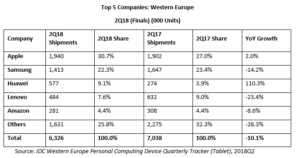

According to the latest figures published by International Data Corporation (IDC), the overall tablet market for Western Europe declined 10.1% YoY, shipping 6.3 million units in the second quarter of 2018 (2Q18).

Slates exhibited a degree of resilience in the commercial space, following strength in certain niche use-case deployments. However, market saturation, lengthening life cycles and a lack of innovation resulted in the ongoing sluggish demand on the consumer side, leading to an overall decline of 6.1% YoY. In terms of volume, detachables had a challenging quarter, declining by 23.3% YoY. As the market has become increasingly dominated by Apple and Microsoft, and consequently more premium-focused, the range of options available to more price-constrained customers has diminished, leading them to consider cheaper alternatives such as lower end convertibles or even traditional PCs. Furthermore, the announcement of upcoming product releases from the main players likely acted as an inhibiting factor on overall demand this quarter, as customers postponed their purchases in anticipation of these newer devices.

“Apple repeated last year’s successful strategy of positioning the iPad at a more attractive price point to address the erosion of consumer demand for tablets,” said Daniel Goncalves, senior research analyst, IDC Western European Personal Computing Devices. “This triggered a wave of renewals of old iPads and some Android tablets which helped Apple to perform above the market average and regain the leading position in Western Europe.

“Huawei, the other winner in the Western European tablet market, continues to pursue its strategy of increasing its penetration in the region. In tablets, particularly, the company found its sweet spot in the lower mid-range price bands and has been gaining market from other Android-based device manufacturers. Most of these companies are increasingly concerned about profitability and therefore reducing their presence in lower tier segments.”

Company Analysis

Apple ranked first with 30.7% market share and increasing 2.0% YoY. This quarter’s strength was largely driven by its slates, as the launch of the newer, attractively priced iPad led to a strong performance in the consumer space.

Samsung ranked second, recording a market share of 22.3%, but decreasing by 14.2% YoY. This decline can be attributed to the sluggish performance of premium Android devices, and also a degree of inventory management in preparation for the launch of the Galaxy Tab S4.

Huawei ranked third with a market share of 9.1% and increasing by a substantial 110.3% YoY. Its penetration strategy within Western Europe has proven to be very successful, as a solid growth of market share was achieved in the low-midrange space.

Lenovo ranked fourth with 7.6% market share, but with a heavy decline of 23.4% YoY. As it is primarily focused on consumer and lower-priced models, Lenovo was particularly susceptible to competition from Huawei and Apple’s cheaper iPad.

Amazon ranked fifth with a 4.4% market share but declined by 8.6% YoY. An expectantly weaker second quarter performance for Amazon, as consumers postpone their purchases until early July in anticipation of Prime day.

Note: Tablets are portable, battery-powered computing devices inclusive of both slate and detachable form factors. Tablets may use LCD or OLED displays (epaper-based ereaders are not included here). Tablets are both slate and detachable keyboard form factor devices with color displays equal to or larger than 7.0in. and smaller than 16.0in.

IDC’s Quarterly PCD Tracker provides unmatched market coverage and forecasts for the entire device space, covering PCs and tablets, in more than 80 countries — providing fast, essential, and comprehensive market information across the entire personal computing device market.

For more information on IDC’s EMEA Quarterly Personal Computing Device Tracker or other IDC research services, please contact Vice President Karine Paoli on +44 (0) 20 8987 7218 or at [email protected]. Alternatively, contact your local IDC office or visit www.idc.com.