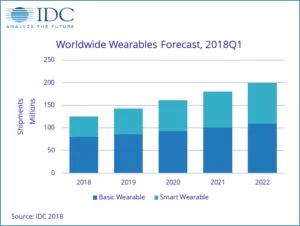

The worldwide wearables market is forecast to ship 124.9 million units by the end of 2018, up 8.2% from the prior year.

Although this growth is slightly lower than the 10.3% growth experienced in 2017, the market is expected to return to double-digit growth from 2019 until 2022 as smartwatches and other form factors grow in popularity, according to the International Data Corporation (IDC) Worldwide Quarterly Wearable Device Tracker.

“The shift in consumer preferences towards smartwatches has been in full swing these past few quarters and we expect that to continue in the coming years,” said Jitesh Ubrani senior research analyst for IDC Mobile Device Trackers. “While Apple will undoubtedly lead in this category, what bears watching is how Google and its partners move forward. WearOS (formerly Android Wear) has been somewhat of a laggard recently and despite expected changes to the OS and the release of new silicon, we anticipate Android-based watches to be WearOS’ closest competitor due to the high amount of customization available to vendors and the lack of Google services in China.”

“Additionally, keep an eye on the other smartwatch platforms, including Fitbit’s Fitbit OS, Garmin’s Connected IQ, and Samsung’s Tizen,” said Ramon T. Llamas, research director for IDC’s Wearables team. “Fitbit’s Versa has had a warm reception in the market, and Garmin’s devices have had a steady presence for many quarters. Expect both companies to dive deeper into health and fitness while exploring new areas as well. Samsung, meanwhile, continues to make strides in the commercial space, including health care and wearable workflows.”

Smartwatches will evolve to encompass far more features and functionalities than they have today. “The smartwatches of 2022, even 2020, will make today’s smartwatches seem quaint,” added Llamas. “Health and fitness is a strong start, but when you include cellular connectivity, integration with other Internet of Things (IoT) devices and systems, and how smartwatches can enable greater efficiencies, the smartwatch market is heading for steady growth in the years to come.”

Beyond the typical wrist-worn devices, IDC also anticipates earwear to gain momentum as various brands start to capitalize on the growing interest in smart assistants. Qualcomm’s upcoming silicon designed for this category is likely to also help bolster supply by offering brands a platform solution to build their products. Clothing with built-in sensors is also expected to grow and double its share by 2022.

Category Highlights

Smartwatches will gain an increasing amount of market share over the course of the forecast, accounting for 44.6% of all wearables shipped by the end of 2022. Apple’s decision to include cellular connectivity on the latest Watch has helped bring some much-needed attention to the smartwatch category from telcos and, more importantly, it has helped with consumer acceptance. It’s only a matter of time before other vendors (beyond those who have already dabbled with it) begin to include this capability and consumers, along with developers, take advantage of the tech to enable additional use cases.

Basic watches, which to date have been primarily comprised of sport watches, kids’ watches, and hybrid watches, are forecast to see a compound annual growth rate (CAGR) of 7.4% from 2018 – 2022. Though these devices offer many advantages such as long battery life, simplified interfaces, and highly fashion-forward designs, this category will continue to remain in the shadow of smartwatches as its share declines from 23.7% in 2018 to 19.7% in 2022. The entire category also faces internal challenges as many sport watch and kids’ watch vendors are focused on transitioning their user base to smartwatches in hopes of increasing revenue.

The market for wristbands is expected to decline 6.6% in 2018 as demand for these simple devices has cooled off and incumbents like Fitbit and Garmin continue to pursue smartwatch growth instead. Beyond 2018, the category is expected remain largely flat with growth below 1% in the following years. Meanwhile, average selling prices (ASPs) are expected to drop below $50 by 2022.

|

Worldwide Wearables Forecast, Product Shipments, Market Share and CAGR, 2018 and 2022 (shipments in millions) |

||||||

|

Product |

OS |

2018 Shipments* |

2018 Market Share* |

2022 Shipments* |

2022 Market Share* |

2018–2022 CAGR |

|

Smartwatches |

watchOS |

20.2 |

16.2% |

34.5 |

17.3% |

14.3% |

|

Wear OS |

5.4 |

4.3% |

19.6 |

9.8% |

38.0% |

|

|

|

Android |

8.0 |

6.4% |

17.4 |

8.7% |

21.3% |

|

|

Others |

9.8 |

7.8% |

17.6 |

8.8% |

15.7% |

|

Smartwatch Total |

43.5 |

34.8% |

89.1 |

44.6% |

19.6% |

|

|

Wristbands |

45.1 |

36.1% |

45.9 |

23.0% |

0.4% |

|

|

Basic Watches |

29.6 |

23.7% |

39.3 |

19.7% |

7.4% |

|

|

Earwear |

2.2 |

1.8% |

12.6 |

6.3% |

54.4% |

|

|

Clothing |

3.4 |

2.7% |

11.7 |

5.9% |

36.4% |

|

|

Other |

1.2 |

0.9% |

1.2 |

0.6% |

0.7% |

|

|

Total |

124.9 |

100.0% |

199.8 |

100.0% |

12.5% |

|

|

Source: IDC Worldwide Quarterly Wearable Device Tracker, June 18, 2018 |

||||||

* Note: All figures represent forecast data.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools.

For more information about IDC’s Worldwide Quarterly Mobile Phone Tracker, please contact Kathy Nagamine at 650-350-6423 or [email protected].

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly-owned subsidiary of International Data Group (IDG), the world’s leading media, data and marketing services company that activates and engages the most influential technology buyers. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn.