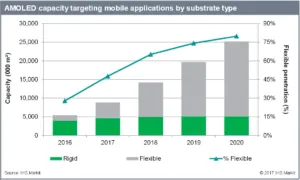

In the current, unprecedented phase of active matrix organic light emitting diode (AMOLED) panel factory build-out, flexible AMOLED capacity will expand from 1.5 million square meters to 20.1 million square meters between 2016 and 2020, at a compound annual growth rate of 91 percent.

In 2016, flexible capacity, or factories with the ability to produce AMOLEDs on plastic substrates, only accounted for 28 percent of total capacity targeting mobile applications. This will increase to 80 percent by 2020 as almost every new Gen 6 fab and smaller factory built over the next four years will be flexible compatible, according to IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

According to the Display Supply Demand & Equipment Tracker by IHS Markit, between 2016 and 2020, China, Japan and South Korea will build the equivalent of 46 new flexible AMOLED fabs, whose monthly capacity reaches 30,000 substrates, each. These fabs will add 18.6 million square meters of new plastic substrate production capability, more than 13 times the industry’s current level.

“All of the new capacity will facilitate a rapid increase in flexible AMOLED panel adoption in smartphones,” said Charles Annis, senior director at IHS Markit. “Nevertheless, as so much new flexible capacity is being added, it is starting to raise concerns that the market will not be able to absorb all of the potential output.”

IHS Markit forecasts that the tight AMOLED panel supply in 2016 will continually give way to a growing capacity-based glut. The supply is predicted to exceed demand by more than 45 percent in 2020, when 40 percent of smartphones will adopt AMOLED panels.

“AMOLED displays will offer excellent image quality and form factor advantages in high-end phones. Despite excessive capacity availability, the challenge to faster adoption will be costs,” Annis said. High manufacturing costs for most makers will keep average rigid AMOLED panel prices 40 percent above equivalent LCD panels, while flexible AMOLED panel prices will remain 100 percent higher. “Smartphone makers, targeting mid and low-end market segments, may want to buy flexible AMOLED panels, but are likely to be restricted by lingering high prices.”

To absorb all the new capacity in the pipeline, flexible AMOLED panels will need to expand the market beyond smartphones to tablet PCs, notebooks and new form factors enabled by foldable displays. Ultimately, the rapid growth of flexible AMOLED capacity and the resulting increase in panel production will help to lower costs, increase yields and improve quality. In the long-run, this will spur further adoption into more applications; however, to get there, the industry may first need to cycle through a difficult period of digesting the 46 new flexible fabs now being built.

The Display Supply Demand & Equipment Tracker by IHS Markit covers all key metrics used to evaluate supply, demand and capital spending for all major flat panel display technologies and applications.