In the year 2022, foldable smartphone shipments are expected to follow a growth path, while the total global smartphone market is expected to decline. The total market is impacted by inflation, continued geopolitical risks and supply chain constraints.

New product introductions, innovative designs, increased reliability, better features, higher performances and competitive pricing are helping to drive foldable smartphones demand. The biggest potential advantage of foldable smartphone is that they can offer “thin, light, larger display in a smaller form factor”. In a market with slowing demand, foldable phones offer potentially higher growth, ASPs, revenue and profitability opportunities for panel and smartphone suppliers. Foldable smartphones can also offer new opportunities for OLED fabs utilization rates due to an increase in the number of displays, increases in display sizes and display area.

On August 10th this year Samsung announced its fourth generation foldables Z Flip4 and Galaxy Z Fold4 with enhanced productivity, customizable form factors and upgraded performance. The next day on August 11th, Xiaomi introduced its second generation thinner foldable, Mix Fold 2, in China. The same day Motorola launched a new clamshell smartphone with significantly upgraded specs, the Motorola, Razr 5G for the Chinese market. With more robust innovative form factors, better price performance and technology advancements, foldable phones are forecast to follow a growth path over the next five years, but they will occupy a small percentage share of the total global smartphone market. They are expected to have a stronger presence in the premium market.

Evolving Form-factors

?Royole was the first company to introduce foldable phones in Q4 2018, but the market really started in Q4 2019 with Samsung’s entrance. Foldable phones have come a long way from the first-generation phones from Samsung and Huawei which were introduced in 2019 with foldable OLEDs. In the beginning, the industry had in-fold, out-fold, clamshells and other designs. First generation products also had many issues with foldable hinges, flexible covers, increased thickness and bulkier designs. Prices were in $2000 range. Also, flagship phones with flexible OLEDs had better features with lower prices making foldable phones less competitive.

Starting from 2020, the industry mostly focused on in-fold and clam-shell designs. Many new suppliers also joined, such as Motorola and Xiaomi. The introduction of the Z-Flip from Samsung in 2020, with a new innovative flip design, a thinner form factor, higher robustness with UTG (Ultra-Thin Glass), and a lower price point, helped to increase interest and sales.

In the initial stages, higher prices were a big challenge for foldables. By 2H 2020, Samsung had its first LTPO display based Z fold2, with a 120Hz, 6.23” front display, 7.6” main display and UTG, powered by Samsung Display’s technology developments. The clamshell design was the first product to use UTG, resulting in a smaller seam, more protection for the display and the smartphone also had a lower price.

Better Price Performance

On March, 2020, Samsung announced Z Flip, its second foldable smartphone, a newly designed foldable flip phone based on flexible AMOLED display but with an ultrathin glass cover rather than plastic. At a price of $1380, Z Flip was cheaper than Samsung’s first foldable with bigger screen size, Galaxy Fold ($1980), but was more expensive than the Galaxy S20($999,99).

According to Omdia press release in March 2022, “Due to the high price barrier, sales of early foldable smartphones were limited. However, from the second half of 2021, sales volume increased rapidly with annual foldable smartphone shipments reaching 9 million units in 2021, up 309% year-on-year. Of these, 8 million units were sold in the second half of 2021, accounting for 89% of the total shipment in 2021.Samsung is the largest original equipment manufacturer (OEM) in the foldable smartphone market. To date, Samsung has shipped over 10 million units, accounting for more than 88% of the foldable smartphone market, which is also the only brand in the market with over 10 million foldable smartphones.” According to the company, in 2021, Samsung’s Z Flip3 5G became the word’s largest foldable smartphone model. Z Flip3 5G was released at $999, $380 cheaper than its predecessor. Through hardware upgrade and price cut Samsung was able to ship more Z Flip3 5G units in 2021 compared to the predecessors in 2020. The launch price of the Galaxy Z Fold3 was $1800, which was $200 cheaper than 2020 model of Z Fold2. Recently introduced Samsung Z Flip4 and Z Fold4 foldable smartphones launch prices were same as last year.

More Advanced Technology

The commercialization of foldable smartphones up to now has been based on foldable AMOLED (active-matrix organic light emitting diode) display technology. For a foldable display, all the layers within the panel should be foldable, durable, and transparent with a total bending radius of less than 1.5 mm. That is why new components are needed for foldable OLEDs. Foldable requirements are as follows:

- Flexible Windows: Film/UTG. Cover windows need to have hybrid organic/inorganic coating with excellent mechanical and thermal properties (Polyimide (PI))/Resilient Flexible UTG (Chemical Strengthening)

- Thin Polarizer: Thin Flexible Polarizer/Polarizer Less to reduce thickness

- Flexible Touchscreen: Add On/On-cell Reduce thickness and improve flexibility (Needs non-ITO materials such as silver nanowire or metal mesh)

- Flexible Adhesive: OCA/OCR

- Reliability (to withstand more than 200K times bending/folding).

Bendability has a trade off with durability and robustness. Bending of a very thin film after a certain point can generate a crease or lead to deformation. The display industry has developed numerous materials and processing challenges to balance bendability with durability. The foldable design revolution is still facing high costs, high price, design complexity and a lack of standardization, limiting the ability to create consumer-acceptable mainstream solutions.

Samsung Display is the dominant supplier for the foldable OLED panel and will continue to dominate in next five years according to DSCC data shown at the SID/DSCC 2022 Business Conference. BOE is in the number 2 position and Visionox and CSOT are fighting for the number three position.

Higher Adoption Rate

Foldable represents the most innovative segment of the market. Although they have not yet captured a significant share of the total smartphone market, they have a strong presence in the premium market.

According to a DSCC blog by David Naranjo, Senior Director in July, 2022:

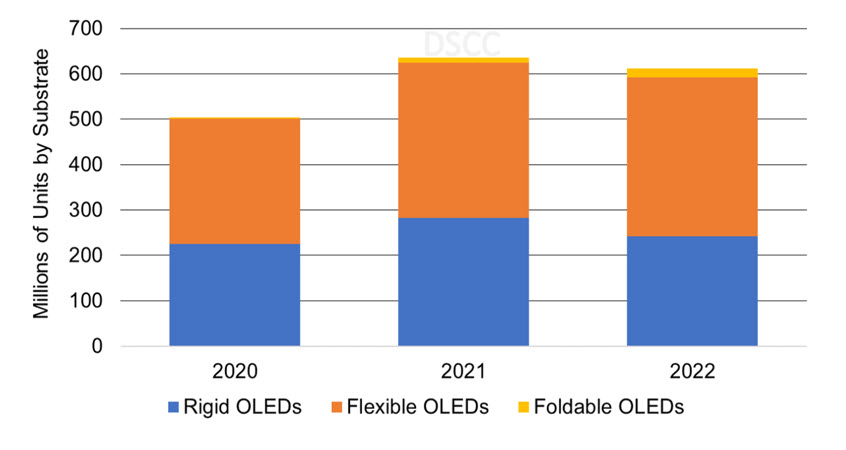

“For 2022, we expect OLED smartphone panels to decrease 4% Y/Y to 612M panels. Flexible OLED smartphone panels are expected to increase 2% Y/Y and account for a 57%unit share, up from 54% in 2021. Rigid OLED smartphone panels are expected to decline 14% Y/Y and account for a 40%unit share, down from 44% in 2021. Foldable OLED smartphone panels are expected to increase 102% Y/Y for a 3%unit share, up from 2% in 2021”.

The revenue share is expected to be even higher. As David Naranjo noted in his blog,

“On a smartphone device revenue basis, we expect rigid OLED smartphone device revenue to decline 10% Y/Y with a 23% revenue share, down from 26% in 2021. Flexible AMOLED smartphone device revenue is expected to decline 1% Y/Y and maintain a 71% revenue share. Foldable AMOLED smartphone device revenue is expected to increase 82% Y/Y with a 5% revenue share, up from 3% in 2021”.

Samsung has been the main driver for advancing the foldable market especially empowered by the technology development of Samsung Display and other partners.

According to Dr. TM Roh, President and Head of Mobile eXperience Business at Samsung Electronics as presented in Samsung’s recent press release.

“Through our unwavering focus and industry leadership, excitement for the foldables continues to grow. We’ve successfully transformed this category from a radical project to a mainstream device lineup enjoyed by millions worldwide.”

He also said in another recent write up,

“Last year, we saw almost 10 million foldable smartphones shipped worldwide. That’s an industry increase of more than 300% from 2020, and I predict this fast-paced growth will continue. We are reaching the moment where these foldable devices are becoming widespread and staking a bigger claim in the overall smartphone market”.

New foldable products, 5G capabilities, innovative designs and evolving form factors have created a strong growth path especially with early adaptors driving demands. However, long term success by gaining even significantly more share of smartphone market will require lower costs, lower prices, better standardization, and form factors that will be accepted by mainstream consumers. Foldable OLED smartphones can offer potentially higher growth, ASP, revenue, and profitability opportunities for panel and smartphone suppliers. (SD)

Sweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact [email protected] or visit www.dash-insights.com