That cellular connectivity will be a growth driver for tablets and hybrid devices in the future, is the main take-away from both IDC and Gartner’s new data set releases.

IDC believes that worldwide tablet growth will continue to slow in 2015, falling 3.8% YoY to 221.8 million units. This follows two consecutive quarters of declines for the market, and is a downward revision from IDC’s previous prediction of 2.1% growth to 234.5 million units. Cellular tablets and hybrids will buck this trend, however.

“[C]ellular-connected devices fill multiple needs for vendors and carriers around the world”, said IDC’s Jean Phillipe Bouchard. “[T]hey offer a quick solution to price and margin erosion, and when compared to smartphones, they offer a less expensive way for carriers to increase their subscriber base”.

Although cellular-enabled devices are still only a small portion of the wider tablet market, IDC predicts growth for the segment. A five-year CAGR of 5.6% is forecast, compared to Wi-Fi-only devices’ -0.4% CAGR over the same period.

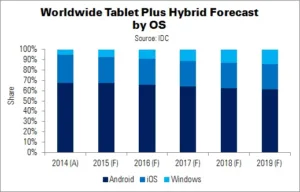

Another trend damaging the tablet market is phablet cannibalisation. The popularity of these products is expected to play a part in the falling share of small-screen tablets, from 64% (2014) to 58% (2015), and sub-50% in 2019. There is also a related impact on ASPs, as large-screen devices tend to cost more.

| Worldwide Tablet plus Hybrid Market Share, by Connectivity, 2014, 2015 and 2019 | |||

|---|---|---|---|

| Connectivity | 2014 Share | 2015 Share (F) | 2019 Share (F) |

| Cellular | 31% | 33% | 40% |

| WiFi-Only | 69% | 67% | 60% |

| Total | 100% | 100% | 100% |

| Source: IDC | |||

Gartner writes that cellular-enabled device sales (including tablets, mobile PCs and mobile hotspots, but excluding smartphones) will exceed 112 million units this year: a 5.6% YoY increase.

The rise in cellular-enabled devices creates new revenue opportunities for both device vendors and telco service providers. Some vendors are trialling new business models: for instance, HP is working with Qualcomm and T-Mobile to offer 200MB of free data per month on its Stream Book 13 4G laptop.

Tracy Tsai, Gartner research director, says that the segment has the potential for fast growth. The price gap between Wi-Fi-only and cellular devices is shrinking; the firm expects the gap to narrow to less than 10% ($20) by 2019. This will cause acceleration to rise beyond 160 million devices, with the potential to exceed 600 million units.

Mobile PCs

Globally, cellular-enabled mobile PCs will rise from 1.8 million to 4.9 million units between 2014 and 2019. Penetration will grow from 1.3% to 2.7% – total penetration remains low, as the majority of mobile PCs are still desk-based and can be used with fixed broadband.

Within this segment, premium ultramobiles will experience the fastest growth: from 492,000 units (2014) to 3.2 million (2019). This category is emerging as a notebook replacement for mobile users and business travellers who require constant connectivity. More than 60% of such devices are sold in Western Europe; higher ASPs are a barrier to entry in emerging markets.

Gartner expects cellular-enabled notebooks to continue to grow, but at a slower rate: from 1.3 million units in 2014, to 1.6 million in 2019. Business users in Europe and North America are particularly keen on this form factor, which ranges from 14″ – 15.6″.

Tablets

Tablets are the largest segment of cellular-enabled devices. Sales passed 50 million last year, and are expected to exceed 76 million in 2019. Consumers purchase more than 84% of cellular-enabled tablets.

Unlike premium ultramobiles, emerging markets are dominant in cellular tablet buying, with a 62% market share. Cellular-enabled devices are the primary form of internet access in these countries; fixed broadband only has about 6% penetration in India, for example.

Gartner’s data from last year showed that only 25% of tablets in the USA, and 33% in Germany, have cellular connectivity. However, these figures rise to more than 52% in India and 49% in Brazil.

Finally, Gartner expects mobile hot spot sales to rise from 54 million in 2014, to 70 million in 2019. Wireless types are preferred.