fitbit) and smart (i.e. Apple Watch) devices.

Smart wearables represent about a third of today’s market. However, says IDC’s Jitesh Ubrani, “Driven by advancements in user interface and features, smart wearables are on track to surpass the lower priced, less functional basic wearable category in 2018”. These products are expected to move from being a smartphone accessory to standalone devices, capable of performing more processing by themselves.

Smart wristwear is a particularly fast-growing segment of the market. More vendors are entering the category, providing consumers with a wider selection of products and – ultimately – more volumes. Potential buyers are likely to be more interested when second- and third-generation devices are launched.

Ramon Llamas, IDC analyst, says that customers will need to be aware of the different operating systems in use in the wearable space. Different wearable OSes will be compatible with different smartphone platforms, and sometimes only with specific models.

Apple’s WatchOS is expected to establish itself quickly as the smart wristwear market leader, and maintain its position through 2019. Second- and third-generation devices are expected to drive wearable volumes later in the forecast period. However, the platform’s share will be eroded as rival systems – particularly Android Wear – come to the fore.

Android and Android Wear will experience ‘market-beating’ growth. Used by a combination of leading consumer electronics brands and an expanding list of watchmakers, the OS will be supported by a broad selection of devices at multiple price points.

The market share of Pebble – which mainly sells basic wearables – will fall, even as volumes grow. However, low price points, compatibility with Android and iOS smartphones and an ‘avid’ fan base will sustain its presence.

IDC calls Tizen a potential ‘dark-horse platform’. Samsung has opened up its Tizen SDK and made its products compatible with devices from other Android manufacturers, opening up the company’s potential market. However, the OS must first win over customers considering other watches compatible with Android phones.

Although Linux entered the wearable market last year, adoption amongst OEMs has so far been limited – a trend that IDC expects to continue.

IDC predicts a ‘small, but nonetheless significant’ market for smart wristwear running on a real-time operating system (RTOS) (capable of running third-party apps), but not on any of the above platforms. These tend to be proprietary OSes, which will be used when OEMs want to promote their own devices. These will help within specific markets of devices, but will not overtake the majority of the market.

| Top Five Smart Wristwear Operating Systems’ Shipments, Market Share and CAGR (Millions) | |||||

|---|---|---|---|---|---|

| Smart Wristwear OS | 2015 Units | 2019 Units | 2015 Market Share | 2019 Market Share | Five-Year CAGR |

| WatchOS | 13.9 | 40.3 | 58.3% | 47.4% | 30.6% |

| Android/Android Wear | 4.1 | 32.6 | 17.4% | 38.4% | 67.5% |

| Pebble OS | 2.1 | 2.6 | 8.7% | 3.1% | 6.4% |

| RTOS | 2.0 | 7.6 | 8.3% | 9.0% | 40.1% |

| Tizen | 1.6 | 1.8 | 6.7% | 2.2% | 3.7% |

| Other | 0.1 | 0.0 | 0.6% | 0.0% | -100.0% |

| Total | 23.8 | 85.1 | 100.0% | 100.0% | 37.5% |

| Source: IDC | |||||