In the second quarter of 2024, gaming PC shipments reached approximately 10.6 million units, marking a year-over-year (YoY) recovery of 2.4%. This improvement is attributed to inventory replenishment and favorable comparisons against a challenging 2023, resulting in the first positive quarter since early 2022. Meanwhile, gaming monitor shipments soared to nearly 6.5 million units, representing a 35% increase YoY, as aggressive promotions and emerging vendors drove growth for the fifth consecutive quarter, according to the IDC.

IDC noted that the slowdown in gaming PC sales can be linked to a lack of compelling hardware and reduced investments in adjacent markets, such as handheld devices. Despite potential market recovery in upcoming quarters, the overall volume of gaming PCs is projected to remain below levels seen in 2021, as consumers increasingly explore alternative gaming methods.

Gaming monitors reached significant milestones during the second quarter, with shipments hitting the highest level since IDC began tracking the market in 2016. Gaming now constitutes 20% of the total monitor market, driven by ongoing price declines and shifts in consumer spending due to the sluggish gaming PC sector. The average price of gaming displays has fallen below $300.

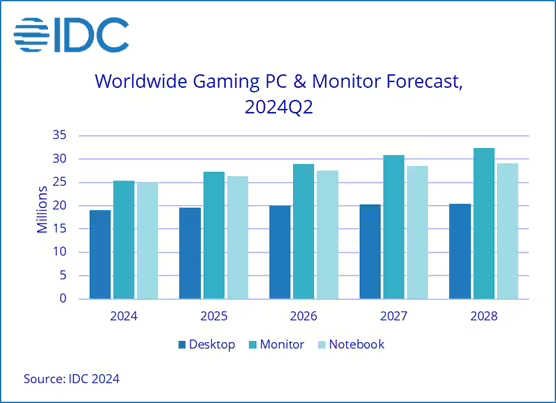

Total gaming volume is expected to rise to 69.3 million units in 2024, a 9% increase from 2023. The gaming desktop segment, critical for high-end gaming, is anticipated to rebound in 2025 as new GPUs become available. Gaming is projected to capture a growing share of the overall PC and monitor market, potentially reaching 20% by 2028.